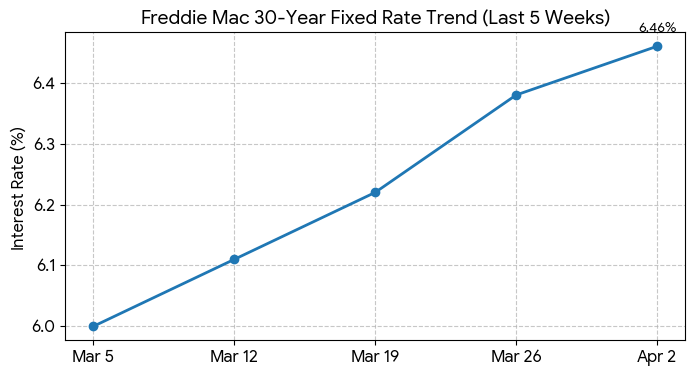

Good news for homeowners looking to potentially lower their monthly payments: on Sunday, April 5, 2026, mortgage refinance rates have seen a slight dip. Specifically, the average 30-year fixed refinance rate has dropped by 5 basis points, now sitting at 6.80%, according to Zillow. This small but welcome decrease comes after a period of some back-and-forth in the market.

Mortgage Rates Today – April 5, 2026: 30-Year Refinance Rate Drops by 5 Basis Points

What's Happening with Refinance Rates Right Now?

Let's break down the numbers from Zillow for today, April 5, 2026:

- 30-Year Fixed Refinance: This is the most common type of mortgage. Today, the average rate is 6.80%. It’s down from last week’s average of 6.85%, which is a 5 basis point improvement. Over the lifespan of a mortgage, even small drops like this can save you a good chunk of money.

- 15-Year Fixed Refinance: If you're looking to pay off your mortgage faster, the 15-year fixed rate has seen a more significant drop, moving down 8 basis points to 5.75%. This is a great option for those who can handle a higher monthly payment but want to be mortgage-free sooner.

- 5-Year Adjustable-Rate Mortgage (ARM): For those who don't mind a rate that could change down the line, the 5-year ARM refinance rate is holding steady at 6.00%. ARMs often start with lower rates than fixed mortgages, but it's important to remember they can go up after the initial fixed period.

Will People Rush to Refinance?

Even though rates have ticked down a bit, I'm not seeing the frenzy of activity that some might expect. The data from Zillow shows that refinance application demand has actually softened considerably over the past month. What gives?

- Monthly Demand Decline: Applications have dropped by about 40% in the last month. This happened as rates climbed almost 40 basis points since late February. When rates climb, people tend to hold off, hoping they’ll go back down.

- Weekly Trends: For the week ending March 27th, the total dollar amount of refinance applications was down by 18.3% compared to the week before.

- Looking Back: Now, it’s important to remember where we were last year. Even with this recent slowdown, the number of people applying to refinance is still 21% to 33% higher than this time last year. That’s because rates were much higher back then.

- Refinance Share: Right now, refinances make up just under half, 49.6%, of all mortgage applications. Back in mid-January, this number was closer to 60%.

This tells me that while the recent drop is good news, many people are still sitting on the sidelines, carefully watching the market. We’re not in a wild refinance boom, but rather a more cautious environment.

What's Driving These Rate Movements?

Several big events are keeping the mortgage rate market on its toes:

- Global Tensions: The ongoing geopolitical situation, particularly the conflict involving Iran, has been a major player. This has caused oil prices to go up, which in turn makes people worry more about inflation. When inflation concerns rise, Treasury yields tend to go up, and mortgage rates closely follow those yields. It’s a chain reaction that can make borrowing more expensive.

- Who's “In the Money”? Think about the folks who bought homes between 2023 and 2025. During those years, mortgage rates were often hovering around the 7% mark. For these homeowners, even a small dip towards 6% or the current 6.80% can be enough to make a rate-and-term refinance worthwhile – meaning they’re refinancing to get a better rate and/or term for their existing mortgage balance.

- Tapping Home Equity Differently: Since refinance rates are still relatively high compared to a few years ago, many homeowners are looking for alternatives to a cash-out refinance. Instead, they're turning to Home Equity Lines of Credit (HELOCs), which currently have an average rate around 7.20%, or traditional home equity loans. This allows them to access the wealth they've built up in their homes without giving up the very low interest rate they might have secured on their first mortgage a few years back. I see this as a smart move for many; why give up a 3% or 4% first mortgage if you don't absolutely have to?

- Mixed Signals for the Future: What's next? The experts have different ideas:

- Fannie Mae is predicting that rates could actually drop below 6% by the end of the year. This is an optimistic outlook, but it hinges on inflation calming down.

- However, the Mortgage Bankers Association (MBA) has recently updated their own predictions. They now believe rates will stay above 6% throughout 2026. This suggests a more cautious approach, anticipating that inflation might be stickier.

My Takeaway for You

As of April 5, 2026, we're seeing a modest breather in refinance rates, with the 30-year fixed at 6.80% and the 15-year fixed at 5.75%. While this is a positive movement from last week, the overall demand for refinancing isn't what it could be. Many homeowners are in a tough spot: they might have a low rate already, or they're waiting to see if rates will drop even further.

For those who bought homes when rates were quite high (say, 2023-2025), these current rates still offer a chance to save some money each month. But if you already secured a rate well below 5%, refinancing now might not make financial sense. The smart play, for many, is to explore options like HELOCs or home equity loans if you need to tap into your home's equity, preserving that fantastic first mortgage rate.

It really boils down to your individual situation and what your financial goals are. Keeping an eye on these numbers and understanding the bigger economic picture will help you make the best decision for your home and your wallet.

VS

Georgia’s affordable rental with higher cap rate vs Florida’s A‑rated property with stability. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Market forecasts suggest steady demand, making turnkey real estate one of the most reliable paths to passive income and wealth creation.

Norada Real Estate helps investors capitalize on these trends with turnkey rental properties designed for appreciation and consistent cash flow—so you can grow wealth securely while others wait for clarity in the market.

Recommended Read:

- 30-Year Fixed Refinance Rate Trends – March 22, 2026

- Best Time to Refinance Your Mortgage: Expert Insights

- Should You Refinance Your Mortgage Now or Wait Until 2026?

- When You Refinance a Mortgage Do the 30 Years Start Over?

- Should You Refinance as Mortgage Rates Reach Lowest Level in Over a Year?

- Half of Recent Home Buyers Got Mortgage Rates Below 5%

- Mortgage Rates Need to Drop by 2% Before Buying Spree Begins

- Will Mortgage Rates Ever Be 3% Again: Future Outlook

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years