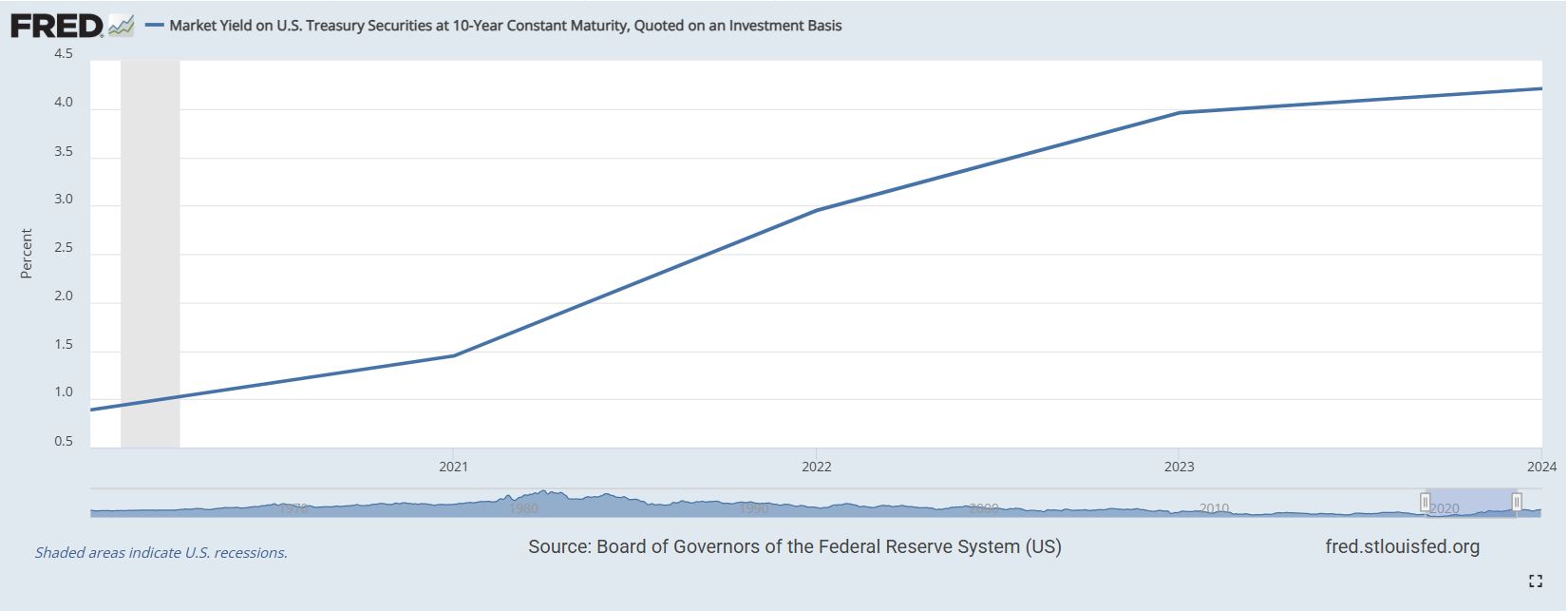

As of February 20, 2025, mortgage rates have seen an increase, with the national average for a 30-year fixed mortgage rate at 6.60% and a 15-year fixed rate at 5.93%. This upward trend in mortgage rates suggests that homebuyers and those looking to refinance should be prepared for sustained high rates in the near future.

Today’s Mortgage Rates February 20, 2025: Rates Are Going Up

Key Takeaways

- Current 30-Year Fixed Rate: 6.60%

- Current 15-Year Fixed Rate: 5.93%

- Refinance rates have also increased.

- Predictions indicate rates will remain elevated throughout 2025 and 2026.

Understanding today’s mortgage rates is essential for anyone considering a home purchase or refinance. High rates can significantly affect monthly payments, influencing both immediate financial commitments and long-term financial health.

Today's Mortgage Rates

Let’s take a closer look at the current mortgage rates according to Zillow:

| Mortgage Type | Interest Rate |

|---|---|

| 30-Year Fixed | 6.60% |

| 20-Year Fixed | 6.34% |

| 15-Year Fixed | 5.93% |

| 5/1 ARM | 6.57% |

| 7/1 ARM | 6.63% |

| 30-Year VA | 6.04% |

| 15-Year VA | 5.51% |

| 5/1 VA | 6.07% |

These rates are rounded national averages, and actual rates can fluctuate based on individual lender offerings and borrower qualifications.

Today's Mortgage Refinance Rates

For homeowners considering refinancing their existing mortgage, here’s a summary of the refinance mortgage rates currently available:

| Refinance Mortgage Type | Interest Rate |

|---|---|

| 30-Year Fixed | 6.62% |

| 20-Year Fixed | 6.40% |

| 15-Year Fixed | 5.98% |

| 5/1 ARM | 6.61% |

| 7/1 ARM | 6.43% |

| 30-Year VA | 6.01% |

| 15-Year VA | 5.60% |

| 5/1 VA | 6.07% |

| 30-Year FHA | 6.12% |

| 15-Year FHA | 5.56% |

Refinancing rates often vary from purchase rates and can depend on market conditions as well as the borrower's individual financial situation.

How Do Mortgage Rates Work?

Understanding how mortgage rates function is crucial for any prospective homebuyer or homeowner considering a refinance. A mortgage interest rate is essentially a fee for borrowing money from a lender. This fee is typically expressed as a percentage of the loan amount.

Types of Mortgage Rates

- Fixed-Rate Mortgages: These loans secure a specific rate for the entire term of the loan, meaning your monthly payment will remain steady, regardless of market fluctuations. For instance, a 30-year fixed mortgage at 6% means you pay 6% for the entire duration of the mortgage, making it easier to budget for your monthly expenses.

- Adjustable-Rate Mortgages (ARMs): ARMs often start with lower initial rates which can adjust after a specified period. If you opt for a 5/1 ARM, for example, you enjoy a fixed rate for the first five years before the rate may adjust annually based on market conditions. This can lead to savings initially, but there's the risk of significantly higher payments after the adjustment occurs.

How Are Mortgage Rates Determined?

Mortgage rates depend on various factors, including:

- Economic Indicators: The overall economy impacts rates greatly. When economic performance is weak, rates might be lower to encourage borrowing. Conversely, strong economic performance may lead to higher rates. Key indicators include inflation, employment rates, and actions taken by the Federal Reserve.

- Borrower Characteristics: Personal factors such as your credit score, debt-to-income ratio, and down payment amount can impact the mortgage rate you qualify for. Typically, higher credit scores and larger down payments can lead to lower rates, as lenders view these borrowers as less risky.

- Lender Policies: Different lenders may offer varying rates for the same borrower profile. It's often recommended that borrowers shop around to find the best deal.

Recommended Read:

Mortgage Rates Trends as of February 19, 2025

Mortgage Rates Predictions for Week February 17 to 23: What to Expect?

Will Mortgage Rates Go Up as Inflation Surges Back Up to 3%

Will Mortgage Rates Rise Back Above 7% or Go Down in 2025?

Mortgage Rate Predictions for February 2025: Will Rates Drop?

Today's Monthly Payment Calculations

Understanding how much you'll pay each month on your mortgage is crucial for budgeting and financial planning. Below, we explore monthly payments based on various mortgage amounts at today’s rates.

Monthly Payment on a $150,000 Mortgage

For a 30-Year Fixed Mortgage at 6.60%, the monthly payment is approximately $956. On the other hand, a 15-Year Fixed at 5.93% would lead to around $1,278, showcasing how the mortgage term dramatically impacts monthly obligations.

Monthly Payment on a $200,000 Mortgage

With the same terms, a 30-Year Fixed results in around $1,275 each month, while the 15-Year Fixed would increase to about $1,704. Homebuyers should evaluate their monthly budget carefully, balancing longer payment terms with the prospects of higher interest over time.

Monthly Payment on a $300,000 Mortgage

For a 30-Year Fixed mortgage at 6.60%, expect to pay approximately $1,913 monthly, whereas the 15-Year Fixed would mean payments of about $2,556.

Monthly Payment on a $400,000 Mortgage

If you were to borrow $400,000, that would result in monthly payments of $2,550 for a 30-Year Fixed mortgage or about $3,408 for a 15-Year Fixed. Given these substantial monthly obligations, first-time buyers may want to dig deep into their financial situations before committing.

Monthly Payment on a $500,000 Mortgage

Finally, a $500,000 mortgage will yield about $3,188 for a 30-Year Fixed mortgage and around $4,260 for the 15-Year Fixed. These examples illustrate the significant difference in monthly payment based on the loan amount and term, providing a clearer picture of financial commitments.

Understanding Payment Impact: Principal vs. Interest

In the early years of your mortgage, most of your monthly payment goes towards the interest accrued on the loan rather than the principal, called amortization. Many borrowers find it insightful to look at how their payments will shift over time:

- Initial Years: Higher interest payments, lower contributions to principal.

- Later Years: Decreasing interest portion and increasing principal repayments.

Understanding this shift can help homeowners recognize the equity build-up in their homes over time.

Impact of High Mortgage Rates on Homebuying

Higher mortgage rates can lead to a slowdown in home sales, as potential buyers reassess their budgets. It’s not uncommon for homebuyers to proceed with caution when rates exceed 6%. This effect can reduce overall housing demand, which might eventually prompt a cooling off in home prices. Nevertheless, buyers still need to recognize the long-term benefits of homeownership, even when facing higher payments.

Additionally, the impact of higher rates often causes buyers to consider lower-priced homes or to extend their home search to different neighborhoods or markets where home prices are more manageable.

- Is a 2.75% mortgage rate still achievable: While that rate was prevalent during the historic lows in 2020 and 2021, today’s market conditions make it unlikely to achieve such rates now.

- When should I consider refinancing: Homeowners typically consider refinancing if they can secure a rate that is 1% to 2% lower than their current mortgage rate, depending on their financial goals. It's crucial to calculate break-even points to determine if it makes financial sense after accounting for closing costs.

Summary: The Importance of Staying Informed

Understanding today’s mortgage rates is crucial for making informed financial decisions. With rates currently trending upwards, prospective homebuyers and existing homeowners contemplating refinancing should stay informed, assess their financial situations carefully, and consider securing an appropriate mortgage rate before potential further increases.

As the market continues to develop over the next year, staying abreast of rate changes will empower you to make strategic decisions that align with your financial objectives and homeownership dreams.

Work with Norada in 2025, Your Trusted Source for

Real Estate Investing

With mortgage rates fluctuating, investing in turnkey real estate

can help you secure consistent returns.

Expand your portfolio confidently, even in a shifting interest rate environment.

Speak with our expert investment counselors (No Obligation):

(800) 611-3060

Recommended Read:

- Mortgage Rates Forecast for the Next 3 Years: 2025 to 2027

- 30-Year Mortgage Rate Forecast for the Next 5 Years

- 15-Year Mortgage Rate Forecast for the Next 5 Years

- Why Are Mortgage Rates Going Up in 2025: Will Rates Drop?

- Why Are Mortgage Rates So High and Predictions for 2025

- NAR Predicts 6% Mortgage Rates in 2025 Will Boost Housing Market

- Mortgage Rates Predictions for 2025: Expert Forecast

- Will Mortgage Rates Ever Be 3% Again: Future Outlook

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions for 2025: Expert Forecast

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?