The mortgage market on March 2, 2026, is offering some of the most attractive borrowing costs we've seen in years. If you're thinking about buying a home or refinancing, the numbers are definitely worth paying attention to. To put it simply, today's 30-year fixed mortgage rate is averaging 5.81%, and the 15-year fixed mortgage rate has dipped to a remarkable 5.32%. This is significant news, especially as we head into the busy spring homebuying season.

Today's Mortgage Rates, March 2: Rates at Multi‑Year Lows Spark Buyer Optimism

Let's break down what these numbers look like across different loan types. Zillow's data for March 2, 2026, paints a clear picture:

| Loan Type | Current Interest Rate |

|---|---|

| 30-Year Fixed | 5.81% |

| 20-Year Fixed | 5.76% |

| 15-Year Fixed | 5.32% |

| 5/1 ARM | 5.82% |

| 7/1 ARM | 5.88% |

| 30-Year VA | 5.41% |

| 15-Year VA | 5.04% |

| 5/1 VA | 5.01% |

As you can see, the 30-year fixed, the most popular choice for many Americans, is comfortably below 6%. The 15-year fixed is even lower, offering a fantastic opportunity to pay off your home faster. Even the VA loans, which are designed to help our nation's veterans, are showing incredibly competitive rates.

What's Driving This Drop in Mortgage Rates?

It's not just a random fluke that rates have fallen so dramatically. Several key factors are working together to push borrowing costs down:

- Strategic Moves in the Bond Market: In early 2026, the Trump administration made a significant move by directing Fannie Mae and Freddie Mac to actively purchase mortgage-backed securities (MBS). We're talking about a $200 billion injection into this market. Think of it this way: when more people (or in this case, government-backed entities) are buying up mortgages, the demand for them goes up. This demand narrows the gap between what mortgage lenders can get for your loan and what they have to pay to borrow money themselves (often tied to Treasury yields). This allowed lenders to lower their rates even without a direct boost from the Federal Reserve in February.

- Inflation is Cooling Off: The good news on the inflation front continues. Recent data suggests that inflation is steadily moving closer to the Federal Reserve's target of 2%. At the same time, the labor market, while still strong, is showing signs of moderating. When inflation is under control and the job market isn't overheating, it signals to the economy that borrowing money might be a bit less risky. This, in turn, pushes down the yields on longer-term investments like bonds, which directly impacts mortgage rates.

- Looking Ahead to Future Fed Actions: The Federal Reserve is playing a strategic role. After making three interest rate cuts in 2025, they held steady at their first meeting of 2026. However, the financial markets are already anticipating that more cuts are on the horizon later this year. This expectation of future lower interest rates has a ripple effect, putting downward pressure on long-term rates, including the 10-year Treasury yield, which is a key benchmark for mortgage rates.

- A Global Search for Safety: In times of global uncertainty, investors often flock to what they consider safe havens. U.S. Treasury bonds are widely viewed this way. Increased demand for these safe assets drives their prices up and, consequently, their yields down. This global trend of seeking stability in U.S. debt contributes to those lower mortgage rates we're seeing.

A Look at the Weekly Trends

The downward movement isn't just a one-off event; it's been a consistent trend.

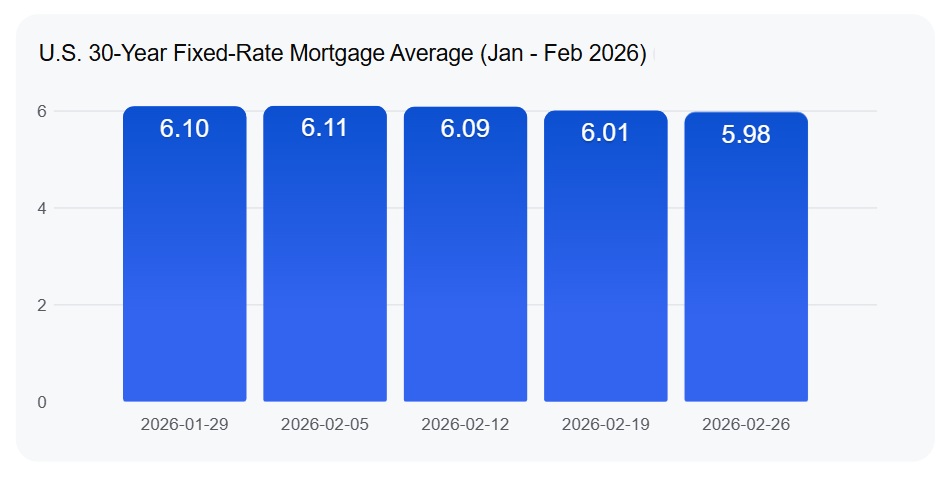

- The 30-Year Fixed Mortgage: At 5.81%, this rate is down over 11 basis points from the previous week. This is the lowest we've seen in more than three years, making it a very attractive option for many.

- The 15-Year Fixed Mortgage: Hitting 5.32% is a big deal. This is the lowest point for this loan type since 2022. It means borrowers can build equity much faster while paying less in interest over the life of the loan.

- Adjustable-Rate Mortgages (ARMs): While ARMs like the 5/1 ARM at 5.82% and the 7/1 ARM at 5.88% are still competitive, the current stability and attractiveness of fixed-rate options are making them the go-to for many buyers. When fixed rates are this low, the predictability of them is a huge advantage.

What This Means for You: Borrowers and Homeowners

These lower mortgage rates have significant implications depending on your current situation:

- For Homeowners Looking to Refinance: If you took out a mortgage in 2024 or 2025 when rates were higher (think 7% or more), now is an absolutely prime time to consider refinancing. Even a drop of 1% on a $340,000 loan can save you well over $2,000 annually in interest payments. That's money that can go back into your pocket or be used for other financial goals. I've seen many homeowners put off refinancing, thinking it's too much hassle, but the savings now are substantial enough to make it very much worth exploring.

- For Prospective Homebuyers: The improved affordability is a game-changer. Not only are the monthly payments lower, but this could also mean more competition in the housing market. Builders are still actively offering incentives like rate buydowns, which can further sweeten the deal and make homeownership even more accessible. If you've been waiting on the sidelines, now might be the time to jump in.

- Thinking About the Market's Future: The general consensus from major forecasters, including Fannie Mae and the National Association of Realtors (NAR), is that we'll likely see rates hovering around or even below 6% for the rest of 2026. This “sub-6%” environment is expected to act like a gentle nudge, encouraging those “locked-in” homeowners who might be hesitant to sell because of their current low rates to finally list their homes. It also provides a much-needed boost for first-time buyers who are looking for that entry point into the market. My sense is that this could lead to a more balanced and active spring season than we've seen in a few years.

Key Takeaways from Today's Mortgage Rates

- We are currently experiencing multi-year lows in mortgage rates, with the benchmark 30-year fixed rate at 5.81% and the 15-year fixed at 5.32%.

- Several factors are contributing to this positive trend, including Federal intervention in the bond market, cooling inflation, and global geopolitical stability driving safe-haven demand for U.S. bonds.

- Homeowners with existing higher-rate mortgages have a strong refinancing opportunity.

- Buyers should be prepared for potentially increased activity and competition as affordability improves, especially with the spring homebuying season approaching.

VS

Two Texas rentals in A‑rated neighborhoods—Cibolo’s larger home vs San Antonio’s newer build with stronger cap rate. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?