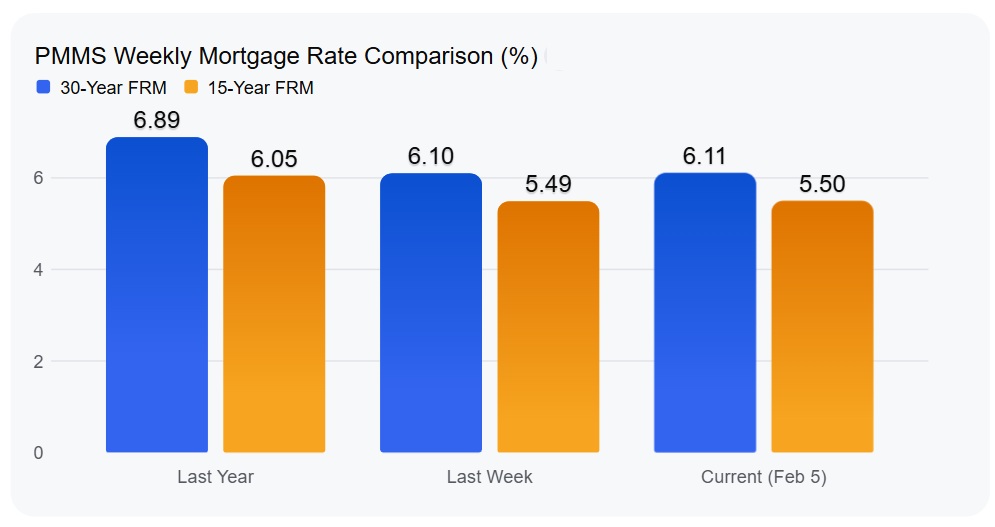

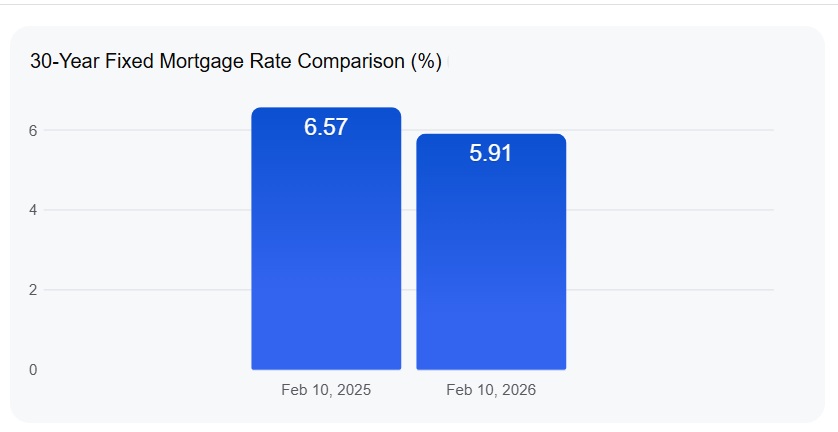

If you're looking to buy a home or refinance your mortgage, I have some good news that might just make you want to celebrate. As of February 10, 2026, the average 30-year fixed mortgage rate for home purchases has dropped to 5.91%. This is a notable improvement, sitting 66 basis points lower than the 6.57% rate we were seeing exactly one year ago. This shift means borrowing money for a home is considerably cheaper right now, opening doors for many potential buyers.

30-Year Fixed Mortgage Rate is Now 66 Basis Points Lower Than a Year Ago

This decline isn't just a small dip; it's a significant change that could dramatically impact how much house you can afford or how much you can save by refinancing. For years, we've been navigating a landscape of higher borrowing costs, and seeing rates fall below the crucial 6% threshold in early 2026 feels like a real turning point. In some areas, this translates to monthly payments being up to 8.4% lower than they were just twelve months ago, which can add up to thousands of dollars saved over the life of the loan.

What's Behind This Cheaper Borrowing?

It’s always fascinating to look beneath the surface and understand why these numbers change. From my perspective, this recent drop in mortgage rates is a confluence of several key economic factors, with the Federal Reserve playing a starring role.

The Fed's Role in Lowering Rates

The Federal Reserve has been actively trying to cool down the economy, and one of their main tools is adjusting the federal funds rate. They've made three rate cuts in late 2025, bringing the target range down to 3.50%–3.75%. When the Fed lowers its benchmark rate, it generally makes borrowing money cheaper across the board, and mortgage rates are certainly influenced by this. It signals a broader shift in monetary policy, aiming to stimulate economic activity without overheating it.

Inflation Finally Calming Down

Another huge piece of the puzzle is inflation. For a while there, it felt like prices were just going up and up, making everything more expensive. But recently, inflation has started to slow down, moving closer to the Fed's target of 2%. When lenders see that inflation is under control, they don't feel the need to charge as much for the risk of lending money. This cooling inflation is a big reason why those mortgage rates are able to come down.

Treasury Yields are Also Taking a Dip

Mortgage rates are closely tied to the yields on U.S. Treasury bonds, particularly the 10-year Treasury note. Just look at the numbers: a year ago, the 10-year yield was sitting at 4.46%. Now, by early February 2026, it's down to 4.25%. This trend indicates that investors are demanding less return for lending money to the government, which in turn allows mortgage lenders to offer lower rates to consumers.

A Slightly Softer Labor Market

It might sound strange, but a slightly weaker job market can actually be good news for mortgage rates. We saw a small uptick in the unemployment rate to 4.3% in late 2025. This signals that the economy isn't running at full blast, which can ease concerns about inflation getting out of control. When the economy cools a bit, it puts downward pressure on interest rates overall.

A Little Help from the Government

Beyond the typical economic forces, there was a specific government action in early 2026 that really helped push mortgage rates down. The federal government directed Fannie Mae and Freddie Mac, which are major players in the housing finance system, to purchase $200 billion in mortgage-backed securities. Think of these securities as bundles of mortgages that investors can buy. By stepping in to buy these, the government increased demand for mortgage debt. This helped to narrow the gap between what Treasury bonds pay and what mortgage loans cost, ultimately contributing to lower rates.

Market Dynamics: Buyers and Sellers

It's not just about the big economic picture, though. The actual supply and demand in the housing market itself plays a crucial role. I've noticed that as rates started to fall below that 6% mark, we saw a decrease in mortgage applications towards the end of 2025. This might seem counterintuitive, but when demand drops, lenders often become more competitive to attract borrowers. They lower their rates to make loans more appealing.

Furthermore, the dreaded “lock-in effect” – where homeowners with low existing mortgage rates are hesitant to sell and buy again at a higher rate – seems to be easing. As rates dipped below 6%, more homeowners might be listing their properties. This increased supply helps to stabilize the housing market and can also contribute to more competitive bidding, which is good news for buyers.

What’s the Outlook for the Rest of 2026?

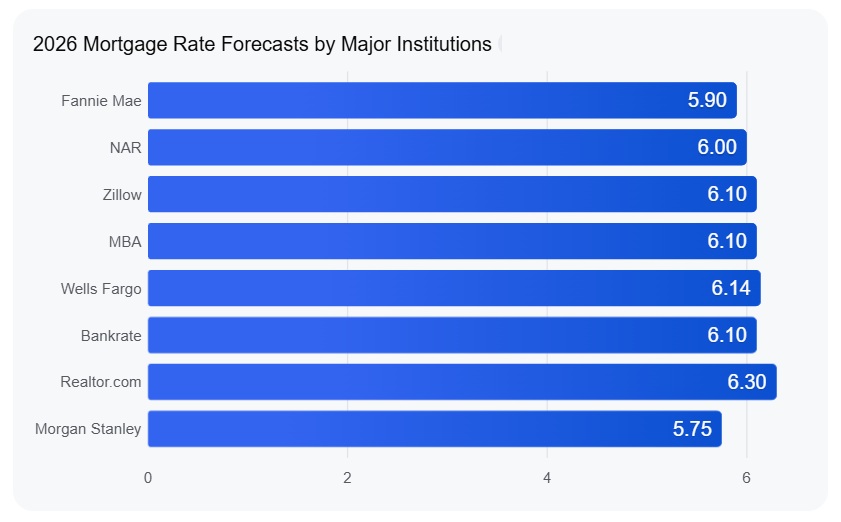

Looking ahead, the crystal ball for mortgage rates is always a bit cloudy, but here's what many experts are saying. The general consensus among major housing economists, as reported by Zillow, is that 30-year fixed mortgage rates will likely stay within a relatively tight range, hovering between 5.9% and 6.3% for the remainder of 2026.

While rates are currently just under 6%, it's important to remember that a return to the super-low rates we saw during the pandemic isn't expected. We might still see some ups and downs, or volatility, depending on how economic policies evolve.

Here’s a quick look at what some of the big names in housing economics are predicting:

- Zillow: Predicts rates will likely stay above 6% for the entire year.

- Fannie Mae: Forecasts a gradual easing of rates down to 5.9% by the last three months of 2026.

- Morgan Stanley: Offers a more optimistic view, anticipating a dip to 5.50%–5.75% by the middle of the year, followed by a slight increase.

- Mortgage Bankers Association (MBA): Expects rates to remain fairly steady, close to 6.1%, throughout the year.

Key Factors to Watch For the Rest of the Year:

- The Fed's Next Moves: After their rate-cutting spree in 2025, the Federal Reserve seems to be adopting a more cautious stance. Many believe their cutting cycle might be winding down, suggesting rates could stabilize.

- Economic Shocks: New trade policies, potential tax changes, or other government economic initiatives could cause ripples in the 10-year Treasury yield, which would directly impact mortgage rates.

- Housing Supply: While lower rates are helping to unlock some previously “locked-in” homeowners, inventory still remains a challenge. If rates continue to stay below 6%, it could be enough to encourage more people to sell, potentially balancing out the market and prices.

- Jobs Report: The ongoing health of the labor market is crucial. If unemployment starts to climb significantly, it could lead to a strong rally in bonds, pushing mortgage rates even lower. If the job market stays solid, rates are likely to stay “pinned” around the 6% level.

The Takeaway for You

So, what does all this mean for you? The bottom line is that the 30-year fixed mortgage rate has seen a substantial drop, now sitting at 5.91%, a significant 66 basis point decrease from February 2025. This favorable shift, fueled by Fed actions, easing inflation, lower Treasury yields, and even government support, creates a much more affordable borrowing environment. For anyone looking to buy a home or refinance an existing mortgage, early 2026 presents a really excellent opportunity to secure financing and explore the possibilities in the housing market. It feels like a much-needed breath of fresh air for aspiring homeowners!

And

Alabama’s newer A- rental vs Tennessee’s larger property with higher NOI. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- What Leading Housing Experts Predict for Mortgage Rates in 2026

- Mortgage Rate Predictions for 2026: What Leading Forecasters Expect

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?