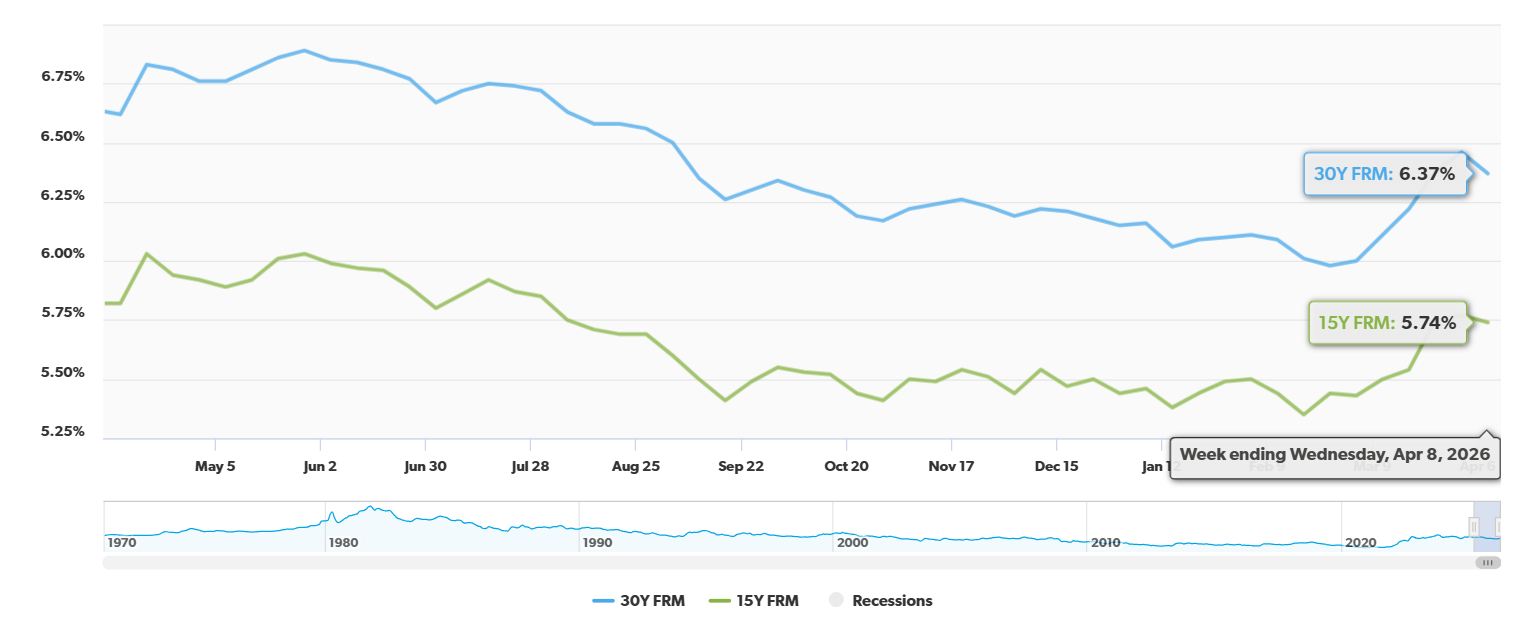

As of Thursday, April 16, 2026, you'll find mortgage rates holding comfortably in the low-six percent range. After a period of unpredictable shifts, the 30-year fixed mortgage rate has nudged up slightly to 6.08%, and the 15-year fixed rate has similarly climbed to 5.58%, according to the latest data from Zillow. This stability offers a much-needed breath of fresh air for anyone looking to buy a home or refinance their existing mortgage.

Today's Mortgage Rates, April 16: Rates Hold Steady Around 6% After Volatility

It’s been a bit of a rollercoaster lately, hasn't it? Just a month ago, we saw rates making some pretty sharp turns, largely due to global events that had everyone a little on edge. But now, things have settled down, and believe it or not, some lenders are even advertising rates just shy of that 6% mark. This quiet period is a good chance for folks to really dig in and figure out what makes the most sense for their financial situation.

What the Numbers Are Showing Us Today (April 16, 2026)

To give you a clear picture, here’s a breakdown of the rates we’re seeing right now. These are the numbers that matter if you're talking about getting a mortgage this week:

| Loan Type | Interest Rate |

|---|---|

| 30-Year Fixed | 6.08% |

| 20-Year Fixed | 5.83% |

| 15-Year Fixed | 5.58% |

| 5/1 ARM | 6.12% |

| 7/1 ARM | 6.02% |

| 30-Year VA | 5.50% |

| 15-Year VA | 5.29% |

| 5/1 VA | 5.50% |

Why Are Rates Where They Are? Understanding the Market’s Pulse

It’s always good to know why things are happening, especially when it comes to something as big as a mortgage. Recently, we saw mortgage rates jump up. A big reason for that was an increase in oil prices, pushing them close to $100 a barrel. This understandably sparked worries about inflation, which, in turn, tends to bump up interest rates, particularly the yields on government bonds like the 10-year Treasury.

Now, in early April, we've seen those concerns ease a bit. As the situation in Iran has become less of a focus, markets have calmed down. This is the period of relative quiet I mentioned, and it’s a great time for borrowers who have been waiting to see if rates would become more predictable.

It's also crucial to keep an eye on what the Federal Reserve is doing. They recently decided to keep the federal funds rate steady, between 3.50% and 3.75%. Everyone is now listening closely for hints from their upcoming meeting on April 28th-29th. Will they start thinking about lowering rates? That’s the big question on many minds.

Looking Ahead: Expert Guesses for the Rest of 2026

Experts are pretty much in agreement that we’re likely to see a bit of a push and pull in the mortgage rate market for the remainder of 2026. On one hand, we have the anticipation of potential rate cuts from the Fed, which would generally push mortgage rates down. On the other hand, we still have those lingering concerns about inflation, especially anything driven by energy prices, which could keep rates from dropping too much.

Here’s a snapshot of what some leading institutions are predicting for the 30-year fixed mortgage rate by the end of 2026:

- Fannie Mae: They’re forecasting a rate around 5.7% by the end of the year.

- Mortgage Bankers Association (MBA): Their average prediction for 2026 is closer to 6.3%.

- General Consensus: Most analysts seem to think rates will likely stay within a comfortable range, somewhere between 5.5% and 6.5%.

From my perspective, having worked in this space for a while, this range feels pretty realistic. We’re not likely to see those super low rates we experienced a few years back, but we’re also probably not going to see the kind of spikes that occurred earlier this spring. It’s about finding that sweet spot.

My Two Cents: What This Means for You

So, what’s the big takeaway from all this on April 16, 2026? Mortgage rates are hanging out in that pleasant low-six percent zone. The 30-year fixed rate is at 6.08%, and if you’re looking at a shorter term, the 15-year fixed is at 5.58%. While these aren’t dramatic shifts, the fact that they’re steady is a big deal. It’s a rare moment of predictability after a period that felt like navigating a choppy sea.

As we look down the road, the predictions suggest rates will probably stay somewhere between 5.5% and 6.5%. The real deciding factors will be how inflation behaves and what move the Federal Reserve makes.

For anyone in the market to buy a home or thinking about refinancing, this current stability could be a golden opportunity. It’s a chance to lock in a rate that feels manageable before any unexpected economic news or global events shake things up again. My best advice? Talk to a trusted mortgage professional. They can help you understand your options and make the best decision for your personal financial journey. Don’t wait too long to explore; this calm window might not last forever.

VS

Georgia’s affordable rental with higher cap rate vs Florida’s A‑rated property with stability. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?