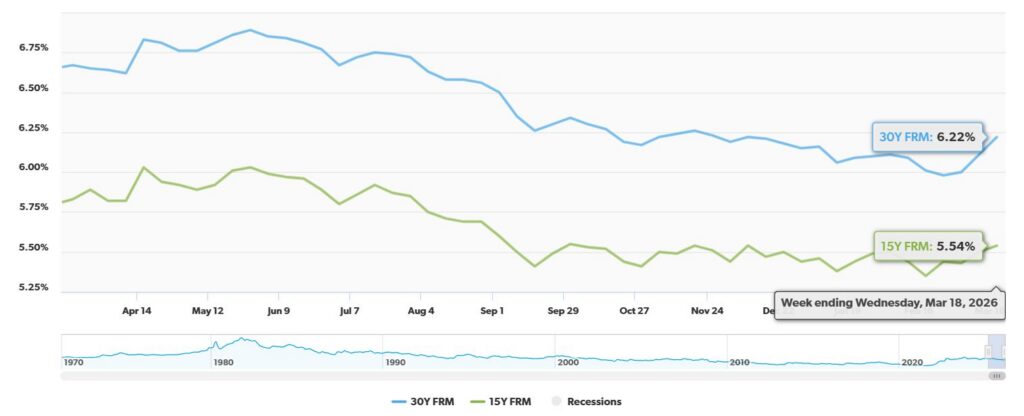

The dream of snagging a low mortgage rate seems to be fading fast. Geopolitical turmoil, particularly the recent conflict erupting in Iran, coupled with stubbornly high inflation, has sent average 30-year fixed mortgage rates climbing back into the 6.22% to 6.50% range, marking their highest point of the year. This isn't just a blip; it's a trend that's reshaping the housing market and making homeownership a tougher pill to swallow for many.

Geopolitical Jitters & Sticky Inflation Push Mortgage Rates Higher in 2026

It feels like just yesterday we were seeing those sub-6% rates, doesn't it? I remember thinking how much easier that made things for folks looking to buy or refinance. But the world is a complicated place, and right now, it's throwing some serious curveballs at our wallets, especially when it comes to getting a mortgage. From my perspective, this isn't just about numbers on a screen; it's about how global events directly impact the stability and affordability of what many consider the biggest investment of their lives.

The Double Whammy: War and Stubborn Prices

Let's break down what's really going on. Two major players are driving these higher mortgage rates:

- Geopolitical Conflict: The outbreak of war in Iran in late February 2026 has sent shockwaves through the global energy markets. We're seeing oil prices soar above $100 a barrel, a significant jump that impacts everything from how we get to work to the cost of building a house. When oil gets more expensive, so does transportation, manufacturing, and pretty much anything that relies on fuel. This ripple effect is unavoidable.

- “Sticky” Inflation: All this energy price chaos naturally fuels inflation fears. It’s not just a temporary spike; economists are worried this is the kind of inflation that likes to stick around. So much so, the Federal Reserve has revised its inflation forecast for 2026 upwards to 2.7%. This “stickiness” is key. It means the central bank might have to keep interest rates higher for longer to get prices back under control.

The Fed's Balancing Act and Treasury Yields

The Federal Reserve is in a tough spot. On March 18th, they decided to hold their benchmark interest rate steady at 3.50%–3.75%. This signals a cautious approach. They're not rushing to cut rates because they're worried about inflation. In fact, they're now projecting only one rate cut for the rest of 2026.

Why does the Fed's rate matter for your mortgage? Well, the Fed's rate influences all sorts of borrowing costs. And a big driver for mortgage rates is the yield on the 10-year Treasury note. Think of this as a key benchmark. With all this uncertainty, investors are demanding a higher return for holding these government bonds, pushing the yield up to around 4.25%–4.35%. When Treasury yields climb, mortgage lenders usually follow suit, repricing their loans to reflect the higher cost of borrowing.

Mortgage Rates Today: A Snapshot

As of late March 2026, here's what we're seeing for some common loan types:

| Loan Type | Average Rate Range |

|---|---|

| 30-Year Fixed | 6.25% – 6.50% |

| 15-Year Fixed | 5.75% – 5.78% |

| 30-Year Refinance | 6.70% – 6.90% |

| 30-Year VA | 5.81% – 5.85% |

These figures are a stark reminder of how much things can change. Just a few months ago, rates looked much more favorable.

Expert Opinions: What's Next?

The crystal ball isn't perfectly clear, and different experts have slightly different views on where rates are headed for the rest of 2026.

- Fannie Mae has a more optimistic outlook, predicting rates will average around 6.0% for the year.

- The Mortgage Bankers Association (MBA) anticipates a slightly higher average of 6.4%.

- Redfin is projecting a 2026 average of 6.3%.

- Morgan Stanley, however, suggests a potential dip to 5.75% by mid-year if inflation eases significantly. But they rightly point out that geopolitical risks are a huge wildcard that could easily change that picture.

From my experience, these forecasts are educated guesses at best. The global situation is so fluid. Any major geopolitical development or an unexpected shift in inflation data can send these projections out the window.

Regional Divide: Some Markets Cool, Others Hold Strong

The impact of these higher mortgage rates isn't felt equally across the country. It's creating a real divide:

Cooling Markets (South and West):

These areas are feeling the pinch the most. With higher-priced homes and tighter affordability, rising rates can quickly push buyers to the sidelines.

- Price Declines: Cities in Florida and Texas are leading the nation in home price corrections. We're seeing projections for significant drops in places like Cape Coral, FL (-10.2%) and North Port, FL (-8.9%). Even California isn't immune, with Stockton, CA facing a projected 4.1% decline.

- Inventory Surge: In places like Las Vegas, Seattle, and Phoenix, active home listings have jumped over 20% compared to last year. This is because higher rates are making buyers more hesitant, and new home builders are still bringing properties to market, leading to an oversupply in some spots.

Resilient Markets (Northeast and Midwest):

These regions are proving surprisingly resilient, largely due to a persistent lack of homes for sale.

- Strong Appreciation: While prices aren't skyrocketing, they're still growing. This is because inventory levels remain critically low. In some cities, like Hartford, CT, listings are up to 74% below pre-pandemic levels.

- Top Growth Projections: Cities like Toledo, OH (+13.1%), Syracuse, NY (+12.4%), and Scranton, PA (+10.9%) are expected to see the highest price increases this year, fueled by this scarcity.

- New York Metro: Even here, a more modest 1.5% growth is forecast for home values in 2026.

Buyer Leverage: A Shift in Power?

While national home price growth has slowed to a crawl—just 0.7% to 1.4% year-over-year as of early 2026—it's important to note that the market hasn't completely “crashed.” Instead, this higher-rate environment is subtly shifting power back to buyers in specific ways:

- Days on Market: Homes are taking longer to sell. In February 2026, the average home sat on the market for 66 days, compared to just 58 days last year. This gives buyers more time to think and negotiate.

- Price Cuts and Concessions: Sellers are increasingly having to lower their asking prices or offer incentives to get deals done, especially in those markets that have seen significant price run-ups.

- The “Locked-In” Effect: This is a big one. Many homeowners who locked in ultra-low mortgage rates of 3%–4% in previous years are understandably reluctant to sell. They don't want to trade a super-low rate for a much higher one. This prevents a massive flood of inventory from hitting the market, which is a key reason why national prices aren't plummeting.

Here's a look at how different sources are forecasting national home price growth:

| Source | 2026 Price Forecast |

|---|---|

| Realtor.com | +2.2% |

| Fannie Mae | +1.3% |

| Zillow | +0.9% |

| J.P. Morgan | 0.0% (Stall) |

Looking Ahead

The message from the market is clear: geopolitical stability and inflation control are the primary drivers for what happens to mortgage rates next. Until we see a significant easing in those areas, expect rates to remain elevated. For potential buyers and homeowners, it means more caution, more negotiation, and a continued appreciation for the markets that demonstrate fundamental strength even in challenging times. It's a complex equation, and I'll be watching closely to see how these factors play out.

VS

Georgia’s affordable rental with higher cap rate vs Florida’s A‑rated property with stability. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- The Real Reason Mortgage Rates Are Rising Back in 2026

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?