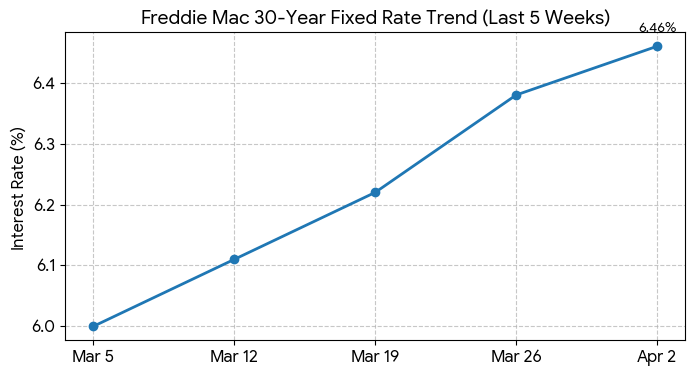

As of April 10, 2026, the numbers are looking a bit brighter for those dreaming of homeownership or looking to refinance. Today, the average 30-year fixed mortgage rate has dropped to 6.08%, according to Zillow. This is a welcome relief, and it’s not the only good news. The 15-year fixed mortgage rate is also down, sitting at 5.60%. I’ve been watching this market for a while, and these lower rates are exactly what many people have been hoping for.

It feels like just yesterday when rates were creeping up, making it harder for families to afford a new home. Seeing them dip below the 6% mark for the popular 30-year loan is a significant step in the right direction. For anyone holding a large mortgage, even a small drop can mean saving quite a bit of money over the life of the loan. Think about it: for a $400,000 mortgage, a drop from, say, 6.37% to 6.08% can shave off a nice chunk of your monthly payment, freeing up money for other important things.

Today’s Mortgage Rates – April 10, 2026: A Welcome Drop for Homebuyers

What’s Happening with Mortgage Rates Right Now?

Let’s dive a little deeper into these numbers and what they mean.

Here’s a quick snapshot of today’s rates, as reported by Zillow for April 10, 2026:

| Loan Type | Today's Rate |

|---|---|

| 30-Year Fixed | 6.08% |

| 20-Year Fixed | 5.97% |

| 15-Year Fixed | 5.60% |

| 5/1 ARM | 6.35% |

| 7/1 ARM | 6.29% |

| 30-Year VA | 5.74% |

| 15-Year VA | 5.38% |

| 5/1 VA | 5.53% |

You can see that not only the fixed-rate loans are seeing improvements, but adjustable-rate mortgages (ARMs) are also following suit. VA loans, which are a fantastic benefit for our veterans, are also trending lower. This broad decrease across different loan types suggests a positive shift in the lending environment. It makes it easier for a wider range of people to find a mortgage that fits their budget.

Why Are Rates Moving Today?

Understanding why rates change is crucial, and it’s what I always try to explain to my clients. It's not just random. Several big things are happening that influence these numbers.

Think of it like this: mortgage rates tend to follow what’s happening with big government loans called Treasury bonds, especially the 10-year Treasury note. When the yield on those bonds goes down, mortgage rates usually follow.

- Calmer Global News: A big factor influencing markets right now is a recent ceasefire agreement between the U.S. and Iran. When there’s less worry about international conflict, markets tend to calm down. This can lead to lower interest rates on bonds, and that, in turn, often means lower mortgage rates for us.

- Bond Market Movements: As I mentioned, mortgage rates are really tied to the 10-year Treasury yield. We’ve seen this yield ease back to around 4.26%. This is a key indicator that lenders are watching very closely.

- Job Growth: The economy is still showing strength. The March jobs report showed 178,000 new jobs were created. This is generally good news for the country, showing we’re building a strong economy. However, when the economy is robust and lots of people have jobs, the Federal Reserve (often called the “Fed”) might be less likely to lower its main interest rates. They look at these job numbers – and if growth is strong, they might decide to keep rates where they are for a while longer instead of cutting them.

What Does the Future Hold for Mortgage Rates?

Predicting the future is always tricky, especially with money matters! But economists and big financial groups have their ideas. Right now, there’s a bit of a split in what they expect.

- The Mortgage Bankers Association (MBA) is predicting that the 30-year fixed rate will mostly stay around 6.30% for the rest of 2026. They’re suggesting it might move up and down a bit, but won’t drastically change.

- On the flip side, Fannie Mae, another big player in the housing market, is more optimistic. They think there’s a good chance the 30-year fixed rate could actually drop below 6.00% by the end of the year.

This difference in opinion shows just how uncertain things can be. We’re seeing good signs like potentially lower inflation and that easing in bond yields. But, strong economic news and any new global worries could keep things from going down too much. It’s a balancing act, and lenders have to be careful.

My Take on Today’s Rates

From where I stand, seeing the 30-year fixed rate at 6.08% and the 15-year fixed at 5.60% today, April 10, 2026, is a real positive development. It’s not a massive drop, but it’s enough to make a noticeable difference in monthly payments. This improved affordability could encourage more people to finally make that move they’ve been putting off.

What I always advise people is to stay informed. Mortgage rates can change quickly based on what’s happening in the world and in our economy. Keep an eye on those Treasury yields and any news about the Fed's plans. For now, though, this dip is a breath of fresh air. It’s a good reminder that even in a sometimes challenging housing market, opportunities for better rates do come along.

VS

Georgia’s affordable rental with higher cap rate vs Florida’s A‑rated property with stability. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?