The housing market trends are captivating as they reveal significant shifts in home prices, buyer behavior, and overall market dynamics. As we navigate through 2024, understanding these trends becomes crucial for potential buyers, investors, and policymakers. Recent reports showcase an intriguing upward trajectory in U.S. house prices, with a 5.7 percent increase noted over the past year, a reflection of sustained demand and varied regional influences.

Housing Market Trends 2024: Current Patterns and Predictions

Key Takeaways

- Annual Appreciation: U.S. house prices have appreciated annually since 2012.

- State Variations: Vermont leads the nation with a 13.4 percent increase in house prices.

- Metropolitan Insights: 96 out of the top 100 largest U.S. metropolitan areas saw price increases in the past year.

- Inventory Challenges: Elevated mortgage rates and housing inventory are affecting growth rates.

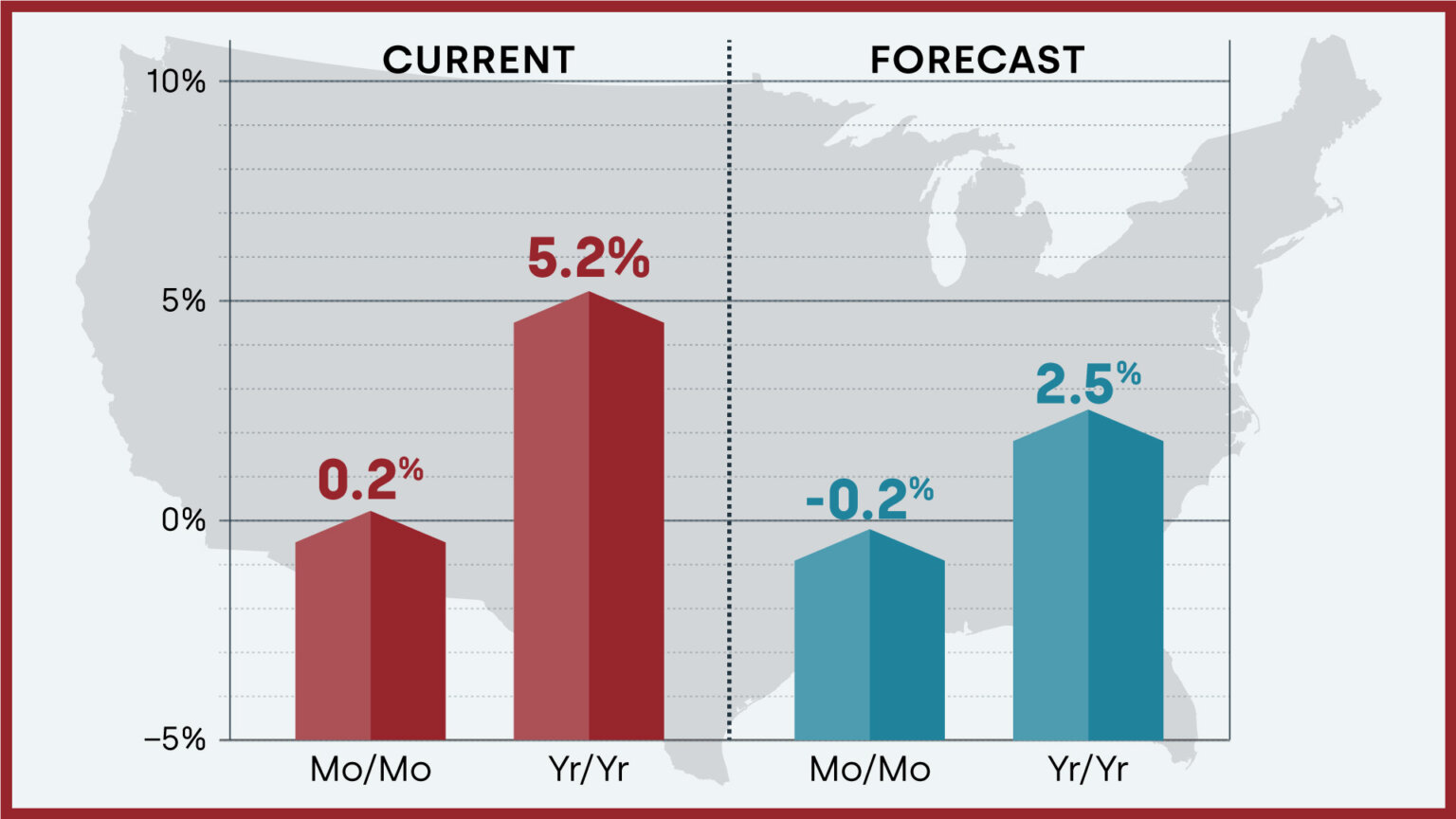

Over the last several quarters, the resilience of the housing market has been a subject of discussion among economists and analysts. The Federal Housing Finance Agency (FHFA) recently reported that U.S. house prices rose 5.7 percent between the second quarter of 2023 and the second quarter of 2024, marking a notable year-over-year growth trend.

Conversely, the FHFA noted a 0.1 percent decline in their seasonally adjusted monthly index for June when compared to May. This duality of trends—steadfast annual appreciation paired with minor quarterly fluctuations—points to a complex housing market scenario where underlying economic factors such as interest rates and inventory levels play a pivotal role.

Current State of the Housing Market

The current housing market demonstrates a series of intricate patterns, affected by various macroeconomic conditions. Interest rates remain elevated, contributing to increased mortgage costs for potential buyers. This scenario has resulted in a unique set of challenges, particularly for first-time buyers and those looking to upgrade their living situations.

According to Dr. Anju Vajja, Deputy Director at FHFA, “The slower pace of appreciation as of June end was likely due to higher inventory of homes for sale and elevated mortgage rates.” This statement encapsulates the intricate relationship between supply and demand in the housing sector. With more homes entering the market, buyers have a wider array of options, which, combined with higher borrowing costs, tempers the fierce competition that characterized earlier market phases.

Regional Insights on Housing Market Trends

When examining housing market trends, it is essential to consider geographical distinctions. Across the United States, we see substantial variation in house price appreciation among states and metropolitan areas. Notably, all 50 states and the District of Columbia recorded increases in house prices from 2023 to 2024. States like Vermont, West Virginia, and Rhode Island have outperformed others, with appreciation rates of 13.4 percent, 12.3 percent, and 10.1 percent, respectively.

Conversely, some markets exhibit contrasting trends. For example, the Austin-Round Rock-Georgetown area in Texas noted a 3.2 percent decline in housing prices over the past year. Understanding these nuances is critical for investors and homebuyers who must navigate varying market conditions depending on their specific regions of interest.

Metropolitan Areas and Their Trends

Delving deeper into housing market trends in metropolitan areas reveals significant insights about urban centers. The report indicates that 96 of the top 100 largest metropolitan areas in the United States experienced price increases, reflecting a robust demand for housing in these locations. Syracuse, NY recorded the most substantial annual price appreciation at 14.2 percent, which begs the question of what drives such demand in particular cities.

Analysts note that factors contributing to significant price movements in metropolitan areas often include local economic conditions, job opportunities, and demographic shifts. For instance, as remote work becomes more mainstream, many individuals are inclined to migrate to locations with lower living costs and abundant amenities, often leading to increased demand in those markets.

The Shift in Buyer Behavior

Amid the evolving housing market trends, buyer behavior has also shifted in response to economic factors such as mortgage rates and inflation. First-time homebuyers are particularly burdened by the current interest rates, which have substantially increased borrowing costs. Consequently, many potential buyers have adjusted their expectations regarding price points and the type of homes they can afford.

Affordability remains a pressing concern, compelling buyers to reevaluate their strategies. Those seeking affordable housing may be inclined to consider areas outside traditional urban centers, pursuing suburban markets or even rural settings that offer more value for their investment. However, this shift does not come without its challenges, as many suburban areas are also experiencing rising prices due to increased demand.

Inventory Dynamics in the Housing Market

A pivotal aspect of housing market trends is the inventory of homes available for sale. The dynamic of higher inventory levels has initiated a slowdown in the pace of price appreciation. According to the FHFA, the increased supply coupled with elevated mortgage rates signifies a transitional phase within the market. Home sellers may need to remain flexible in their pricing strategies as potential buyers weigh the implications of financing their purchases in a higher interest rate environment.

As of the latest reports, the Middle Atlantic region shows the strongest appreciation among census divisions, boasting an 8.5 percent increase. In contrast, the West South Central division recorded the least amount of change, with only a 2.8 percent increase. These disparities illustrate the complex interplay between local economies and housing supply-demand dynamics.

The Future of Housing Market

Looking forward, the housing market is positioned to face continued scrutiny as economists predict a range of outcomes influenced by interest rates, inflation, and job growth. While positive annual appreciation is expected to persist, particularly in states with increasing demand, the rate of growth may slow down due to external economic pressures.

As homeowners, investors, and policymakers monitor these variables, the ongoing dialogue about housing market trends will remain relevant and critical for informed decision-making. Everyone from first-time buyers to seasoned investors will have to navigate a market that continues to evolve, influenced by larger economic patterns and localized shifts.

In summary, the housing market as of 2024 is demonstrating both resilience and complexity, with regional variances, changing buyer behaviors, and inventory challenges that complicate traditional narratives. As stakeholders engage with these trends, their strategies and decisions will need to reflect an understanding of the underlying economic and social factors at play.

ALSO READ:

- Housing Market Predictions for the Next 4 Years: 2024 to 2028

- Real Estate Forecast Next 5 Years: Top 5 Predictions for Future

- Is the Housing Market on the Brink in 2024: Crash or Boom?

- 2008 Forecaster Warns: Housing Market 2024 Needs This to Survive

- Housing Market Predictions for the Next 2 Years

- Real Estate Forecast Next 10 Years: Will Prices Skyrocket?

- Housing Market Predictions for Next 5 Years (2024-2028)

- Housing Market Predictions 2024: Will Real Estate Crash?

- Housing Market Predictions: 8 of Next 10 Years Poised for Gains

- Trump vs Harris: Which Candidate Holds the Key to the Housing Market (Prediction)