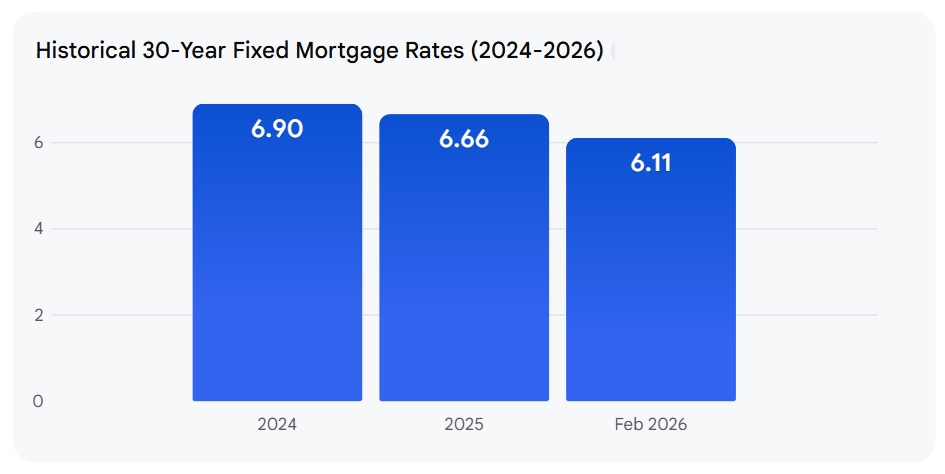

If you're thinking about buying a home or looking to lower your monthly payments on an existing mortgage, you're in luck. As of February 16, 2026, today’s mortgage rates are looking incredibly attractive, with the average 30-year fixed rate dipping to a compelling 5.85% and the 15-year fixed at 5.36%, according to data from Zillow. This marks a significant shift from the higher rates we experienced in previous years, offering a genuine opportunity to lock in some of the best borrowing costs we've seen in quite some time.

Today’s Mortgage Rates, Feb 16: Rates Drop to New Lows, Marking a Significant Shift

Understanding Today's Mortgage Rates: The Numbers

Let's break down exactly where things stand. Zillow Home Loans provides a clear snapshot of the current mortgage rate environment, and it’s quite encouraging for borrowers.

Here's a look at the average rates as of February 16, 2026:

| Loan Type | Average Rate |

|---|---|

| 30-year fixed | 5.85% |

| 20-year fixed | 5.64% |

| 15-year fixed | 5.36% |

| 5/1 ARM | 5.81% |

| 7/1 ARM | 5.71% |

| 30-year VA | 5.36% |

| 15-year VA | 5.15% |

| 5/1 VA | 4.99% |

What’s really striking here is how these rates are hovering near multi-year lows. You can see that both conventional loans and VA loans are offering competitive options. The VA loan products, especially, are incredibly attractive with the 5/1 VA ARM dipping below 5% at 4.99%. This is fantastic news for our veterans and service members.

What's Driving These Lower Rates? A Look Under the Hood

It’s easy to focus on the numbers, but understanding why they're falling is just as important. Several factors are working together to create this borrower-friendly environment:

- A Three-Year Trend Reversal: We’ve been seeing a steady decline in mortgage rates since the middle of 2025. This is a significant turnaround from the rising rates we experienced earlier this decade. It suggests a cooling of inflationary pressures and a shift in monetary policy.

- Economic Winds are Shifting: Softer inflation data and easing Treasury yields have played a major role. When inflation is under control and the government's borrowing costs (Treasury yields) go down, lenders have more room to offer lower interest rates on mortgages. It's a domino effect.

- The Federal Reserve's Influence: The Federal Reserve made three interest rate cuts in late 2025. While they held rates steady at their January 28, 2026 meeting, the market anticipates further cuts. The Fed’s decisions are heavily influenced by inflation and labor market data. Some experts are predicting they might hold off on additional cuts until at least March 2026, but the trend is leaning towards easing.

- Falling Treasury Yields: Specifically, the 10-year Treasury yield, which mortgage rates are often closely tied to, is currently hovering around 4.065%. This is a key indicator that points to lower mortgage rates being sustainable.

Expert Predictions: What’s Next?

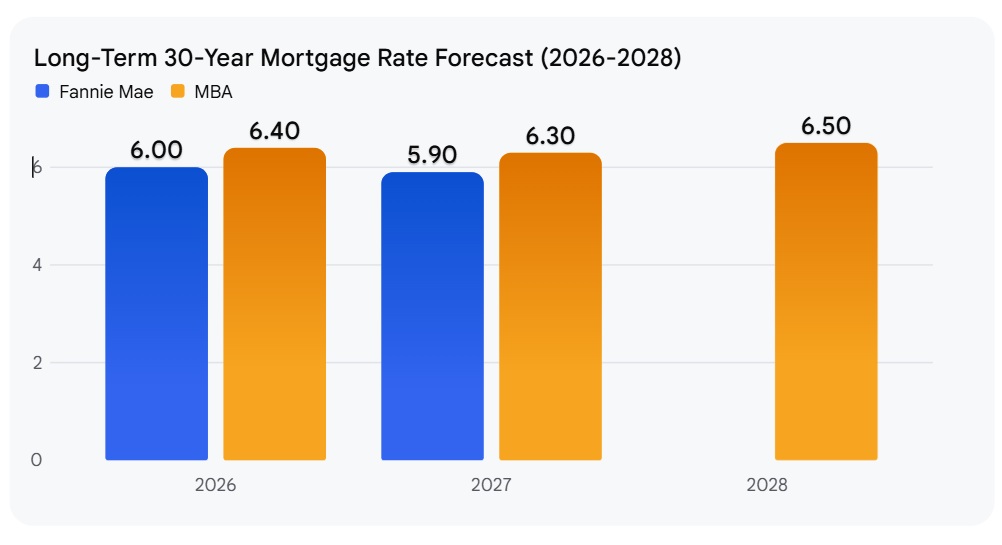

While today’s rates are a treat, it's natural to wonder about the future. Major industry organizations like the Mortgage Bankers Association (MBA) and Fannie Mae are forecasting that 30-year fixed rates will likely stay in a narrow range, around 6%, for the rest of 2026. This suggests that while we might not see rates plummet even further dramatically in the short term, they are expected to remain relatively stable and historically attractive. This forecast provides a degree of certainty for those planning their homeownership journey.

How These Rates Impact You: Homebuyers and Refinancers

The implications of these lower mortgage rates are significant and far-reaching for anyone involved in the housing market. From my perspective, this is a moment to really consider your options.

For Homebuyers:

- Improved Affordability: This is the biggest win. Lower rates mean either your monthly mortgage payment is less for the same loan amount, or you can afford to borrow more for the same monthly payment. This is especially critical in markets where home prices have been high, making affordability a major hurdle. You might find yourself qualifying for a bigger home than you initially thought possible, or simply enjoying a more comfortable monthly budget.

- Increased Purchasing Power: With lower interest costs, your housing budget stretches further. This could enable you to get into a more desirable neighborhood, a larger home, or simply have more wiggle room in your finances after moving in.

For Refinancers:

- Significant Savings: If you have a mortgage with an interest rate significantly higher than the current offerings, refinancing could save you thousands of dollars over the life of your loan. Even a half-percent or one-percent drop can add up substantially. I’ve seen clients save hundreds of dollars per month by refinancing when rates dropped, which is life-changing money.

- Accessing Equity: Refinancing can also be a way to tap into your home equity for things like renovations, consolidating debt, or funding education, often at a better rate than other loan types.

For Veterans and Service Members:

- Unbeatable Value: VA loans are already known for their fantastic benefits, like no down payment options and no private mortgage insurance. When coupled with the current low rates, such as the 5/1 VA ARM at 4.99% or the 15-year VA at 5.15%, they represent some of the most compelling and cost-effective financing options available today. It's a well-deserved perk for those who have served.

Key Takeaways: Seize the Opportunity

To sum it up, February 16, 2026, truly feels like a special day in the mortgage market. The 30-year fixed rate at 5.85% and the 15-year fixed at 5.36% aren't just numbers on a screen; they represent a tangible opportunity to improve your financial situation.

If you’ve been on the fence about buying or refinancing, now is the time to seriously explore your options. The market conditions are exceptionally favorable, but these low rates might not stick around forever. Acting strategically and understanding your personal financial goals will be key to making the most of this borrower-friendly environment. It’s a chance to secure a lower cost of borrowing that can benefit you for years to come.

VS

Texas’s A‑rated rental with stability vs Ohio’s affordable property with higher cap rate. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to Our Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?