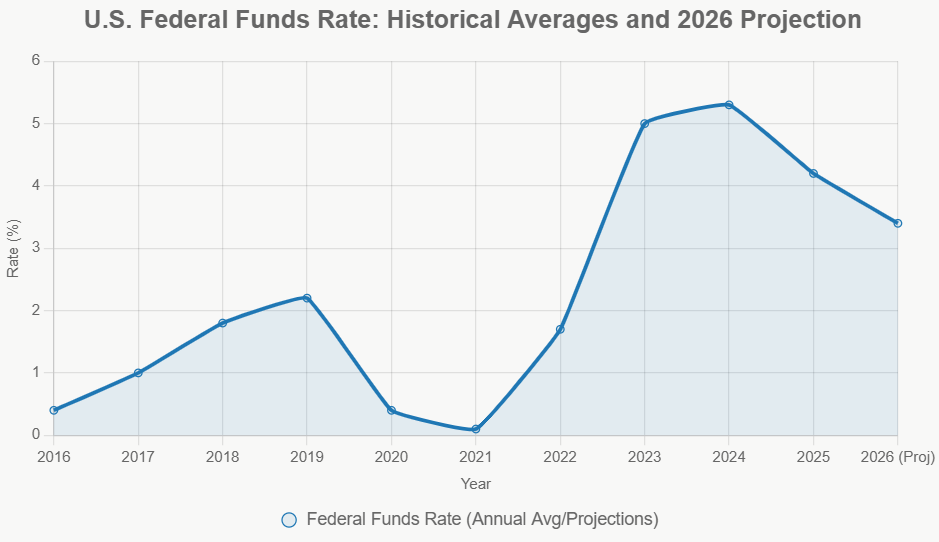

It’s the start of a new year, and the Federal Reserve has made its first big move – or rather, no move. In their January 28, 2026 meeting, the Fed decided to keep interest rates exactly where they are, in the 3.5% to 3.75% range. This might sound like just another boring financial headline, but trust me, it’s a pretty big deal, especially with all the talk coming from the White House lately.

As someone who’s watched this stuff for a while, I can tell you this decision wasn’t made lightly. The Fed could have easily bowed to pressure to start cutting rates, but they seem to be taking a deep breath and waiting to see how everything plays out. This shows they’re sticking to their guns, focusing on the numbers rather than the noise.

No Fed Rate Cut: Interest Rates Remain Unchanged in January 2026

Why the Pause? It’s All About Those Numbers

The Fed’s main job is to keep prices stable and the economy humming along. They do this by tweaking interest rates. When they lower rates, it makes it cheaper for people and businesses to borrow money, which usually gets people spending and the economy growing. When they raise rates, it’s like tapping the brakes, making borrowing more expensive to slow down a stuffy economy and fight rising prices.

After cutting rates three times in the latter half of 2025, it seems they’ve decided enough is enough for now. They’re watching the inflation rate very closely. Even though it’s come down a lot from its scary highs in 2023 (it was over 4% then; now core inflation is above 2.5%), it’s still not at their target of 2%. The latest numbers for December 2025 showed prices went up 3.1% compared to a year ago, which is good, but still a bit too warm for their liking.

The job market is another big piece of the puzzle. We’re not seeing the huge hiring booms we used to. The unemployment rate has been steady at 4.2%, and while people are still getting raises, the pace has slowed to about 3.8% a year. This is a good thing because it means businesses aren’t feeling pressured to hike prices just to cover ever-increasing wages. The fact that there are fewer job openings than there used to be also signals that things are cooling down, which is what the Fed wants to see when inflation is still a concern.

And let’s look at the economy’s overall speed. The Gross Domestic Product (GDP), which is basically the total value of everything we produce, grew at a 1.6% annual rate in the last three months of 2025. That’s not terrible, but it’s definitely not a sprinting pace. People are still spending, which is keeping things going, but businesses seem to be pulling back a bit on their investments. It’s a bit of a mixed bag, which is probably why the Fed is sitting tight.

What About Trump’s Pressure?

Now, let’s talk about President Trump. We all know he’s never been shy about letting his opinions be known, and the Federal Reserve, and especially its Chair Jerome Powell, have been frequent targets. During his presidency, Trump often publicly urged the Fed to lower interest rates, arguing it would help the economy and boost his political standing. This time around, as the Fed held rates steady, the pressure is still there. We’ve even heard rumblings about a potential DOJ investigation and speculation about who might be the next Fed Chair. Trump is expected to nominate a new Fed Chair sometime this year, which adds a layer of uncertainty about where the Fed might go in the future.

It’s a tough spot for Chair Powell and the other Fed members. They’re supposed to be independent, making decisions based purely on economic data, not politics. But when the President of the United States is actively calling for different actions, it’s hard to ignore completely. My take on it? The Fed’s decision to hold rates steady, despite this political pressure, shows a commitment to their mandate of price stability. They’re signaling that they won’t be swayed by public opinion or political favors. This independence is crucial for the long-term health of our economy.

The Fed’s tone was described as cautiously dovish. That means while they aren’t ready to cut rates now, they are leaning towards cutting them in the future, likely in mid-2026, maybe around June. Markets had already expected this, so there wasn't a big shock.

What’s Next? Eyes on the Data

The Fed keeps saying they’re going to wait and see. This means how the economy behaves in the coming months will be the deciding factor in their next move. They said that any future rate changes will depend on the incoming data.

The Fed’s own projections from their last meeting in December 2025 still show they expect to make 1 or 2 rate cuts in 2026. But the timing is the big question mark.

Their next meeting is coming up on March 18-19, 2026, and that will be another key event to watch.

The Bigger Picture: Balancing Act

Ultimately, the Fed is trying to walk a very fine line. They need to bring inflation down without tipping the economy into a recession. With current inflation still above their target and economic growth slowing a bit, they’ve chosen patience. It’s not about being stuck; it’s about being deliberate. They’ve made good progress on inflation, but they haven’t declared victory yet. And with all the political talk swirling around, their independence and focus on the data are more important than ever.

The Fed’s rate decisions can create market volatility, but turnkey rentals continue to deliver reliable cash flow and appreciation. Investors in 2026 are focusing on real estate as a hedge against uncertainty.

Norada Real Estate helps you secure turnkey properties designed for immediate income and long‑term growth—so your portfolio stays strong regardless of Fed policy shifts.

Want to Know More?

Explore these related articles for even more insights:

- Fed Interest Rate Predictions for the Next 3 Years: 2026-2028

- The Fed After Jerome Powell: Who Could Drive Rate Cuts in 2026?

- Why Your Loan Payment Isn’t Budging Despite Recent Fed Rate Cut

- How Does the Recent Fed Rate Cut Impact Your Personal Finances

- How Will Today's Fed Rate Cut Impact Mortgage and Refinance Rates

- Fed Interest Rate Decision Today: Latest News and Predictions

- Fed Meeting Today is Poised to Deliver the Third Interest Rate Cut of 2025

- Fed Interest Rate Predictions Signal 70% Chance of December 2025 Cut

- Fed Meeting Minutes Expose Divide: Why December Rate Cut Odds Are Fading Fast

- Fed Interest Rate Predictions for the December 2025 Policy Meeting

- Fed Signals Growing Reluctance to Interest Rate Cut in December 2025

- Fed Cuts Interest Rate Today for the Second Time in 2025

- Fed Interest Rate Forecast for the Next 12 Months

- When is Fed's Next Meeting on Interest Rate Decision in 2025?

- Market Reactions: How Investors Should Prepare for Interest Rate Cut

- Impact of Interest Rate Cut on Mortgages, Car Loans, and Your Wallet