This is potentially fantastic news for anyone dreaming of homeownership. The 30-year fixed mortgage rate has experienced a significant drop of 78 basis points compared to this time last year, now hovering near an approachable 6%. This substantial decrease offers a much-needed boost in affordability for prospective buyers and could invigorate the housing market as we head into the busy spring season.

30-Year Fixed Mortgage Rate Drops Steeply by 78 Basis Points

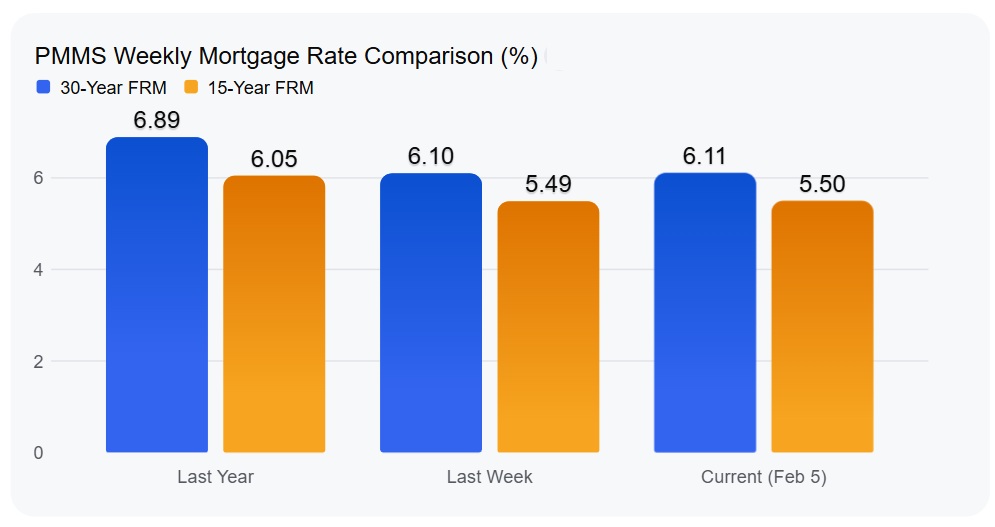

As of Thursday, February 5, 2026, a major shift has occurred in the mortgage world. Freddie Mac, a prominent player in the housing finance industry, has reported a steep decline of 78 basis points in the average 30-year fixed mortgage rate when compared to the same period last year. This isn't just a small nudge; it's a substantial move that could rewrite the financial plans of countless Americans. This particular drop from an average of 6.89% last year to a new average of 6.11% this year is incredibly significant. It means that buying power has just received a considerable injection.

Understanding What a Basis Point Actually Means

Before we dive deeper, let's clarify what “78 basis points” translates to in real dollars. A basis point is simply one-hundredth of a percentage point. So, 78 basis points equal 0.78%. This might not sound like a massive number on its own, but when applied to the large sums involved in a mortgage, it can add up to thousands, even tens of thousands, of dollars saved over the life of a loan.

Imagine you're looking at a $300,000 mortgage.

- At last year's rate of 6.89%, your monthly principal and interest payment would have been approximately $1,976.

- At this year's new rate of 6.11%, that payment drops to about $1,821.

That's a difference of $155 per month, or $1,860 per year in savings! Over a 30-year period, this translates to nearly $46,800 in interest savings. That's a considerable chunk of change that could go towards renovations, investments, or simply building wealth.

A Closer Look at the Numbers: The Latest Freddie Mac Data

Freddie Mac’s latest report, the Primary Mortgage Market Survey® (PMMS) for the week ending February 5, 2026, paints a clear picture.

| Loan Type | Current Rate (Feb 5, 2026) | 1-Wk Change | 1-Yr Change | Monthly Avg. | 52-Wk Avg. | 52-Wk Range |

|---|---|---|---|---|---|---|

| 30-Year Fixed | 6.11% | +0.01% | -0.78% | 6.09% | 6.51% | 6.06% – 6.89% |

| 15-Year Fixed | 5.50% | +0.01% | -0.55% | 5.45% | 5.71% | 5.38% – 6.09% |

As you can see, the 30-year fixed-rate mortgage (FRM) averaged 6.11%. This is a slight tick up from last week's 6.10%, but the year-over-year comparison is where the real story lies. The -0.78% change from last year is a powerful indicator of the current favorable environment for borrowers.

Even the 15-year fixed-rate mortgage has seen its own positive movement, dropping by 55 basis points year-over-year to an average of 5.50%. While the 30-year mortgage remains the most popular choice for its predictable payments and lower monthly costs, the 15-year option can save a significant amount in interest if you have the financial capacity for higher monthly payments.

Why Are Rates Dropping So Sharply?

It's natural to wonder what's driving such a significant drop. It's rarely just one factor, but rather a combination of economic forces.

The Influence of Monetary Policy

The Federal Reserve plays a crucial role in shaping interest rates. In a recent development, the Fed made the decision to pause interest rate cuts after lowering them three times towards the end of 2025. This pause offers a sense of stability. While the Fed isn't actively pushing rates lower right now, the impact of those previous cuts is still reverberating through the economy. Furthermore, the market anticipates that future policy decisions will likely lean towards keeping rates lower for a sustained period. This expectation itself can influence mortgage rates downwards.

Treasury Yields and the “Spread”

Mortgage rates are closely tied to the yields on U.S. Treasury bonds, particularly the 10-year Treasury note. This bond is often seen as a benchmark for long-term borrowing costs. While the 10-year Treasury yield has recently been hovering around 4.2%, something interesting is happening. The “spread” – the difference between Treasury yields and mortgage rates – has actually narrowed. This means that even though Treasury yields haven't plummeted, mortgage lenders are able to offer lower rates because the gap between what they pay for funds and what they charge borrowers has tightened. This is a bit technical, but it means less of a premium is being added to mortgage rates.

Looking Ahead: The Spring Home Sales Season

This sharp drop in rates is arriving at a critical time: the cusp of the spring home sales season. Freddie Mac's Chief Economist, Sam Khater, has pointed to a couple of key factors that make this a positive outlook:

- Improving Affordability: Lower mortgage rates directly translate to lower monthly payments, making homes more affordable for a larger segment of the population. This can bring buyers back into the market who may have been priced out previously.

- Increased Home Availability: Reports suggest that the supply of homes available for purchase is also on the rise. A greater selection of homes, combined with better affordability, creates a more balanced market that benefits both buyers and sellers. A balanced market is a healthy market.

Potential Challenges and What They Mean for You

While the news on mortgage rates is overwhelmingly positive, it's important to remain grounded.

Winter Storms Dampen Recent Demand

It’s worth noting that despite the favorable rate environment, recent mortgage applications have seen a dip. The week ending January 30, for instance, saw a nearly 9% decrease in new mortgage applications. Freddie Mac attributes this largely to the winter storms that swept across the U.S., which likely hindered homebuying activities. This is a temporary setback. As the weather improves and the spring season picks up, we can expect to see renewed interest and activity in the housing market.

The Fed's Next Move: A Watchful Eye

While the Fed has paused rate cuts, the future trajectory of interest rates will depend on economic indicators like inflation and employment. If the economy continues to perform well and inflation remains under control, we might see rates stay at these favorable levels or even dip further. However, any unexpected economic shifts could lead to adjustments.

Key Takeaways from My Perspective

I view this sharp decline in 30-year fixed mortgage rates as a significant opportunity. For years, affordability has been the elephant in the room for many aspiring homeowners. This 78-basis-point drop is closing that gap considerably.

If you've been patiently waiting for the right moment to buy, or if you’ve been considering refinancing your existing mortgage to secure a lower rate, now is the time to seriously explore your options. Get pre-approved, talk to lenders, and understand exactly how much you can save. Don't let this moment pass you by. The housing market is dynamic, and conditions like these don't always last.

And

Alabama’s newer A- rental vs Tennessee’s larger property with higher NOI. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- What Leading Housing Experts Predict for Mortgage Rates in 2026

- Mortgage Rate Predictions for 2026: What Leading Forecasters Expect

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?