Today, March 19, 2025, the mortgage market is showing very little movement as everyone waits to hear from the Federal Reserve. While some mortgage rates have nudged up a tiny bit and others have dipped slightly, it's mostly a steady day. Let's dive into the details of where mortgage rates stand right now.

Mortgage Rates Today, March 19, 2025: Rates Inch Up and Down as Market Awaits Fed's Next Move

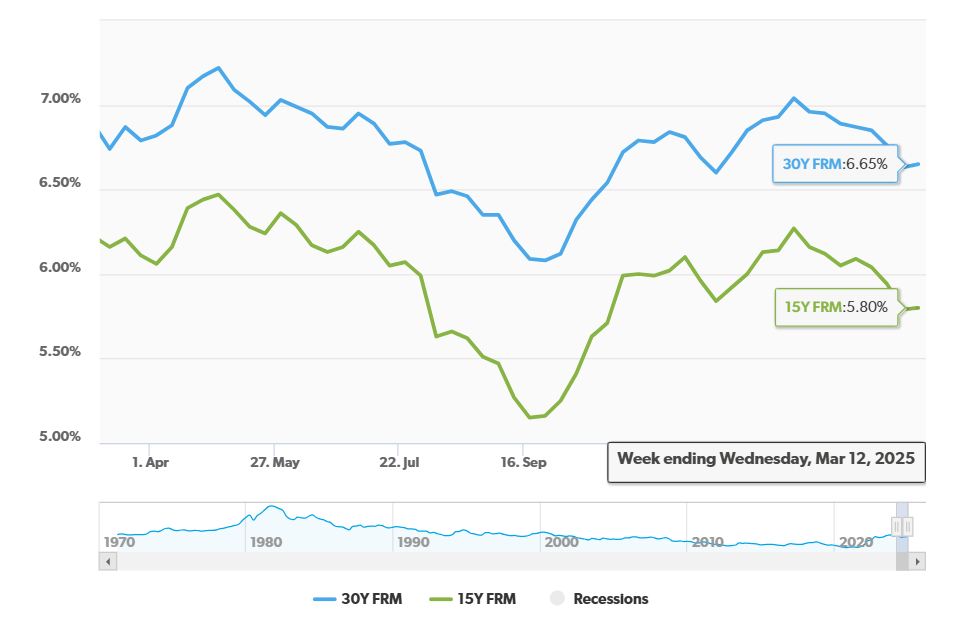

Key Takeaways

- 30-Year Fixed Mortgage Rate: Slightly increased to 6.59%, up by just two basis points.

- 15-Year Fixed Mortgage Rate: Decreased a little to 5.99%, down by two basis points.

- Federal Reserve Impact: The market is holding its breath for the Federal Reserve's meeting today. No changes to the federal funds rate are expected, but what Fed Chair Jerome Powell says about the economy could push mortgage rates up or down.

- Rate Volatility: Mortgage rates are still a bit shaky because of economic uncertainty.

Current Mortgage Rates on March 19, 2025

If you're looking to buy a home, understanding today's mortgage rates is crucial for figuring out your budget. Here’s a snapshot of the national average rates as of today, March 19, 2025, according to the latest data from Zillow:

| Loan Type | Interest Rate |

|---|---|

| 30-Year Fixed | 6.59% |

| 20-Year Fixed | 6.49% |

| 15-Year Fixed | 5.99% |

| 5/1 ARM | 6.68% |

| 7/1 ARM | 6.88% |

| 30-Year VA | 6.15% |

| 15-Year VA | 5.67% |

| 5/1 VA | 6.16% |

Note: These are national averages and can vary based on your location and personal financial situation. Rates are rounded to the nearest hundredth.

Refinance Rates Today, March 19, 2025

Thinking about refinancing your current mortgage? Refinancing can help you lower your monthly payments or shorten your loan term. Here are today's average refinance rates, also from Zillow:

| Loan Type | Interest Rate |

|---|---|

| 30-Year Fixed | 6.68% |

| 20-Year Fixed | 6.33% |

| 15-Year Fixed | 6.08% |

| 5/1 ARM | 6.80% |

| 7/1 ARM | 6.85% |

| 30-Year VA | 6.22% |

| 15-Year VA | 5.90% |

| 5/1 VA | 6.21% |

| 30-Year FHA | 6.21% |

| 15-Year FHA | 5.73% |

Note: These are national averages and can vary. Refinance rates can sometimes be a bit higher than purchase rates.

Understanding 30-Year Fixed Mortgage Payments

The 30-year fixed-rate mortgage is a popular choice for homebuyers because it offers stable, predictable monthly payments over a long period. This makes budgeting easier. However, it's important to understand how today's rates translate into actual monthly payments. Let's look at some examples of different loan amounts.

Monthly Payment on a $150,000 Mortgage

If you were to take out a $150,000 mortgage at today's 30-year fixed rate of 6.59%, your estimated monthly payment would be around $954. This payment covers just the principal and interest. You'll also need to factor in property taxes and homeowners insurance, which will increase your total monthly housing cost.

Monthly Payment on a $200,000 Mortgage

For a $200,000 mortgage at 6.59%, your estimated monthly payment would be approximately $1,272 for principal and interest. Remember, this is before adding in other homeownership expenses like taxes and insurance.

Monthly Payment on a $300,000 Mortgage

Stepping up to a $300,000 mortgage at the same 6.59% rate, you're looking at a monthly payment of roughly $1,908 for principal and interest. As the loan amount increases, so does your monthly financial commitment.

Monthly Payment on a $400,000 Mortgage

A $400,000 mortgage at 6.59% would result in an estimated monthly payment of $2,544 for principal and interest. It's essential to consider if this payment fits comfortably within your monthly budget.

Monthly Payment on a $500,000 Mortgage

Finally, for a $500,000 mortgage at 6.59%, the estimated monthly payment comes to around $3,180 for principal and interest. This example highlights how significantly mortgage payments can vary based on the loan amount.

These calculations are just estimates and don't include property taxes, homeowners insurance, or potentially private mortgage insurance (PMI) if your down payment is less than 20%. Using a mortgage calculator can give you a more complete picture by including these additional costs.

Recommended Read:

Mortgage Rates Trends as of March 18, 2025

Mortgage Rates Drop: Can You Finally Afford a $400,000 Home?

Expect High Mortgage Rates Until 2026: Fannie Mae's 2-Year Forecast

Factors Influencing Today's Mortgage Rates

Why are mortgage rates doing what they're doing today? A big part of it is the Federal Reserve. The Fed meeting happening today is a major event for the financial markets. Even though experts expect the Fed to hold steady on the federal funds rate right now, everyone is listening closely to Fed Chair Powell's comments. His words about the economy and any hints about future interest rate cuts could quickly change the direction of mortgage rates.

Mortgage rates are closely tied to the bond market, and right now, there's a lot of uncertainty in the air. Economic concerns, like potential recession worries and unclear trade policies, are keeping pressure on the financial markets. This week, investors are especially focused on the Fed's interest rate forecast.

According to experts, mortgage rates have been a bit “unsteady” recently. We saw a period where they were slowly decreasing, but that trend has paused in the last couple of weeks. This kind of fluctuation is normal when the economic outlook is unclear.

Looking Ahead: Will Rates Go Down?

Many experts predict that mortgage rates will likely decrease by the end of 2025. Fannie Mae, for example, projects that rates will probably stay above 6.5% for much of this year, but could come down later. However, predictions are just that – predictions. The economy is complex, and many things can influence where rates go.

If the economy weakens significantly, mortgage rates could start to fall more noticeably, perhaps even closer to 5.5% to really boost buyer activity. Lower rates are generally good for housing affordability, but a struggling economy can also dampen the housing market. If rates drop because of a recession, people might still be hesitant to buy homes if they're worried about job security.

Adjustable-Rate Mortgages (ARMs)

Besides fixed-rate mortgages, adjustable-rate mortgages (ARMs) are another option. ARMs usually start with a lower interest rate for a set period, like 5 or 7 years (that’s where the “5/1 ARM” or “7/1 ARM” names come from). After that initial period, the interest rate can change, usually once a year.

The initial lower rate on an ARM can make monthly payments more affordable in the beginning. However, the risk is that rates could increase later, making your payments go up. ARMs can be a good choice if you plan to move or refinance before the fixed-rate period ends. But if you plan to stay in your home long-term, the uncertainty of rate changes can be a drawback.

In Conclusion

Today's mortgage rates are barely budging as the market waits for signals from the Federal Reserve. While rates remain around the 6.5% range for a 30-year fixed mortgage, small daily changes are happening. Keeping an eye on economic news and Fed announcements will be key to understanding where mortgage rates might be headed in the coming weeks and months. For now, if you're in the market to buy or refinance, it's a good time to talk to a lender and explore your options based on these current rates.

Work With Norada, Your Trusted Source for

Real Estate Investments

With mortgage rates fluctuating, investing in turnkey real estate

can help you secure consistent returns.

Expand your portfolio confidently, even in a shifting interest rate environment.

Speak with our expert investment counselors (No Obligation):

(800) 611-3060

Read More:

- Will Mortgage Rates Go Down in 2025: Morgan Stanley's Forecast

- Mortgage Rate Predictions 2025 from 4 Leading Housing Experts

- Mortgage Rates Forecast for the Next 3 Years: 2025 to 2027

- 30-Year Mortgage Rate Forecast for the Next 5 Years

- 15-Year Mortgage Rate Forecast for the Next 5 Years

- Why Are Mortgage Rates Going Up in 2025: Will Rates Drop?

- Why Are Mortgage Rates So High and Predictions for 2025

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?