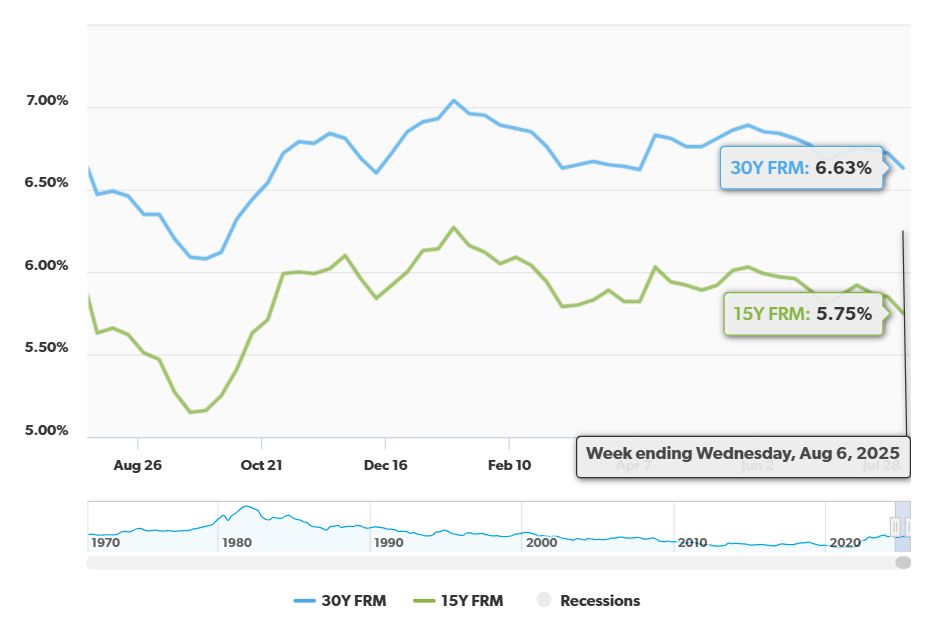

Good news for prospective homebuyers and those looking to refinance! As of today, August 10, 2025, the national average 30-year fixed mortgage rate has seen a modest dip. The 30-year FRM is sitting at 6.75%, a welcome decrease of 7 basis points from the previous week's average of 6.82%. But what does this really mean for you, and is this a sign of things to come? Let's dive in.

30-Year Mortgage Rate (FRM) Today: Drops by 7 Basis Points – August 10, 2025

What's Happening with Mortgage Rates Right Now?

It's important to get the full picture, so let's look beyond just the 30-year fixed-rate mortgage. Here's a quick snapshot of other key mortgage rates as of August 10, 2025, according to Zillow:

- 15-Year Fixed Rate: Increased slightly by 1 basis point to 5.80%.

- 5-Year ARM: Increased by 6 basis points to 7.40%.

Here is an exhaustive picture:

Conforming Loans

| PROGRAM | RATE | 1W CHANGE | APR | 1W CHANGE |

|---|---|---|---|---|

| 30-Year Fixed Rate | 6.75 % | down0.08 % | 7.08 % | down0.19 % |

| 20-Year Fixed Rate | 6.65 % | up0.19 % | 6.93 % | 0.00 % |

| 15-Year Fixed Rate | 5.80 % | down0.08 % | 6.02 % | down0.16 % |

| 10-Year Fixed Rate | 5.48 % | down0.26 % | 5.84 % | down0.28 % |

| 7-year ARM | 7.08 % | down0.14 % | 7.59 % | down0.29 % |

| 5-year ARM | 7.40 % | down0.14 % | 7.74 % | down0.17 % |

| 3-year ARM | — | 0.00 % | — | 0.00 % |

| Last updated: 8/10/2025 |

Government Loans

| PROGRAM | RATE | 1W CHANGE | APR | 1W CHANGE |

|---|---|---|---|---|

| 30-Year Fixed Rate FHA | 6.69 % | down0.51 % | 7.71 % | down0.52 % |

| 30-Year Fixed Rate VA | 6.30 % | up0.01 % | 6.52 % | up0.02 % |

| 15-Year Fixed Rate FHA | 5.49 % | down0.03 % | 6.45 % | down0.06 % |

| 15-Year Fixed Rate VA | 5.83 % | down0.01 % | 6.19 % | up0.01 % |

| Last updated: 8/10/2025 |

While the 30-year FRM has decreased, we can see a mixed bag of movement across different loan types.

Why Did the 30-Year Mortgage Rate Drop?

The 30-year mortgage rate is influenced by a myriad of economic factors, and it's rarely just one thing that causes movement, but one key factor is being driven by the Federal Reserve.

The Federal Reserve has a huge influence on rates, including mortgage rates. From March 2022-July 2023, aggressively raised rates to combat inflation, indirectly pushing mortgage rates up. Then the Fed cut rates three times in late 2024 (September to December).

2025 has been relatively still, it has held rates steady for five consecutive meetings in 2025 (through July 30), despite growing economic headwinds. Although no firm decision has been made, the Fed cutting rates later in 2025 would result in lower mortgage rates.

The Federal Reserve’s Role in Mortgage Rates and Monetary Policy: 2024-2025 Update

So, let's break down the recent history and future expectations from the Fed:

The Federal Reserve, through its monetary policy, is the biggest factor impacting mortgage rate trends.

- Pandemic Recovery to Rate Hike Cycle (2021-2023): The Fed’s pandemic-era bond purchases kept rates extremely low. Later, to combat rising inflation, the Fed aggressively hiked the federal funds rate.

- The Pivot to Cuts (Late 2024): After holding rates steady for 14 months, The Fed cut rates three times in late 2024 (September to December).

- 2025: A Year of Waiting and Uncertainty: The Fed has now held rates steady for five consecutive meetings.

- Internal Divisions: The July 30 decision saw a 9-2 vote, with dissents from Governors Bowman and Waller advocating for immediate cuts to address slowing growth. But the majority wants to wait.

- Economic Crosscurrents:

- Inflation Stubbornness: Core PCE remains elevated at ~2.7%, with new tariff pressures complicating the outlook. It's proving difficult to tame.

- Growth Slowdown: GDP growth has decelerated to ~1.2% annualized in H1 2025, with unemployment creeping up to 4.5%. The economy needs a boost.

How Does This Affect You?

Ultimately, the recent drop of 7 basis points in the 30-year FRM is a positive sign for the housing market. Here's what this could mean for different groups:

- For Homebuyers: Any decrease in mortgage rates makes homeownership more affordable. Even a small reduction can translate to significant savings over the life of a 30-year mortgage. Run the numbers and see what you can afford!

- For Those Looking to Refinance: If you're currently holding a mortgage with a higher interest rate, this dip could be an opportunity to refinance and lower your monthly payments.

- For Everyone Else: Even if you're not actively buying or refinancing, lower mortgage rates generally stimulate the economy, which can benefit everyone.

Mortgage Rate Impact

- 30-year fixed rates have hovered near 6.8% through mid-2025, with modest declines expected later this year if cuts materialize.

- The Fed’s projected two cuts in 2025 (per June “dot plot”) could eventually pull mortgage rates toward 6% by year-end, though timing remains uncertain.

What’s Next? Key Dates and Scenarios

- September 16-17 Meeting: The next critical juncture, with updated economic projections. Market odds of a cut currently stand at 47%.

- December Meeting: Likely the Fed’s last realistic 2025 cut opportunity if September passes without action.

- Long-Term Outlook: The Fed anticipates gradual easing, with rates potentially settling near 2.25%-2.5% by 2027.

Why This Matters for Borrowers

- Current Buyers: High rates persist, but Fed signals suggest relief may come in late 2025/early 2026.

- Refinancers: Those with rates above 7% should monitor September/December Fed decisions for potential opportunities.

- Investors: Bond markets remain volatile, with the 10-year Treasury yield sensitive to Fed rhetoric (currently 4.34%).

Related Topics:

30-Year Fixed Mortgage Rate (FRM) Trends – August 9, 2025

Mortgage Rates Predictions for the Next 30 Days: July 22-August 22

Looking Ahead: What to Expect From Mortgage Rates

Predicting the future is always tricky, but here are some factors to keep an eye on:

- The Federal Reserve's Actions: The Fed's decisions regarding interest rates will continue to be a primary driver of mortgage rates. Pay attention to their meetings and announcements.

- Inflation: If inflation remains high, the Fed may be hesitant to lower interest rates, which could keep mortgage rates elevated.

- Economic Growth: A strong economy could lead to higher interest rates, while a weaker economy could push them lower. It's a delicate balancing act.

- Geopolitical Events: Unexpected global events can also impact financial markets and influence mortgage rates.

My Advice

While a 7 basis point drop is a welcome sign, it's important to remember that mortgage rates can fluctuate. If you're considering buying or refinancing, now is a good time to shop around and compare rates from different lenders. Don't just focus on the interest rate; also consider the fees and closing costs associated with the loan.

Capitalize Amid Rising Mortgage Rates

With mortgage rates expected to remain high in 2025, it’s more important than ever to focus on strategic real estate investments that offer stability and passive income.

Norada delivers turnkey rental properties in resilient markets—helping you build steady cash flow and protect your wealth from borrowing cost volatility.

HOT NEW LISTINGS JUST ADDED!

Speak with a seasoned Norada investment counselor today (No Obligation):

(800) 611‑3060

Also Read:

- Will Mortgage Rates Go Down in 2025: Morgan Stanley's Forecast

- Mortgage Rate Predictions 2025 from 4 Leading Housing Experts

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?