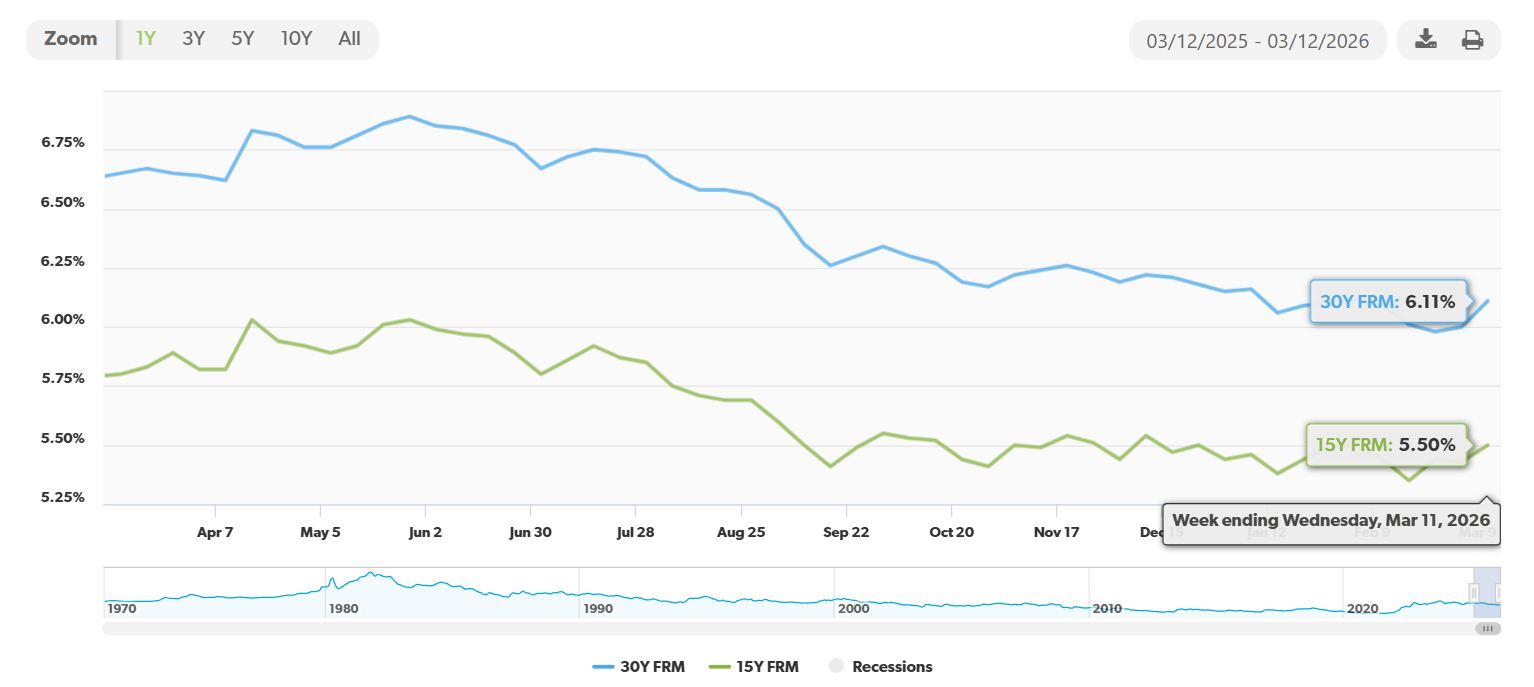

If you're thinking about buying a home or refinancing an existing mortgage, you've probably been keeping a close eye on interest rates. As of Sunday, March 22, 2026, today's mortgage rates have reached their highest point since September of last year, a trend that’s making waves in the housing market. The 30-year fixed mortgage rate is now averaging a solid 6.31%, and the 15-year fixed rate has ticked up to 5.77%. This isn't just a small blip; it reflects a broader economic story that's worth understanding if you're navigating the current real estate environment.

It feels like just yesterday we were seeing rates dip below the 6% mark, and honestly, it’s a bit of a jolt to see them climb again. This shift is a stark reminder of how sensitive the housing market is to larger economic forces. From my perspective, when rates move like this, it signals that several factors are at play, and it’s not just a random fluctuation.

Today's Mortgage Rates, March 22: 30-Year Fixed Rises to 6.31%, a Six-Month High

Let’s break down the numbers you need to know, directly from Zillow, which is a go-to source for this kind of data. As of March 22, 2026, these are the rates we're seeing:

| Mortgage Type | Interest Rate |

|---|---|

| 30-Year Fixed | 6.31% |

| 20-Year Fixed | 6.29% |

| 15-Year Fixed | 5.77% |

| 5/1 ARM | 6.36% |

| 7/1 ARM | 6.34% |

| 30-Year VA | 5.85% |

| 15-Year VA | 5.47% |

| 5/1 VA | 5.39% |

These figures are significant because they represent the highest we’ve seen in about six months. This means that for anyone taking out a new mortgage or considering refinancing an older, higher-rate loan, the costs involved have just gone up. It puts a bit more pressure on wallets, plain and simple.

Why Are Rates Going Up? It's Not Just One Thing.

There are a few big reasons why we're seeing this upward trend in mortgage rates. It’s a confluence of global events and domestic economic policy that's pushing borrowing costs higher.

- Inflation Woes: The biggest story continues to be inflation. Even though the Federal Reserve has been working to keep it in check, stubborn inflation concerns are making lenders nervous. When inflation is high, the money you borrow today is worth less in the future, so lenders need to charge more interest to compensate.

- Global Economic Jitters: The world feels a little uncertain right now. The ongoing conflict with Iran, for instance, has really shaken global markets. When oil prices jump above $100 a barrel, as they have recently, it directly contributes to inflation. This kind of global instability always makes investors a bit more cautious, and that caution gets passed on to borrowing costs.

- The Fed's Tightrope Walk: The Federal Reserve held its benchmark interest rate steady at 3.5%–3.75% during its March 18 meeting. While this might seem like good news, keeping the federal funds rate high signals the Fed's continued focus on fighting inflation. It also means the cost of borrowing money for banks remains elevated, which in turn influences the rates they offer to consumers. They’ve only projected one rate cut for late 2026, which doesn't offer much immediate relief.

- Bond Market Signals: Longer-term government bonds are a key indicator for mortgage rates. The 10-year Treasury yield recently shot up to 4.303%. When Treasury yields rise, it generally means investors are demanding more return for lending their money, and this directly correlates with higher mortgage rates.

How This is Affecting Homeowners and Buyers

When mortgage rates rise, it doesn’t just affect the numbers on a spreadsheet; it has real-world consequences for real people.

- The Affordability Squeeze: For those looking to buy, especially for the first time, this jump is noticeable. Moving from rates below 6% just a month ago to over 6.3% can mean an extra few hundred dollars on your monthly mortgage payment. That can make a significant difference in what kind of home people can afford or even if they can enter the market at all. I’ve seen firsthand how quickly affordability can change when rates shift even a quarter of a percent.

- Refinancing Gets Less Appealing: Homeowners who locked in rates below 6% are likely feeling pretty good about that decision right now. With rates climbing, the incentive to refinance has dwindled significantly. Why would you trade a 5.5% rate for a 6.31% rate? This is why we're seeing a shift in how people access home equity.

- Turning to HELOCs and Home Equity Loans: Instead of refinancing their primary mortgage, many homeowners are tapping into their home equity through Home Equity Lines of Credit (HELOCs) or home equity loans. The average rates for these are currently around 7.20% for HELOCs and 7.47% for home equity loans. While these rates are higher than primary mortgages, they allow homeowners to keep their existing low mortgage rate and still access cash for renovations, debt consolidation, or other needs. It’s a smart move for many to preserve their prime mortgage terms.

- Demand Takes a Hit: Unsurprisingly, this rate environment has cooled down buyer demand. Mortgage applications fell by 10.9% last week, and the drop in refinance activity was particularly sharp. When rates move further away from the magic 6% mark, people tend to put their buying or refinancing plans on hold.

What Does the Future Hold? Expert Predictions

Looking ahead, there’s a lot of discussion about where rates might go. While nobody has a crystal ball, some of the smartest minds in the industry have offered their insights.

- Fannie Mae's View: Fannie Mae is predicting that by the end of 2026, rates could potentially settle back down to the 5.7%–5.9% range. This optimistic outlook assumes that economic growth will slow down from its current pace, which would typically lead to lower interest rates.

- The Mortgage Bankers Association (MBA) Perspective: The MBA, on the other hand, is a bit more cautious. They forecast that rates will likely remain in the 6% to 6.5% range for the rest of 2026. Their view suggests that persistent inflation will keep borrowing costs elevated, even if they don't climb much higher from here.

From my experience, these predictions often come with a caveat: the economic situation is fluid. If there are unexpected developments, these forecasts could change.

Key Takeaways for Today's Market

If you're trying to make sense of all this, here are the most important things to remember as of March 22, 2026:

- Rates are High (for now): We've hit a six-month high for mortgage rates, with the benchmark 30-year fixed at 6.31%.

- Inflation and Global Issues Drive This: Persistent inflation, geopolitical conflicts, and rising bond yields are the main reasons for these higher costs.

- Homeowners are Being Creative: To avoid higher primary mortgage rates, people are increasingly using HELOCs and home equity loans.

- Buyers are Pulling Back: Demand has softened, although there's more inventory available, which can create opportunities for determined buyers.

- Expect More of the Same (for a while): Analysts anticipate rates will stay elevated, with only modest potential for relief towards the end of the year.

The Bottom Line: Today's mortgage rates, March 22, have climbed to their highest levels since last fall, impacting both those looking to buy and those considering refinancing. The current economic climate, fueled by inflation and global uncertainty, is keeping borrowing costs high. While there's hope for stabilization later in 2026, the near future suggests continued challenges for affordability in the housing market. It’s a time for careful consideration and strategic planning for anyone involved in real estate.

VS

Two Pleasant Grove rentals—one affordable with higher cap rate vs one larger with stronger NOI. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?