Today, April 2, 2026, marks a subtle shift in the refinance market, as the popular 30-year fixed refinance rate has dipped by 4 basis points week-over-week, settling at an average of 6.81%, according to Zillow. While this might seem like a small step, for homeowners looking to adjust their current mortgages, it's a breath of fresh air in a period of persistent rate pressure.

Mortgage Rates Today, April 2, 2026: 30-Year Refinance Rate Drops by 4 Basis Points

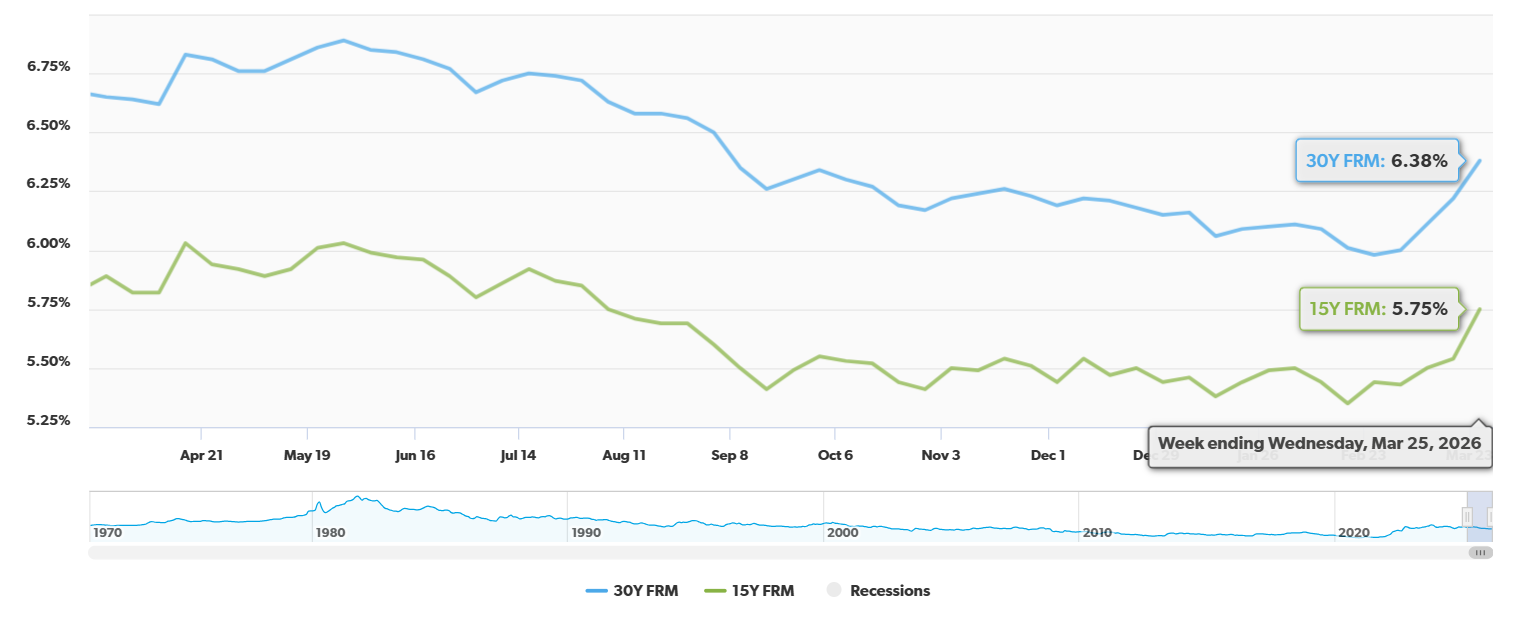

What's Happening with Refinance Rates Today?

Let's break down the numbers from Zillow for April 2, 2026:

- 30-Year Fixed Refinance: Currently averaging around 6.81%. This is actually up a hair from yesterday (by 2 basis points), but the important story is that it's down 4 basis points compared to where we were just last week, when the average was closer to 6.85%.

- 15-Year Fixed Refinance: These rates are holding steady at a solid 5.83%.

- 5-Year Adjustable-Rate Mortgage (ARM) Refinance: These are also staying put at 5.94%.

As you can see, it's a mixed bag. The 30-year is the one making waves today, offering a small bit of relief. The others are playing it cool, staying put.

Why Are Rates Moving (or Not Moving)?

My experience tells me that mortgage rates don't just wake up and decide to go up or down. There are real forces at play. Today, it seems like a few things are creating this mixed picture:

- Geopolitical Shakes: We've all been watching the news about the Middle East. When conflict heats up there, oil prices tend to climb. Higher oil prices can make people worry about inflation, and that worry often pushes up something called Treasury yields. Mortgages tend to follow Treasury yields pretty closely, so this is a big factor.

- The Fed's Watchful Eye: The Federal Reserve, our central bank, decided to keep its main interest rate on hold again in March. We're talking about a range of 3.50%–3.75%. The general feeling now is that they plan to keep rates higher for longer, prioritizing getting inflation under control before they even think about lowering them. This sentiment definitely puts a lid on how much mortgage rates can drop.

- A Bit More Room to Breathe (For Some): In some housing markets, we're starting to see a little more inventory – more houses for sale. This can be good news for buyers and potentially create more opportunities for homeowners considering a refinance. However, general economic uncertainty still has people feeling a bit cautious.

Refinance Demand: Cooling Off?

I've noticed a trend, and the data backs it up: fewer people are rushing to refinance right now. It makes sense when rates are hovering near recent highs.

- A Big Weekly Slip: Applications for refinancing dropped by a significant 17% in the week ending March 27th, according to the Mortgage Bankers Association.

- Monthly Slide: Looking at the whole month, refinance demand is down about 40%. That’s a pretty steep drop, as rates have climbed nearly half a percent in that time.

- Refi's Slice of the Pie: Refinancing now makes up 45.3% of all mortgage activity. Last week, it was a bit higher, at 49.6%.

- Still Better Than Last Year: Even with this recent dip, it's worth remembering that refinance activity is still much stronger – somewhere between 33% and 52% higher – than it was this time last year, in 2025, when rates were even higher.

It’s a delicate balance. While fewer people are refinancing this week or this month, the overall interest compared to a year ago is still significant.

What Experts Are Saying About the Future

Predicting mortgage rates is notoriously tricky, and experts are all over the map. Here's a glimpse of what some are forecasting for the rest of 2026:

- Fannie Mae: They're optimistic that if inflation calms down, we could see rates dip below 6% later in the year.

- Mortgage Bankers Association (MBA): Their outlook is a bit more conservative, expecting rates to likely hang out between 6.1% and 6.3% for the remainder of 2026.

- Morgan Stanley: They're playing the long game, predicting a potential drop to 5.50%–5.75% by the middle of 2026. However, they also see a strong possibility of rates climbing back up in the latter half of the year.

As you can see, there's no crystal ball. Some see potential dips, while others believe rates will stick around higher levels or even creep back up. This uncertainty is precisely why staying informed is so crucial.

My Takeaway for You

So, what does this all mean for you, the homeowner? Today, April 2, 2026, we're seeing a slight improvement in the 30-year fixed refinance rate, bringing it down to 6.81%. While this is a welcome change from last week, it's happening in an environment where overall refinancing hasn't been as strong.

The economic climate, including inflation worries and global events, continues to make interest rates a bit jumpy. The Federal Reserve's stance also suggests we might not see dramatic rate drops anytime soon.

If you've been thinking about refinancing, now might be a good time to explore your options. That 4-basis-point dip, while modest, could make a difference for your monthly payment. However, it's essential to weigh that against the broader economic picture and the forecasts for the rest of the year. Keep an eye on those inflation reports, what the Fed says, and any major global developments. These are the things that really shape where mortgage rates will go next.

VS

Georgia’s affordable rental with higher cap rate vs Florida’s A‑rated property with stability. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Market forecasts suggest steady demand, making turnkey real estate one of the most reliable paths to passive income and wealth creation.

Norada Real Estate helps investors capitalize on these trends with turnkey rental properties designed for appreciation and consistent cash flow—so you can grow wealth securely while others wait for clarity in the market.

Recommended Read:

- 30-Year Fixed Refinance Rate Trends – March 22, 2026

- Best Time to Refinance Your Mortgage: Expert Insights

- Should You Refinance Your Mortgage Now or Wait Until 2026?

- When You Refinance a Mortgage Do the 30 Years Start Over?

- Should You Refinance as Mortgage Rates Reach Lowest Level in Over a Year?

- Half of Recent Home Buyers Got Mortgage Rates Below 5%

- Mortgage Rates Need to Drop by 2% Before Buying Spree Begins

- Will Mortgage Rates Ever Be 3% Again: Future Outlook

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years