Mortgage rates have seen a significant drop over the past year. We've gone from an average of 6.76% to a much more palatable 5.78%, and for the first time in nearly four years, the benchmark 30-year fixed rate has dipped below 6%. This is a game-changer for the housing market, and I want to dive into what this really means for you.

Right now, the shift is decidedly in favor of buyers and homeowners looking to refinance. This isn't just a small blip; it's a sign that the market is responding to economic changes, and it could be your moment to make a move.

Mortgage Rates Fall from 6.76% to 5.78% Over the Past Year

A Breath of Fresh Air for the Housing Market

For a long time, those high mortgage rates acted like a freeze on the housing market. Buyers were priced out, sellers were hesitant to list because they’d have to buy again at a higher rate, and bidding wars, while still happening for desirable properties, definitely cooled from their frenzy. When mortgage rates are high, even a seemingly small difference in percentage points can translate into hundreds of dollars more on your monthly payment.

Think about this: For a typical $400,000 loan, that drop from an average of, say, 6.85% down to around 6% saves a homeowner approximately $220 per month in principal and interest payments. Over the life of a 30-year loan, that's thousands upon thousands of dollars back in your pocket. That's money that can go towards renovations, savings, or simply a better quality of life.

Why the Big Drop? Tracing the Trend

So, how did we get here? The most significant driver of this decline is the action taken by the Federal Reserve. In late 2025, they initiated a series of interest rate cuts, bringing the federal funds rate down. While the federal funds rate isn't directly the mortgage rate, it's a major influencing factor. When the Fed lowers its target rate, it signals a loosening of monetary policy, which tends to trickle down to other borrowing costs, including mortgages.

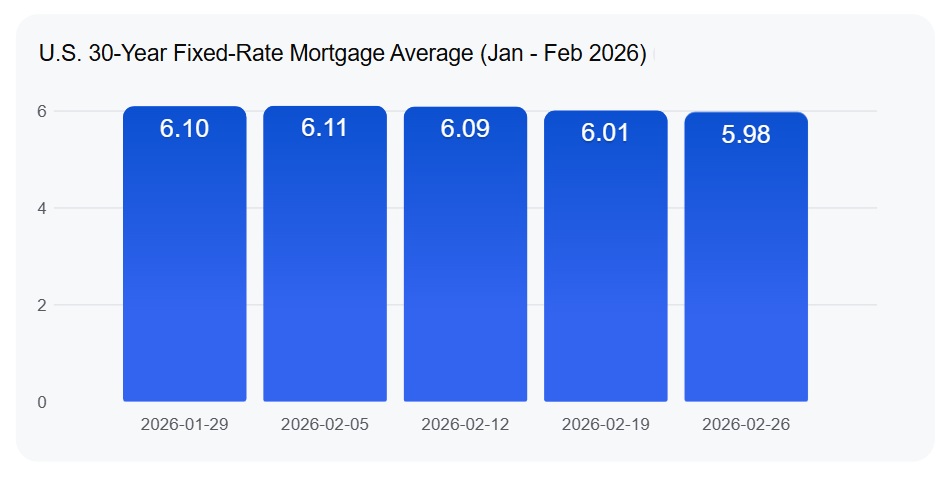

According to data from Freddie Mac, the average 30-year fixed mortgage rate has specifically fallen from 6.76% in February 2025 to 5.98% as of February 26, 2026. This is a substantial shift and marks a significant psychological victory for the market.

Here’s a snapshot of the current averages as of February 27, 2026, also reported by Freddie Mac:

- 30-Year Conventional: 5.964%

- 15-Year Conventional: 5.291%

- 30-Year FHA: 5.881%

- 30-Year VA: 5.638%

Each of these numbers is lower than they were a year ago, offering more inviting options for different types of homebuyers.

What's Driving Mortgage Rate Volatility in 2026?

While the overall trend is encouraging, the reality is that mortgage rates don’t move in a perfectly straight line. There are still factors that can cause them to sway, even in 2026. From my perspective as someone who keeps a close eye on the housing market, this year is particularly interesting because of a few key influences:

- Federal Reserve Leadership Speculation: Heads up, as there's chatter about a potential leadership change at the Fed. Any uncertainty about who will be steering the ship and their approach to interest rates can create ripples in the mortgage market. Will a new leader prioritize keeping rates low, or continue a more cautious path? This speculation alone can make rates jump or dip.

- The 10-Year Treasury Yield Spread: Mortgage rates are closely tied to the interest paid on 10-year U.S. Treasury bonds. However, the gap or spread between these two can widen or narrow. Things like investor confidence and even government directives on mortgage-backed securities can influence this spread, causing mortgage rates to move more independently from Treasury yields at times.

- Mixed Signals from the Labor Market: The job market is crucial. While we've seen growth in some sectors, others are showing signs of slowing down. If employment numbers are stronger than expected, it might make the Fed pause on further rate cuts, leading to a quick spike in mortgage rates. Conversely, softer job reports can signal room for more rate reductions.

- Inflation Watch: Everyone is watching inflation reports, like the Consumer Price Index (CPI). If inflation doesn't seem to be heading steadily towards the Fed's 2% target, it can signal to lenders and investors that rates might need to stay higher for longer. Any unexpected jump in inflation can immediately push mortgage rates up.

- Global Events: Sometimes, events happening far away can have a direct impact on your mortgage rate. If there's global uncertainty, investors often flock to U.S. Treasury bonds as a safe bet. This increased demand can, paradoxically, drive down bond yields and, consequently, pull mortgage rates lower for a period.

Expert Forecasts for the Rest of 2026

So, where are we headed? The general consensus from major players like Fannie Mae and the Mortgage Bankers Association (MBA) is that rates are likely to stabilize or even decline slightly further through the remainder of 2026. Many experts are predicting an average rate hovering around 6.0% to 6.1%.

Here's a look at some expert projections:

| Source | Projected Rate Range | Key Assumption |

|---|---|---|

| Fannie Mae | ~5.9% | Stable labor market; inflation near 2% |

| Morgan Stanley | 5.5% – 5.75% | Possible mid-year dip due to economic softening |

| Mortgage Bankers Association | ~6.4% | Continued but very gradual inflation moderation |

| Redfin | ~6.3% | Moderate labor market weakness without a recession |

While there are slight variations, the overarching theme is one of relative stability with potential for further modest decreases, rather than a sharp upward trend.

Is Now the Time to Buy or Refinance?

For many, this period of lower mortgage rates presents a fantastic opportunity.

- For Buyers: You can potentially afford a larger loan amount than you could a year ago, which might mean a nicer home, a better location, or simply more breathing room in your monthly budget. The key is to get pre-approved and understand exactly what you can afford.

- For Refinancers: If you have an existing mortgage with a rate significantly higher than current offerings, refinancing could save you substantial money over time. It’s worth exploring whether the costs of refinancing outweigh the monthly savings.

And

Alabama’s newer A- rental vs Tennessee’s larger property with higher NOI. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Will Mortgage Rates Drop to 5% in 2026: Expert Forecast

- How to Get a 3% Mortgage Rate in 2026 With Assumable Mortgages?

- How to Get a 4% Interest Rate on a Mortgage in 2026?

- What Leading Housing Experts Predict for Mortgage Rates in 2026

- Mortgage Rate Predictions for 2026: What Leading Forecasters Expect

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?