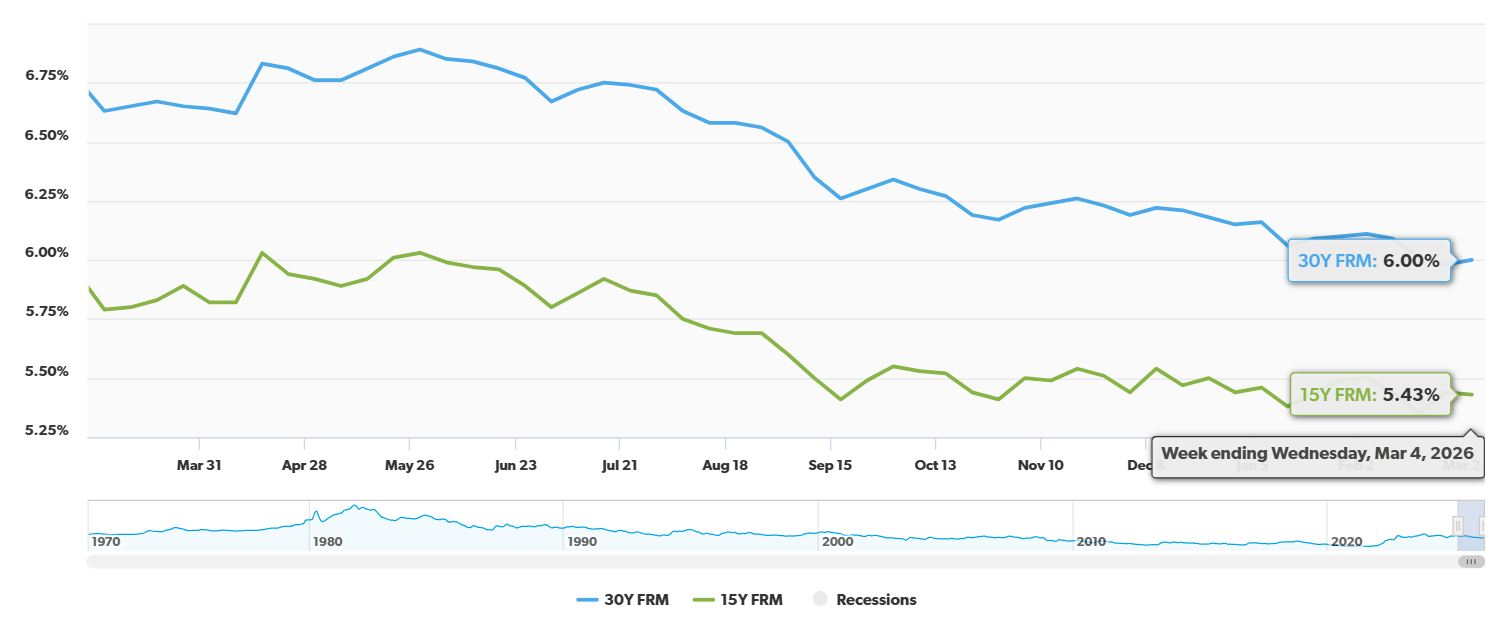

Well, it’s March 15th, 2026, and if you’ve been keeping an eye on mortgage rates, you’ll notice they’ve nudged back up, crossing that 6% mark again. This isn’t a shocker, given the choppy global waters we're navigating. For many of us thinking about buying a home or refinancing, this is the critical question: how do today's mortgage rates affect our plans? As of Sunday, March 15, 2026, the average rate for a 30-year fixed mortgage has settled at 6.08%, according to Zillow.

This is a bit of a climb back from dipping below 6% just a few weeks ago, and it’s a clear signal that the market is still a bit on edge. While we're not seeing the sky-high rates of 2023, this recent upward tick is something worth paying attention to.

Today's Mortgage Rates, March 15: What You Need to Know Right Now

Why the Jump? A Look Under the Hood

It’s easy to just see the numbers, but understanding why rates move is key to making smart decisions. Right now, a couple of big factors are at play.

First, we’re seeing some serious ripples from geopolitical instability. Reports of military actions involving the U.S., Israel, and Iran have sent oil prices spiking to around $89 a barrel. When energy costs go up, it doesn’t just affect your gas tank; it tends to fan the flames of inflation. Higher inflation usually means that the yields on bonds go up, and guess what heavily influences mortgage rates? You got it – those bond yields. It's a domino effect from global events straight to your potential monthly payment.

Second, there's the ever-present Federal Reserve. The Fed is expected to keep its finger on the pause button, holding interest rates steady when they meet on March 17th and 18th. Now, the Fed doesn't directly set mortgage rates, but their signals about inflation and their economic outlook are a big deal. Their cautious approach, especially concerning inflation, is putting a cap on how low mortgage rates can really go.

The Spring Market is Stirring

Even with these rate ups and downs, it's interesting to see that buyer activity hasn't completely stalled. In fact, Zillow data shows that purchase applications actually rose by 7.8% in early March. This tells me that people are still eager to get into the housing market, especially as we head into the more traditional spring buying season. And it makes sense; compared to the 8% plus rates we saw in late 2023, where we are now still feels like a relative bargain for many.

It’s a bit of a balancing act. On one hand, rates have moved up. On the other, they’re still a far cry from the punishing highs of not too long ago. This can create a sense of urgency for some buyers who want to lock in a rate before they potentially climb further.

What the Experts See for the Rest of 2026

So, what’s the crystal ball telling us about the rest of the year? I’ve been following the forecasts from big names in the housing world like Fannie Mae and the Mortgage Bankers Association (MBA), and they seem to be pointing towards a period of relative calm. Their projections suggest that mortgage rates will likely hover in the 6.0% to 6.1% range for the remainder of 2026. This is good news for anyone hoping for some predictability.

However, and this is where my experience kicks in, it’s crucial to remember that forecasts are just that – forecasts. The economic world is full of “wildcards.” We’re talking about potential new trade tariffs, unexpected shifts in the job market, or even further international flare-ups. These could cause rates to dance around a bit more, possibly swinging anywhere from 5.7% to 6.5% throughout the year. So, while stability is the general expectation, don't be surprised by some bumps along the way.

Your Mortgage Rate Game Plan: What It Means for You

If you're in the market for a home or considering refinancing, here’s how I see today's numbers and trends impacting your decision-making:

- The Opportunity Window is Still Open: While rates are above 6%, they’re still significantly better than the rates of last year. This presents a real chance to secure a more favorable interest rate on a home or a refinance compared to what many experienced in 2023. It's about seizing the moment.

- Consider Locking It In: Given the current global uncertainties and the ongoing inflation concerns, many financial advisors (and frankly, my own gut feeling) would suggest that locking in your rate sooner rather than later is a smart move. Waiting for that absolute “perfect” bottom might mean missing out on a good rate altogether if the market takes an unexpected turn.

- The Spring Market is Heating Up: The rise in purchase applications is a clear indicator. We're likely to see increased competition among buyers in the coming months. This means being prepared, pre-approved, and ready to act quickly when you find the right home.

The Bottom Line from My Perspective

As of March 15, 2026, we're seeing mortgage rates climb back above the 6% mark, largely due to global instability and concerns about inflation. This is a point where it's really important to stay informed and make a plan. Zillow's data shows the current averages, and while forecasts suggest general stability around 6% for the rest of the year, remember that unforeseen events can always shake things up.

For anyone looking to buy or refinance, there’s a delicate balance between acting decisively to secure a good rate and being aware of potential market fluctuations. My advice? Get your ducks in a row, understand your options, and make the move that feels right for your financial future. Don’t let the noise distract you from what’s important: securing a home at a manageable cost.

VS

Two Texas rentals in A‑rated neighborhoods—Cibolo’s larger home vs San Antonio’s newer build with stronger cap rate. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?