Here's the big news for homeowners and aspiring buyers: mortgage rates have seen a significant drop, dipping by nearly 100 basis points since 2024, and this is creating a fantastic opportunity for those looking to refinance their homes. As of March 5, 2026, the average 30-year fixed-rate mortgage stands at a very attractive 6.00%, a steep decline from where we were just a couple of years ago, and this has certainly gotten people talking – and acting – on their home financing.

When rates take a tumble like this, it's not just a minor blip; it can translate into real savings for people. Freddie Mac, a key player in the housing finance market, has reported this sharp decline and, as I suspected, it's already leading to a noticeable uptick in homeowners looking to refinance their existing mortgages. It's also giving a boost to those wanting to buy a new home.

30-Year Fixed Mortgage Rate Falls Nearly 100 Basis Points Since 2024

What's Behind the Big Drop? A Look at the Numbers

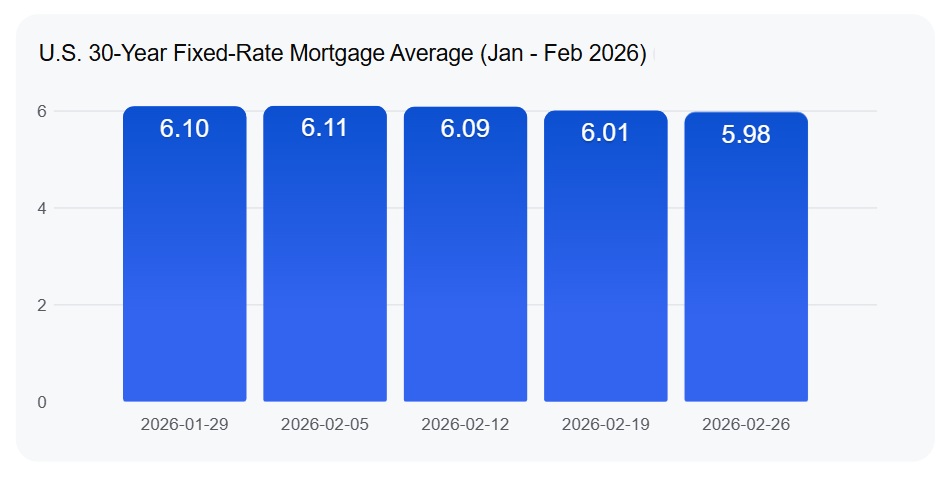

Let's dive a bit deeper into what Freddie Mac's Primary Mortgage Market Survey is telling us. For the week ending March 5, 2026, that average 30-year fixed mortgage rate hit 6.00%. To put that into perspective, if you cast your mind back to around the same time in 2024, that rate was considerably higher. In fact, by March 2025, it was sitting at 6.63%. That's a difference of nearly 0.7 percentage points right there, and if we compare it to earlier in 2024, the drop is even more pronounced, approaching that 100-basis-point mark.

Here's a quick snapshot from Freddie Mac's data for the week ending March 5, 2026:

- 30-Year Fixed-Rate Mortgage: Averaged 6.00%. This is up ever so slightly from 5.98% the week before, showing a little bit of fluctuation, but still comfortably in a lower range.

- 15-Year Fixed-Rate Mortgage: Averaged 5.43%. This shorter-term loan also saw a slight dip, down from 5.44% in the prior week.

It’s important to remember that these are averages. Your specific rate will depend on your credit score, loan-to-value ratio, and the lender you choose. But the overall trend is undeniable: borrowing money for a home is cheaper now than it has been in quite some time.

The Ripple Effect: Why Refinancing is Booming

So, why should this matter to you? Well, when mortgage rates decrease significantly, it opens up a golden opportunity for homeowners who originally took out their loans when rates were higher. This is where the surge in refinance activity comes into play.

I've spoken with many people who are now looking at refinancing. They might have locked in a 30-year mortgage at 7% or even 8% a couple of years ago. Now, with rates dipping into the 5% range, they can potentially lower their monthly payments significantly, or perhaps shorten the loan term, saving them tens of thousands of dollars in interest over the life of the loan.

Weekly refinance applications jumped by a considerable 14.3% as rates fell into that 5% territory in late February. And when you compare that to the previous year, this represents a massive 109% increase year-over-year (Mortgage Bankers Association). That tells me people are not just noticing the lower rates, they are actively taking advantage of them.

This recent trend sees mortgage rates hovering near their lowest levels since late 2022. For many homeowners, this is a chance to reset their finances and achieve greater stability or affordability.

What's Driving These Rate Movements?

As with most things in economics, there isn't one single factor at play, but rather a combination of forces. Freddie Mac points to lower U.S. Treasury yields as a primary driver for the decline in mortgage rates. Generally, when Treasury yields go down, mortgage rates tend to follow suit because they are closely correlated.

However, it's not always a smooth ride. We’ve also seen some volatility. Recent geopolitical tensions and ongoing concerns about inflation have caused day-to-day fluctuations. These larger global and economic events can introduce some uncertainty, leading lenders to adjust their rates in response. It’s a delicate balance.

Looking Ahead: The Spring Buying Season and Beyond

With these lower rates, economists at Freddie Mac are optimistic about the upcoming spring homebuying season. This is traditionally a busy time for real estate, and the more favorable borrowing conditions are expected to draw more potential buyers into the market.

Here are a few forecasts from some major housing authorities:

- Fannie Mae: Predicts average rates around 6.0% for much of 2026, possibly touching 5.9% by the year's end.

- Mortgage Bankers Association (MBA): Expects rates to stay in a tight band of 6.0% to 6.5%, averaging about 6.1%.

- National Association of Realtors (NAR): Believes rates could fall to 6.0%, which they think will unlock more market activity.

- Morgan Stanley: Offers a more optimistic view, suggesting rates could hit 5.50%–5.75% by mid-2026 if Treasury yields continue to drop.

Refinance activity is also predicted to stay strong throughout 2026. Redfin, a real estate brokerage, even projects a 30% increase in total refinance volume for the year. Analysts are seeing that rates dropping below the 6.0% mark act as a significant psychological trigger, encouraging many homeowners who may have been waiting on the sidelines to finally take action on refinancing. For those who secured a mortgage at rates between 6.5% and 8% in 2023 and 2024, the current environment presents a genuinely attractive window to improve their financial situation.

Is Refinancing Right for You? Expert Thoughts

From my perspective, this is a prime time for homeowners to at least explore their refinancing options. It's not just about snagging a lower monthly payment, though that's a huge benefit. It could also be about:

- Cashing out equity: If you've built up significant equity in your home, a cash-out refinance can provide funds for renovations, debt consolidation, or other major expenses.

- Switching loan types: Perhaps you have an adjustable-rate mortgage and want to lock in a fixed rate for stability.

- Shortening your loan term: If you're in a strong financial position, you might refinance into a shorter term (like a 15-year mortgage) to pay off your home much faster and save on interest.

However, it's crucial to remember that refinancing involves costs, such as appraisal fees, title insurance, and lender fees. You need to calculate if the savings from the lower interest rate will outweigh these expenses over the time you plan to stay in your home. This is where a good financial advisor or mortgage broker can be invaluable. They can run the numbers for your specific situation and help you determine if refinancing makes financial sense.

Key Considerations When Refinancing:

- Your Current Loan Terms: What's your existing interest rate and remaining loan term?

- Closing Costs: How much will it cost to refinance?

- Break-Even Point: How long will it take for your monthly savings to cover the closing costs?

- Your Financial Goals: Are you looking for lower monthly payments, faster payoff, or to access equity?

- Your Credit Score: A higher credit score will generally secure you the best rates.

The current market conditions are undeniably favorable for homeowners looking to improve their mortgage situation. The nearly 100-basis-point drop in mortgage rates since 2024, as reported by Freddie Mac, has created a significant opportunity. Whether you're looking to lower your monthly payments or gain more financial flexibility, now is the time to seriously consider exploring your refinancing options.

VS

Nashville’s A‑rated rental with stability vs Birmingham’s affordable property with higher cap rate. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain near 6%, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Will Mortgage Rates Drop to 5% in 2026: Expert Forecast

- How to Get a 3% Mortgage Rate in 2026 With Assumable Mortgages?

- How to Get a 4% Interest Rate on a Mortgage in 2026?

- What Leading Housing Experts Predict for Mortgage Rates in 2026

- Mortgage Rate Predictions for 2026: What Leading Forecasters Expect

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?