Securing the lowest 30-year fixed mortgage rate in 2026 isn’t about luck — it’s about preparation. While most borrowers will see rates hover near 6%, highly qualified buyers may be able to lock in something closer to the mid-5% range. The ultra-low rates of past years aren’t coming back anytime soon. But that doesn’t mean meaningful savings are out of reach. Even a small difference in your rate can translate into tens of thousands of dollars over the life of a loan.

The key is understanding what lenders are really looking for. Getting the lowest available rate goes beyond having a strong credit score — it requires presenting a complete financial profile that signals stability, low risk, and long-term reliability. Here’s what you need to know to position yourself for the most competitive 30-year fixed mortgage rates in 2026.

How to Get the Lowest 30-Year Fixed Mortgage Rate in 2026?

Factors That Will Help You Nail the Lowest Rate

Getting a mortgage rate below 6% in 2026 is definitely achievable if you tick all the right boxes. It goes beyond just having a decent credit score, although that's a huge part of it. Lenders assess several things to figure out how much of a risk you are, and the lower that risk, the better the rate they'll offer.

- Your Credit Score is King: If you're aiming for the absolute lowest advertised rates, you'll likely need a credit score of 780 or higher. Think of it like climbing a ladder; each rung you move up can make a difference. Moving up just one credit band, say from a 620 to a 640, could potentially drop your rate by roughly 0.18% to 0.25%. That might not sound like much, but over 30 years, it adds up significantly.

- The Power of Your Down Payment: Putting down a larger amount than the standard 20% (which helps you avoid private mortgage insurance, or PMI) can also signal to your lender that you're less of a risk. A down payment substantially larger than 20% can sometimes lead to additional rate discounts. It shows you're financially invested and have skin in the game.

- Loan Term: Shorter Can Mean Cheaper: This is a big one, and it often surprises people. If you can swing it, switching from a 30-year fixed mortgage to a 15-year fixed mortgage can typically lower your interest rate by a good chunk, usually around 0.50% to 0.75%. Yes, your monthly payments will be higher because you're paying it off faster, but you'll save a ton on interest over the life of the loan.

- “Buying Down” Your Rate with Discount Points: This is a strategy where you pay an upfront fee to lower your interest rate for the life of the loan. Typically, paying one discount point, which is 1% of the loan amount, can reduce your interest rate by about 0.25%. You'll need to do the math to see if the upfront cost is worth the long-term savings for your specific situation.

- Your Debt-to-Income (DTI) Ratio Matters: Lenders like to see that you're not carrying too much debt relative to your income. While a DTI of 35% or less is generally preferred, the most competitive rates often go to borrowers with a DTI below 25%. This shows you have plenty of room in your budget for a mortgage payment.

The “Baseline Floor”: Why Rates Won't Plummet to 2.5%

Now, let's talk about the reality check. It's going to be incredibly difficult to see new 30-year fixed mortgage rates drop below 5.0% in 2026. There are fundamental economic reasons for this, often referred to as the “baseline floor.”

- Economic “Stickiness”: Things like persistent inflation (even if it's around 2.7%), and the government needing to borrow money, tend to keep long-term bond yields higher than we've seen in the past. These yields are a major factor in mortgage rates.

- The Fed's Cautious Stance: The Federal Reserve, which controls short-term interest rates, has been signaling a careful approach. They aren't planning on slashing rates drastically through 2026. This means we're not likely to return to the super-low, pandemic-era rates anytime soon.

- Lender Risk and Profit: Lenders need to make a profit, and they do this by adding a “spread” to the yield on 10-year Treasury bonds. If those Treasury yields are expected to stay around 3.75%, lenders physically can't offer mortgages much lower than about 5.5% without actually losing money.

The “Holy Grail”: Assumable Mortgages in 2026

So, if getting below that 5.5% to 5.75% range for a new mortgage is tough, how can someone potentially get an even lower rate? This is where the “holy grail” of real estate comes in: an assumable mortgage.

An assumable mortgage is a special type of loan that allows a buyer to take over the seller's existing mortgage, including their original interest rate, the remaining balance, and all the loan's terms. This is huge because many sellers who bought homes in 2020 or 2021 have interest rates as low as 2.5% to 3.5%. Imagine taking over a loan with that kind of rate!

How it Works in Practice:

- The “Find”: You need to look for homes where the seller has a specific type of loan – typically an FHA, VA, or USDA loan. Standard “Conventional” loans are almost never assumable.

- The Qualification: Just because you found a house with an assumable mortgage doesn't mean you automatically get it. You still have to qualify with the original lender based on your credit, income, and DTI. You need to prove you can handle the payments.

- The “Gap” Challenge: This is the biggest practical hurdle. Let's say a house is worth $500,000, but the seller only owes $300,000 on their assumable mortgage. You have a $200,000 “gap.” You must be able to come up with that $200,000 difference, either with cash or by taking out a second mortgage (which will likely be at a higher, current market interest rate).

Monthly Payment Comparison: Seeing the Savings

To really drive home why even a small difference in interest rates matters, let's look at a hypothetical $400,000 mortgage (this is the amount after your down payment).

| Feature | 6.0% Interest Rate | 5.5% Interest Rate | Monthly Savings | Total Interest (30 yrs) |

|---|---|---|---|---|

| Monthly (P&I) | $2,398 | $2,271 | $127 | |

| Total Interest (30 yrs) | $463,353 | $417,605 | $45,748 |

See that? An extra 0.5% might seem small, but it saves you $127 a month on your mortgage payment. Over 30 years, that's almost $46,000 in total interest savings! That's enough to buy a pretty nice car or cover a good chunk of college tuition.

Your Practical “Way Out” (Steps to Take)

If you're serious about trying to snag an assumable mortgage, here's how I'd recommend approaching it:

- Target Specific Listings: Your first move is to tell your real estate agent that you are specifically looking for homes with assumable mortgages. Ask them to search the Multiple Listing Service (MLS) for listings that mention “assumable,” “VA,” or “FHA” in the financing details.

- Negotiate the “Gap”: If you don't have all the cash needed for that equity gap (the difference between the sale price and the loan balance), you need to get creative. Sometimes, a seller might be open to “Seller Financing” for that portion. This means you'd pay the gap amount directly to the seller over a few years, often with an agreed-upon interest rate.

- Check for “Release of Liability”: If you're assuming a VA loan, it's crucial to make sure the seller gets a formal “release of liability” from the lender. This ensures they aren't on the hook if you happen to miss a payment down the line.

- Be Patient: I can't stress this enough: assuming a loan takes much longer than a standard home purchase. Expect an extra 30 to 60 days because the original lender has very little incentive to speed things up for a low-rate transfer.

The “Baseline” Reality Revisited

Just to reiterate, outside of finding an incredible assumable mortgage scenario, the absolute floor for a new 2026 mortgage is heavily influenced by the 10-Year Treasury Yield. Lenders will add their spread (typically around 1.7% to 2.0%) to cover their costs and make a profit. If those Treasury yields are hovering around 3.75%, it's just not physically possible for lenders to offer rates much lower than the 5.5% mark without losing money.

A Message for Your Real Estate Agent

If you're ready to go the assumable route, you need to be prepared. Sending your agent a well-crafted message can make all the difference. This shows you're serious and knowledgeable.

Hi [Agent's Name],

I’m very interested in finding homes with assumable mortgages, specifically FHA, VA, or USDA loans, as I’m aiming to secure a lower interest rate. Could you please search the MLS for listings in [Your Target Area] that mention “assumable” in the private remarks or financing fields?

Here’s the information I’d like to see:

- 📉 Current interest rate and the remaining balance of the existing loan

- 💡 An estimate of the equity gap (difference between the sale price and the loan balance)

- 🤝 Whether the seller is open to seller financing for any part of that gap, or if you can identify recent listings with these loan types that may not have been explicitly advertised as assumable yet

Thank you for your help with this specialized search!

Practical Tools for Your Search

While your agent is your go-to on the MLS, you can also explore these resources to find potential assumable inventory:

- Roam: This platform is built specifically to help you discover and buy homes with low-rate, assumable mortgages.

- AssumeList: Similar to Roam, this site lets you search for homes with VA, FHA, and USDA assumable mortgages, including those not yet widely advertised.

- Realtor.com Filter: You can use their search filters and try keywords like “assumable” or “assume” to narrow down standard listings, though results will vary.

Key “Watch-Outs” for 2026

Keep these things in mind as you navigate the mortgage market in 2026:

- Processing Time: As mentioned, expect 60 to 120 days for an assumption, unlike the typical 30-day closing for a standard purchase. The original lenders are not in a hurry.

- The Gap Solution: If the home has appreciated significantly, that gap needs to be covered. If cash is tight, a second mortgage is an option, but remember it will be at current, likely higher, rates.

- Proof of Funds: Be ready to provide immediate proof of funds to sellers to show you can cover that often substantial equity gap.

While the era of sub-3% fixed rates for everyone seems to be behind us for now, a strategic approach and a keen eye for assumable mortgages can still lead to significant savings.

And

Alabama’s newer A- rental vs Tennessee’s larger property with higher NOI. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- How to Get a 4% Interest Rate on a Mortgage in 2026?

- What Leading Housing Experts Predict for Mortgage Rates in 2026

- Mortgage Rate Predictions for 2026: What Leading Forecasters Expect

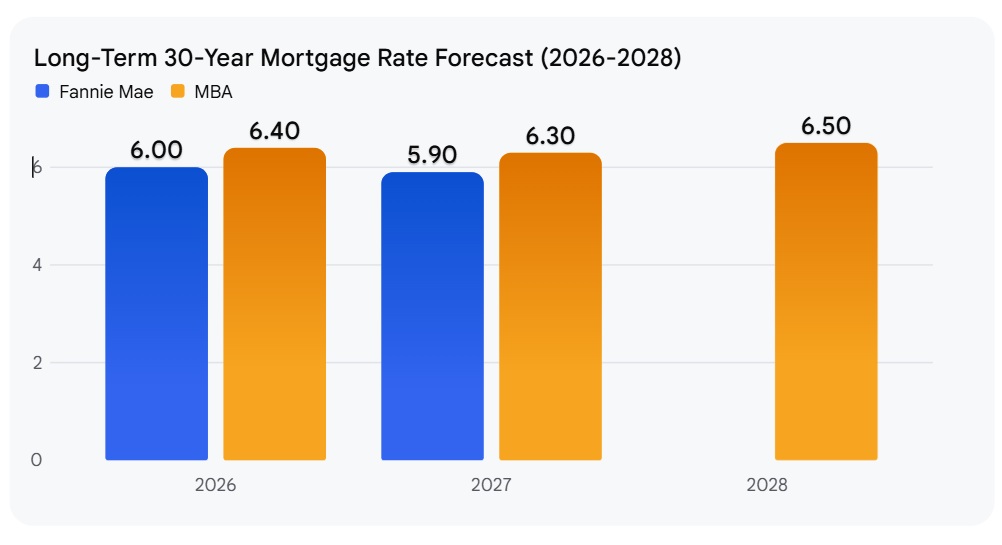

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?