Will the housing market crash again? The short answer is: probably not in 2025, and not anytime soon after that either. While the ghost of the 2008 financial crisis still haunts our collective financial consciousness, the current housing market, as of May 2025, possesses a different set of characteristics that make an imminent collapse improbable. I understand the anxiety – I feel it too! Home prices are high, and interest rates aren't exactly inviting. But let's dig into the details and see why most experts (and myself) believe a full-blown crash isn't in the cards… at least for now.

Housing Market Crash: When Will It Crash Again?

A Look Back: Lessons From Housing Market Crashes

To understand where we might be headed, it’s important to understand where we've been. Housing market crashes aren't exactly new. They’ve happened throughout history, each time with its own unique set of triggers. However, there are some common threads:

- Excessive Speculation: When everyone believes prices will only go up, irrational exuberance takes over. People buy homes not to live in, but to flip them for a quick profit. This inflates prices artificially.

- Lax Lending Standards: This is where things get really dangerous. When banks and lenders make it too easy to borrow money, even for those who can't really afford it, you're creating a recipe for disaster.

- Economic Imbalances: A strong economy can support a healthy housing market. But if other parts of the economy are weak, or if there are underlying problems like high unemployment or stagnant wages, the housing market becomes vulnerable.

The most recent and painful example is, of course, the 2008 financial crisis. Remember that? I certainly do. Here are a few of the ingredients that baked that particular cake of financial disaster:

- Subprime Lending: Banks were giving out mortgages like candy, even to people with bad credit or no income. These were called subprime mortgages, and they were often packaged with low introductory rates that would later skyrocket.

- Speculative Bubble: As home prices soared, people started buying homes solely as investments, hoping to flip them for a quick profit. This drove prices even higher, creating an unsustainable bubble.

- Complex Financial Instruments: Banks bundled these risky mortgages into complex investments called mortgage-backed securities. These were sold to investors all over the world, spreading the risk far and wide. When the housing market collapsed, these securities became toxic assets, triggering a global financial crisis.

Where We Are Today: The 2025 Housing Market

Alright, so what does the housing market look like right now, in May 2025? Here's a snapshot:

- High Home Prices: Yes, home prices are high. The average home value nationwide is around $357,138, and while the growth rate is slowing, it's still growing.

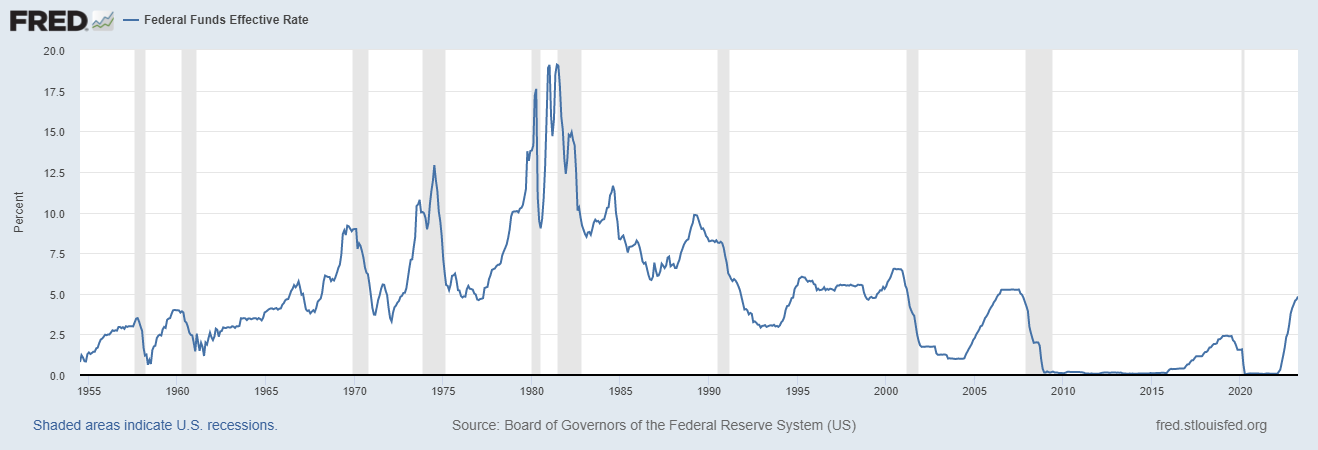

- Elevated Mortgage Rates: Interest rates are definitely higher than they were during the pandemic, hovering between 6.5% and 7% for a 30-year fixed-rate mortgage.

- Low Inventory: This is a big one. There simply aren't enough homes for sale. The current supply of existing homes is only about 3.5 months, which is well below the 4-6 months considered a balanced market.

- Strong Demand: Despite the high prices and interest rates, there's still strong demand for homes, particularly from millennials who are now entering their prime home-buying years.

I can tell you one thing for sure, it isn't easy saving up a downpayment with all these factors at play!

Key Factors Shaping the Future

The housing market isn't some monolithic entity. It's a complex system influenced by a whole bunch of different factors. Understanding these factors is crucial to making any kind of prediction about the future:

- Interest Rates: Interest rates are the gatekeepers of affordability. When rates go up, it becomes more expensive to borrow money, which cools down demand. Experts generally predict that mortgage rates will remain in the 6-7% range throughout 2025.

- Housing Supply: As I mentioned earlier, the lack of homes for sale is a major factor supporting prices right now. New construction is picking up, but it's not enough to meet the pent-up demand.

- Economic Conditions: A strong economy with low unemployment is good for the housing market. People are more likely to buy homes when they feel secure in their jobs and finances. The U.S. unemployment rate is currently around 4.2%, which is relatively low.

- Government Policies: Government policies can have a big impact on the housing market, both directly and indirectly. Things like tax incentives for homeownership, regulations on lending, and even trade policies can all play a role.

- Demographic Trends: Demographics is destiny, as they say. The millennial generation is a huge demographic force, and their housing preferences and purchasing power will continue to shape the market for years to come.

What the Experts Are Saying

So, what do the people who spend their days analyzing the housing market think? Here's a rundown of some expert predictions for 2025:

| Source | Home Price Growth (2025) | Key Notes |

|---|---|---|

| Zillow | 0.9-1% | Modest growth due to low supply and high demand. |

| Fannie Mae | 4.1% | Expects slight rate declines to improve affordability. |

| Mortgage Bankers Association | 1.3% | Predicts stable but slow growth. |

| National Association of Realtors (NAR) | 3% | Anticipates increased sales with lower rates. |

The general consensus seems to be that we're unlikely to see a major crash in 2025. Most experts are predicting modest price growth or at least stability. They point to the low inventory, strong demand, and relatively healthy economy as reasons to be optimistic.

However, There are Always Risks

Now, I don't want to sound too Pollyannaish. The housing market is a complex beast, and there are always risks to consider. Here are a few potential triggers that could lead to a downturn:

- A Sharp Increase in Interest Rates: If mortgage rates were to suddenly jump to, say, 9% or higher, that would definitely put a damper on demand and could lead to price declines.

- An Economic Downturn: A recession with widespread job losses would be bad news for the housing market. People who lose their jobs may struggle to make their mortgage payments, leading to foreclosures and lower prices.

- Policy Shocks: Unexpected changes in government policies, such as aggressive tariffs or a sudden privatization of Fannie Mae, could disrupt the market.

- External Factors: Geopolitical events, global economic crises, or even natural disasters could all have an impact on the housing market.

Don't Forget Local Markets

It's important to remember that the housing market is not uniform across the country. Local market conditions can vary widely. Some areas may be more vulnerable to a downturn than others. For example, a recent study identified several cities in Florida as having a higher risk of price declines in 2025 due to rising inventory and slowing demand.

Public Fear vs. Reality

Despite the relatively optimistic outlook from experts, many people are still worried about a housing market crash. A recent survey found that a significant percentage of Americans fear a crash in 2025. This fear is driven by concerns about inflation, rising property taxes, and the overall economic outlook. While these concerns are valid, they don't necessarily translate into an imminent crash. However, public sentiment can influence market behavior, as fear can lead people to delay purchases or sales, which can slow down activity.

My Two Cents

So, where do I stand on all of this? Based on the data I've seen and the analysis I've done, I agree with the experts that a major housing market crash in 2025 is unlikely. The fundamentals of the market are simply too strong. However, I also think it's important to be cautious and to keep a close eye on the key risk factors.

I believe that the combination of low inventory, continued demand from millennials, and a relatively stable economy will continue to support home prices. I do think we'll see a moderation in price growth, as higher interest rates and affordability challenges start to bite. But I don't expect to see a sudden or dramatic collapse.

Ultimately, the best advice I can give is to do your own research, talk to a qualified real estate professional, and make decisions that are right for your own individual circumstances.

In Conclusion

While the possibility of a “Housing Market Crash” always lingers in the back of our minds, the current market conditions suggest a stable outlook for 2025. Low inventory, strong demand, and a relatively healthy economy make a crash unlikely, though vigilance and awareness of localized risks are still important. As always, informed decisions are the best defense against market volatility.

“Turnkey Real Estate Investing With Norada”

Worried about what might cause the housing market to crash? Diversify smartly with income-generating rental properties in stable, high-demand markets.

Norada Real Estate helps investors like you navigate uncertainty with properties built for long-term cash flow and appreciation.

HOT NEW LISTINGS JUST ADDED!

Call our investment counselors today (No Obligation):

(800) 611-3060

Recommended Read:

- What Would Cause Housing Market to Crash Again?

- Housing Market Crash: Expert Says Market is Ready to Pop

- Will the Next HOUSING CRASH Be WORSE Than 2008?

- Is the Housing Market on the Brink: Crash or Boom?

- Will the Housing Market Crash in 2025?

- 10 Most Vulnerable Housing Markets: Crash or Correction?

- United States Housing Bubble: Are We Headed for Another Crash?

- Housing Market Crash 2008 Explained: Causes and Effects

- 2024 Housing Market vs. 2008 Crash: Key Differences