On August 7, 2025, mortgage rates have shown a marginal drop from last week across all segments, with the national average 30-year fixed mortgage rate decreasing to 6.70% from 6.82%. This slight dip provides a bit of relief to homebuyers who have been grappling with historically high rates over the last couple of years.

Refinancing rates, however, show mixed results with the 30-year fixed refinance rate inching up slightly to 6.98% but still down from previous highs. Understanding these trends in mortgage and refinance rates can help buyers and homeowners make informed decisions today.

Today's Mortgage Rates – August 7, 2025: Rates Drop Consistently Across All Segments

Key Takeaways

- 30-year fixed mortgage rates dropped slightly to 6.70%, down 12 basis points from last week.

- 15-year fixed mortgage rates increased marginally to 5.75%.

- 5-year ARM mortgage rates slightly decreased to 7.18%.

- Mortgage applications rose by 3.1% as rates fell, according to Mortgage Bankers Association.

- 30-year fixed refinance rates slightly increased to 6.98%, but are still down 5 basis points from last week.

- Federal Reserve monetary policy continues to influence rates, with potential cuts expected later in 2025.

Current Mortgage and Refinance Rates: August 7, 2025

Understanding today's mortgage and refinance rates is key for anyone thinking about purchasing a home or refinancing an existing mortgage. Rates vary by loan type and term, influenced heavily by Federal Reserve decisions and market conditions.

| Loan Type | Current Rate | Weekly Change | APR | Weekly APR Change |

|---|---|---|---|---|

| 30-Year Fixed | 6.70% | Down 0.13% | 7.21% | Down 0.07% |

| 20-Year Fixed | 6.41% | Down 0.05% | 6.80% | Down 0.13% |

| 15-Year Fixed | 5.75% | Down 0.13% | 6.08% | Down 0.09% |

| 10-Year Fixed | 5.48% | Down 0.26% | 5.84% | Down 0.28% |

| 7-Year ARM | 7.08% | Down 0.14% | 7.59% | Down 0.29% |

| 5-Year ARM | 7.18% | Down 0.36% | 7.84% | Down 0.07% |

Government Loans Mortgage Rates

| Loan Type | Current Rate | Weekly Change | APR | Weekly APR Change |

|---|---|---|---|---|

| 30-Year Fixed FHA | 6.91% | Down 0.29% | 7.93% | Down 0.30% |

| 30-Year Fixed VA | 6.40% | Up 0.11% | 6.62% | Up 0.12% |

| 15-Year Fixed FHA | 5.75% | Up 0.23% | 6.72% | Up 0.20% |

| 15-Year Fixed VA | 6.00% | Up 0.16% | 6.36% | Up 0.18% |

(Source: Zillow, August 7, 2025)

Refinance Rates Today

Refinancing rates have shown small fluctuations, with a slight increase in the average 30-year fixed refinance rate but a mixed trend in shorter terms.

| Loan Type | Current Rate | Weekly Change | APR | Weekly APR Change |

|---|---|---|---|---|

| 30-Year Fixed Refi | 6.98% | Up 0.03% | — | — |

| 15-Year Fixed Refi | 5.82% | Up 0.08% | — | — |

| 5-Year ARM Refi | 7.89% | Up 0.16% | — | — |

Understanding Why Mortgage Rates Matter in 2025

Mortgage rates heavily influence housing affordability. When rates rise, monthly payments increase, making homes less affordable for many buyers. Conversely, when rates fall or stabilize, more buyers find it feasible to enter the market. After years of rising rates that peaked near historic highs, the recent slight retreat signals potential good news for home buyers and those looking to refinance.

The Mortgage Bankers Association reports a 3.1% increase in mortgage applications following the recent dip in rates. This uptick reflects buyers seizing the opportunity to lock in lower rates before they potentially rise again.

The Federal Reserve's Role in Shaping Mortgage Rates

The Federal Reserve’s monetary policy is a critical factor behind the movement of mortgage rates. Since the pandemic, the Fed's actions have dramatically affected borrowing costs.

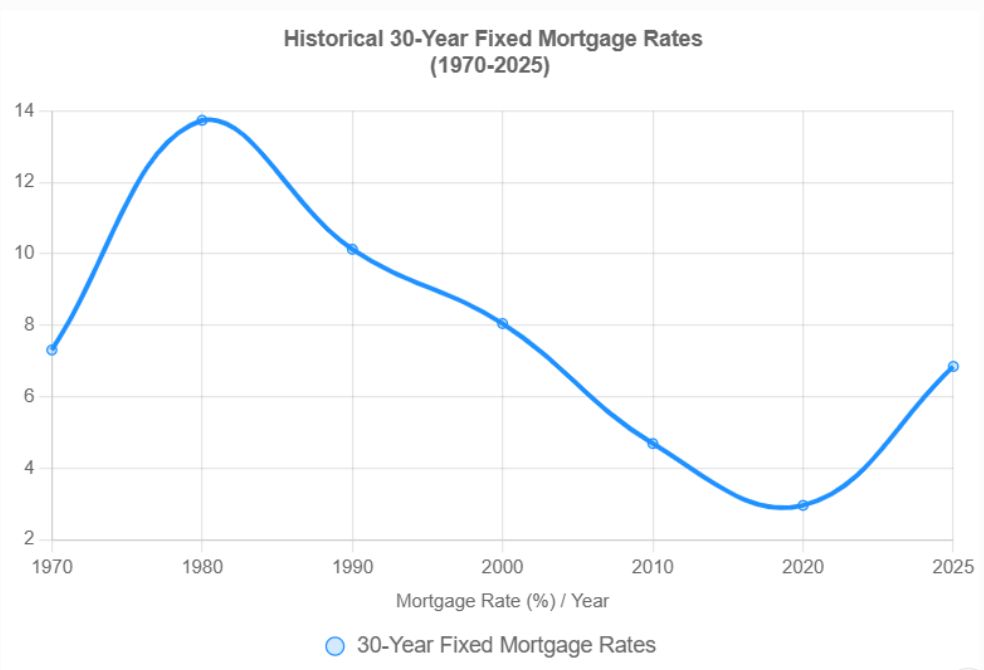

The Rate Journey from Pandemic to 2025

- 2021-2023: The Fed kept rates near zero to support recovery, causing mortgage rates to historically low levels.

- March 2022 – July 2023: The Fed aggressively increased the federal funds rate by 5.25 percentage points to fight inflation, pushing mortgage rates to around 7% and beyond—the highest in about 20 years.

- Late 2024: The Fed started cutting rates, signaling the beginning of easing monetary policy. By December 2024, rates were lowered by a full percentage point to 4.25%-4.5%.

- 2025: Since the rate cuts, the Fed has paused at these higher levels into mid-year, creating uncertainty and volatility in mortgage markets.

Despite no changes at the last five Fed meetings, internal divisions exist about when to cut rates further due to slowing economic growth and persistent inflation.

Related Topics:

Mortgage Rates Trends as of August 6, 2025

Mortgage Rates Predictions for the Next 30 Days: July 22-August 22

Economic Context and Mortgage Rates Forecast

- Inflation remains stubbornly above the Fed’s 2% target, particularly core prices impacting consumer goods and services.

- Economic growth has slowed to an annualized GDP rate of approximately 1.2% in the first half of 2025.

- Unemployment has crept upward to around 4.5%.

These mixed signals lead the Fed to hold rates steady while awaiting clearer economic data to adjust policy again.

Predictions include:

- Average mortgage rates expected to trend around 6.4% in H2 2025, with possible dips toward 6.1% in 2026 (National Association of REALTORS®).

- The Mortgage Bankers Association expects rates to remain near 6.7% by year-end 2025, with modest declines into 2026.

- The Federal Reserve might enact two rate cuts this year, which could lower mortgage rates closer to 6% by late 2025 or early 2026, but timing is uncertain.

What This Means for Homebuyers and Refinancers

Buyers remain challenged by rates near 7% for 30-year fixed loans, but recent declines suggest some relief may be coming. Refinancers with loans above 7% should watch closely for Fed moves later this year that could open opportunities for cost savings.

Example Mortgage Payment Calculation (30-Year Fixed Loan at 6.7%)

To illustrate, consider a conventional 30-year fixed mortgage of $300,000 at today's average rate of 6.7%:

- Monthly principal and interest payment = $1,939.37

- Total payments over 30 years = $1,939.37 × 360 months = $698,173.20

Compare that with last week's average rate of 6.82% for the same loan:

- Monthly payment = $1,948.10

- Total paid over 30 years = $701,316

The slight rate drop saves almost $9 monthly and about $3,143 in interest over the life of the loan.

Long-Term Trends and What to Watch

- The Fed’s cautious approach and uncertain economic outlook suggest rates will hover near current levels for some months.

- Inflation pressures continue to create upward risk, while slowing growth pressures push rates downward.

- Real GDP forecasts of 1.4% growth in 2025 and 2.2% in 2026 point toward a slow recovery phase that could stabilize mortgage rates in the mid-6% range.

Summary Table: Mortgage Rate Trends August 7, 2025

| Metric | Current Rate | Weekly Change | Trend |

|---|---|---|---|

| 30-Year Fixed Mortgage | 6.70% | Down 0.12% | Slight Drop |

| 15-Year Fixed Mortgage | 5.75% | Up 0.02% | Slight Rise |

| 5-Year ARM Mortgage | 7.18% | Down 0.02% | Slight Drop |

| 30-Year Fixed Refi | 6.98% | Up 0.03% | Slight Rise |

| 15-Year Fixed Refi | 5.82% | Up 0.08% | Slight Rise |

| 5-Year ARM Refi | 7.89% | Up 0.16% | Moderate Rise |

Mortgage rates remain a pivotal factor for the real estate market in 2025. While recent small declines offer hope, the overall environment remains challenging. The Federal Reserve’s future decisions, inflation data, and economic growth will continue to be watched closely by borrowers and lenders alike.

Capitalize Amid Rising Mortgage Rates

With mortgage rates expected to remain high in 2025, it’s more important than ever to focus on strategic real estate investments that offer stability and passive income.

Norada delivers turnkey rental properties in resilient markets—helping you build steady cash flow and protect your wealth from borrowing cost volatility.

HOT NEW LISTINGS JUST ADDED!

Speak with a seasoned Norada investment counselor today (No Obligation):

(800) 611‑3060

Also Read:

- Will Mortgage Rates Go Down in 2025: Morgan Stanley's Forecast

- Mortgage Rate Predictions 2025 from 4 Leading Housing Experts

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?