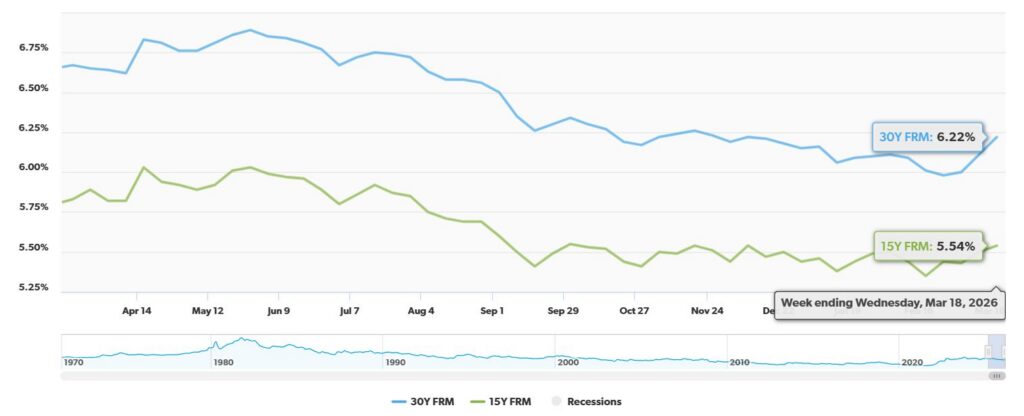

As of today, March 25, 2026, there's a welcome, albeit small, bit of good news for anyone eyeing a new home or thinking about refinancing: mortgage rates have taken a slight dip. Following a week of climbing prices, we're seeing a little relief, with the 30-year fixed rate dropping to 6.29% and the 15-year fixed hitting 5.77%, according to Zillow. This is the first bit of breathing room in days, offering a sigh of relief to homebuyers and homeowners who’ve watched rates creep up to levels we haven’t seen since late last year.

Right now, the rates are being led by rising Treasury yields and some unsettling developments overseas, particularly in the Middle East. Even though the Federal Reserve made a decision to keep its key interest rate steady, the persistent worry about inflation, amplified by the surge in oil prices, is casting a long shadow over the mortgage market.

Today's Mortgage Rates, March 25: Rates Go Down as 30-Year Fixed Falls to 6.29%

Let’s break down the latest averages Zillow shared with us:

| Mortgage Type | Rate |

|---|---|

| 30-Year Fixed | 6.29% |

| 20-Year Fixed | 6.25% |

| 15-Year Fixed | 5.77% |

| 5/1 ARM | 6.35% |

| 7/1 ARM | 6.35% |

| 30-Year VA | 5.93% |

| 15-Year VA | 5.57% |

| 5/1 VA | 5.57% |

Looking at these numbers, it’s clear that while today’s drop is a positive sign, we’re still a far cry from the sub-6% days that felt pretty normal earlier this year.

The Forces Shaping Our Mortgage World

It’s never just one thing, is it? A few key players are really influencing where mortgage rates are heading, and I think it's important we look at them together:

- The Federal Reserve's Stance: The Fed held its ground at their March 17-18 meeting, keeping the federal funds rate between 3.50% and 3.75%. Now, they haven't signaled any immediate rate cuts, and that's a big part of why borrowing costs are staying put at these higher levels. They're watching inflation very closely, and until they feel it's truly under control, they're likely to remain cautious.

- Oil Prices and Inflation: This is a big one, and frankly, it’s a bit nerve-wracking. The recent events in Iran have pushed oil prices past the $100 per barrel mark. When oil goes up, everything from transportation to manufacturing costs tends to follow, creating what economists call “second-round effects” on inflation. This directly impacts the 10-year Treasury yield, which is a major benchmark that mortgage rates tend to mirror. So, while the Fed might be one piece of the puzzle, global events are having a significant ripple effect.

- Buyer Hesitation (and its Impact): It makes perfect sense – when rates go up, people tend to step back. We’ve seen mortgage application volume drop by over 10% in the past week. A good portion of that decline, about 15%, comes from homeowners who were thinking about refinancing but are now finding it less attractive with rates outside of that sweet spot we saw not too long ago. This cooling demand can, in theory, take some pressure off rates, but it’s a delicate balance.

My Gut Feeling and the Experts' Views for 2026

When I look ahead, I try to balance the immediate news with the bigger picture.

- In the Short Term: My feeling, and what many industry watchers are saying, is that rates will likely continue to be a bit unpredictable. We might see them hover in that mid-6% range for a while. This is until we get more clear direction from the Federal Reserve, or until the geopolitical situation in the Middle East calms down. Volatility can be tough for planning.

- Looking Towards Year-End: Most economists I follow are still predicting a gradual easing of rates by the end of 2026. For instance, folks at Fannie Mae and Bankrate are suggesting that if inflation continues to trend downward, we could see 30-year fixed rates nudging toward 6.1% or possibly even dipping slightly below 6.0%. This is the kind of outlook that makes me tell clients to look at their long-term goals, not just the daily headlines.

The Big Takeaway for Today

So, what’s the bottom line for March 25, 2026? Today’s small drop in mortgage rates is a welcome pause, like catching your breath during a challenging hike. However, the overall picture is still one where borrowing costs are higher than many hoped for at the start of the year, and global events are keeping things a bit uncertain.

If you’re someone who’s been dreaming of owning a home or is considering refinancing an existing mortgage, my advice is to start by looking at your personal financial situation and your long-term plans. While the future might bring lower rates, the current environment really calls for careful consideration. Weighing the costs of refinancing now against the potential savings down the road, or understanding the affordability of a new purchase at today’s rates, is crucial. It's about making a decision that feels right for you, not just reacting to the daily market flutter.

VS

Georgia’s affordable rental with higher cap rate vs Florida’s A‑rated property with stability. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?