It’s February 13th, and if you've been eyeing a refinance, I've got some news that might make you perk up: the 30-year fixed refinance rate has actually dropped by 9 basis points when you look at the bigger picture from last week, even though it nudged up a tiny bit today. That's a real signal that the market is still moving, and it’s worth paying attention to.

Mortgage Rates Today, February 13: 30-Year Fixed Refinance Drops by 9 Basis Points

Let's dive into what this means for your wallet and your homeownership dreams this Valentine's Day week.

A Quick Look at Today’s Refinance Rates

The mortgage market is a bit like a moody teenager right now – things are shifting, and not always in a straight line. According to Zillow's data for February 13th, 2026, here's where we stand:

| Loan Type | Today's Rate | Change from Friday | Change from Last Week |

|---|---|---|---|

| 30-Year Fixed | 6.46% | Up 5 basis points | Down 9 basis points |

| 15-Year Fixed | 5.59% | Up 6 basis points | Up 6 basis points |

| 5-Year ARM | 7.03% | Up 3 basis points | Up 3 basis points |

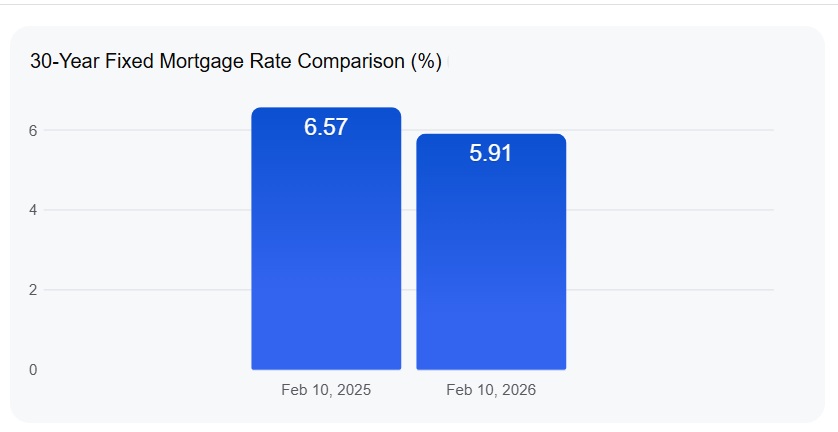

As you can see, it's a bit of a mixed bag. The 30-year fixed refinance rate is up a smidge from Friday, sitting at 6.46%. But here's the good news: compared to where we were at the beginning of last week, it's actually down by 9 basis points from 6.55%. This is the one that matters most for a lot of homeowners looking to lower their monthly payments over the long haul.

For those looking to pay off their home faster, the 15-year fixed refinance rate has edged up a bit, now at 5.59%. While this might seem a little higher, it’s still a strong option if you can handle a larger monthly payment, as you’ll save a ton on interest over the life of the loan.

And then there are Adjustable-Rate Mortgages (ARMs). The 5-year ARM refinance rate is currently at 7.03%, up a few basis points. These can be tempting with their lower initial rates, but the jump here reminds us that they come with the risk of future rate hikes.

Why the Ups and Downs? Let's Break It Down.

As someone who’s been watching the mortgage market for a while, I can tell you it's never just one thing causing rates to move. It’s a complex dance between economic news, government actions, and what people are actually doing.

- Economic Whispers (and Shouts): The latest inflation reports and job numbers are like the weather forecast for mortgage rates. When the economy looks strong, like with the recent news of 130,000 jobs added in January, it can make lenders a bit nervous about inflation sticking around. This, in turn, can put a little upward pressure on rates because investors demand higher returns for their money in a growing economy.

- The Fed's Stance: The Federal Reserve has been playing a strategic game. After cutting rates a few times back in late 2025, they’ve hit the pause button for now. This is to see how the economy is reacting. While everyone’s hoping for more cuts, any hint of a change in their plan makes the market jump.

- A Helping Hand for Mortgages: Interestingly, there's a new government directive that's directly trying to lower borrowing costs. Fannie Mae and Freddie Mac have been tasked with buying a significant amount of mortgage-backed securities. This is essentially injecting money into the market and is designed to push mortgage rates down, independent of what the Federal Reserve is doing with its main interest rate. It's a pretty big deal and is likely a major reason why we're seeing rates drop from last week's levels.

- Your Neighbors are Refinancing: Remember the huge refinancing boom during the pandemic? Well, it's picking up steam again, but for different reasons. Almost 5 million homeowners are now in a position where they can actually save money by refinancing. This is especially true for those who took out loans at higher rates (think 7% or more) in 2023 and 2024. We saw a big jump in refinance applications last month, proving that people are ready to act when the numbers make sense.

What This Really Means for YOU, the Homeowner

So, what’s the takeaway from all this?

- Your Refinance Window: That 9-basis point drop in the 30-year fixed refinance rate from last week is your cue. It’s a solid opportunity to potentially lock in a lower monthly payment if you’ve been on the fence. Even a small drop can save you thousands over the years.

- The Great Rate Debate: Short vs. Long: It always comes down to your personal situation. Do you want the lowest possible monthly payment and plan to stay in your home for a long time? The 30-year fixed is your friend. Or can you handle a higher monthly payment to slash years off your loan and save a boatload on interest? Then the 15-year fixed is worth serious consideration. It’s a trade-off between today’s cash flow and long-term wealth building.

- ARMs: Proceed with Caution: With 5-year ARMs now averaging over 7%, they’re looking less like a bargain and more like a gamble for most people, especially if interest rates keep going up. Unless you’re absolutely sure you’ll sell or refinance again before those variable rates kick in, it might be wiser to stick with a fixed rate.

My Two Cents: Strategic Moves in Today's Market

Having weathered many mortgage market cycles, I’ve learned that timing and strategy are everything.

- Don't Ignore the Small Stuff: Those basis points might sound tiny, but trust me, they add up. I’ve seen clients save tens of thousands of dollars over a 30-year mortgage just by locking in a rate that was a quarter-point lower. Keep an eye on those weekly trends.

- Think Local: While these are national averages, your specific area might have slightly different rates. If you're in a hot market like Texas, California, or Florida, you might see some variations due to how many lenders are competing and how much demand there is for homes.

- The Crystal Ball (Kind Of): If inflation continues to cool down, which is the hope, we could see refinance rates continue to creep downwards in the coming months. However, as we've seen, the market can be unpredictable, so getting locked into a good rate now is often better than waiting for a potential future drop that may or may not happen.

The “Great Housing Reset” and Digital Dreams

You can't scroll through real estate forums or social media these days without hearing about the “Great Housing Reset of 2026.” People are actively discussing when the “lock-in effect” – where homeowners are stuck with their current low rates – will finally break.

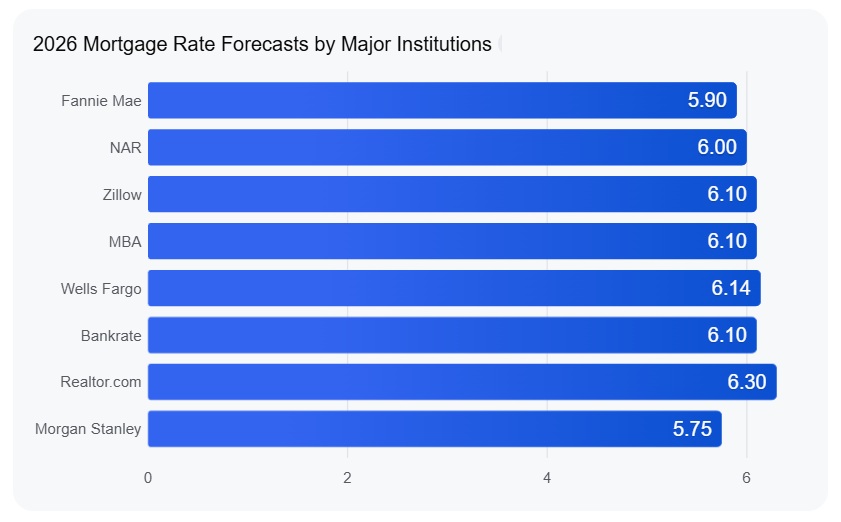

Many are debating whether to “buy now” or wait. Some analysts are predicting rates could hit 5.75% by mid-year, which is a tempting thought. But with home equity at record highs (we're talking an average of $181,000 per homeowner with a mortgage!), a lot of people are leaning towards using that equity for renovations through cash-out refinances or Home Equity Lines of Credit (HELOCs) instead of battling it out in the still-tight purchase market.

And my personal observation? The shift to online mortgage services is undeniable. About 86% of folks now prefer digital platforms, and frankly, it makes sense. Faster processing, less paperwork – it streamlines the whole confusing process.

The Bottom Line: What to Do Today

So, to wrap things up, that 9-basis point drop in the 30-year fixed refinance rate from last week isn't just a number; it's a tangible opportunity for homeowners. Even though rates saw a slight uptick today, the recent downward trend is encouraging.

My advice? Take a good, hard look at your financial goals. Do you want to cut your monthly bills? Pay off your home faster? Are you comfortable with the idea of an ARM for a while? Evaluate what makes the most sense for your personal situation.

Refinancing now, especially with rates hovering near these multi-month lows, could help you secure significant savings. But as always, do your homework, compare offers, and make sure you’re making a decision that’s right for you and your family's future.

and

Florida’s modern build with strong cash flow vs Missouri’s affordable rental with higher cap rate. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to Our Investment Counselor (No Obligation):

(800) 611-3060

Market forecasts suggest steady demand, making turnkey real estate one of the most reliable paths to passive income and wealth creation.

Norada Real Estate helps investors capitalize on these trends with turnkey rental properties designed for appreciation and consistent cash flow—so you can grow wealth securely while others wait for clarity in the market.

Recommended Read:

- 30-Year Fixed Refinance Rate Trends – February 12, 2026

- Best Time to Refinance Your Mortgage: Expert Insights

- Should You Refinance Your Mortgage Now or Wait Until 2026?

- When You Refinance a Mortgage Do the 30 Years Start Over?

- Should You Refinance as Mortgage Rates Reach Lowest Level in Over a Year?

- Half of Recent Home Buyers Got Mortgage Rates Below 5%

- Mortgage Rates Need to Drop by 2% Before Buying Spree Begins

- Will Mortgage Rates Ever Be 3% Again: Future Outlook

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years