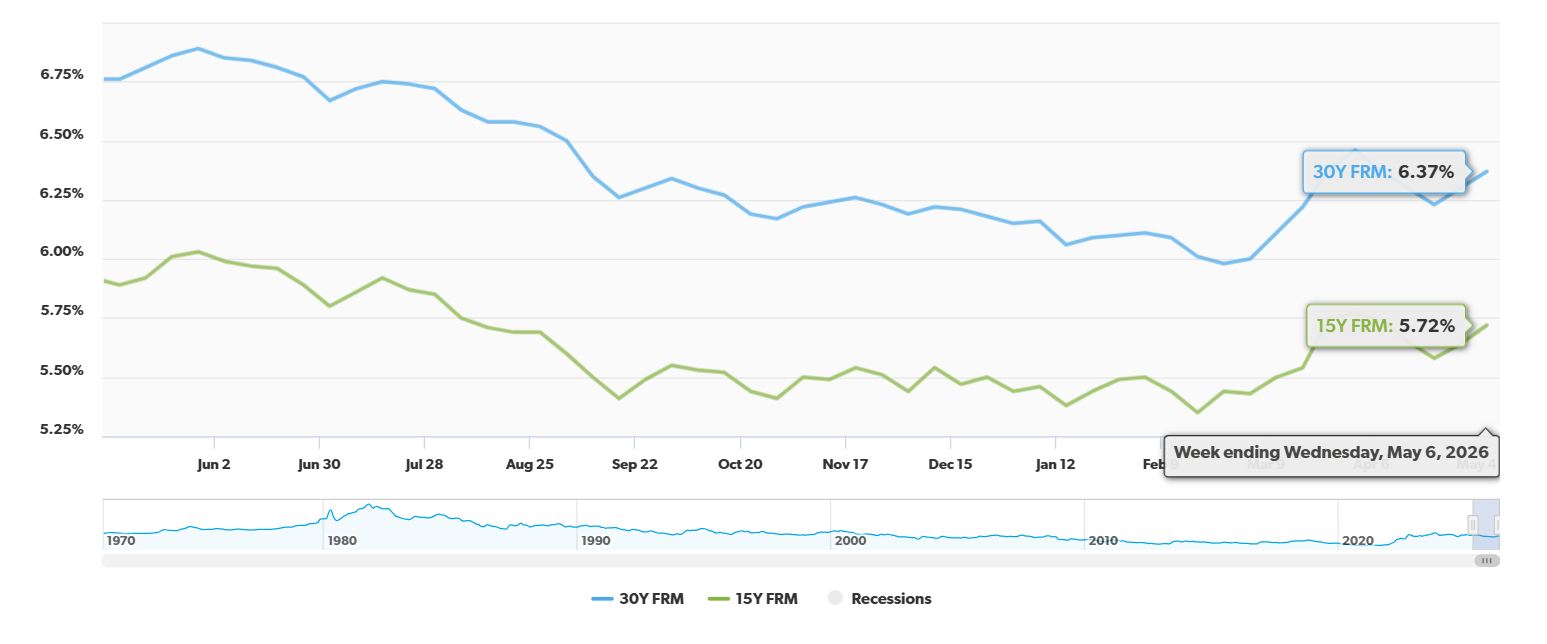

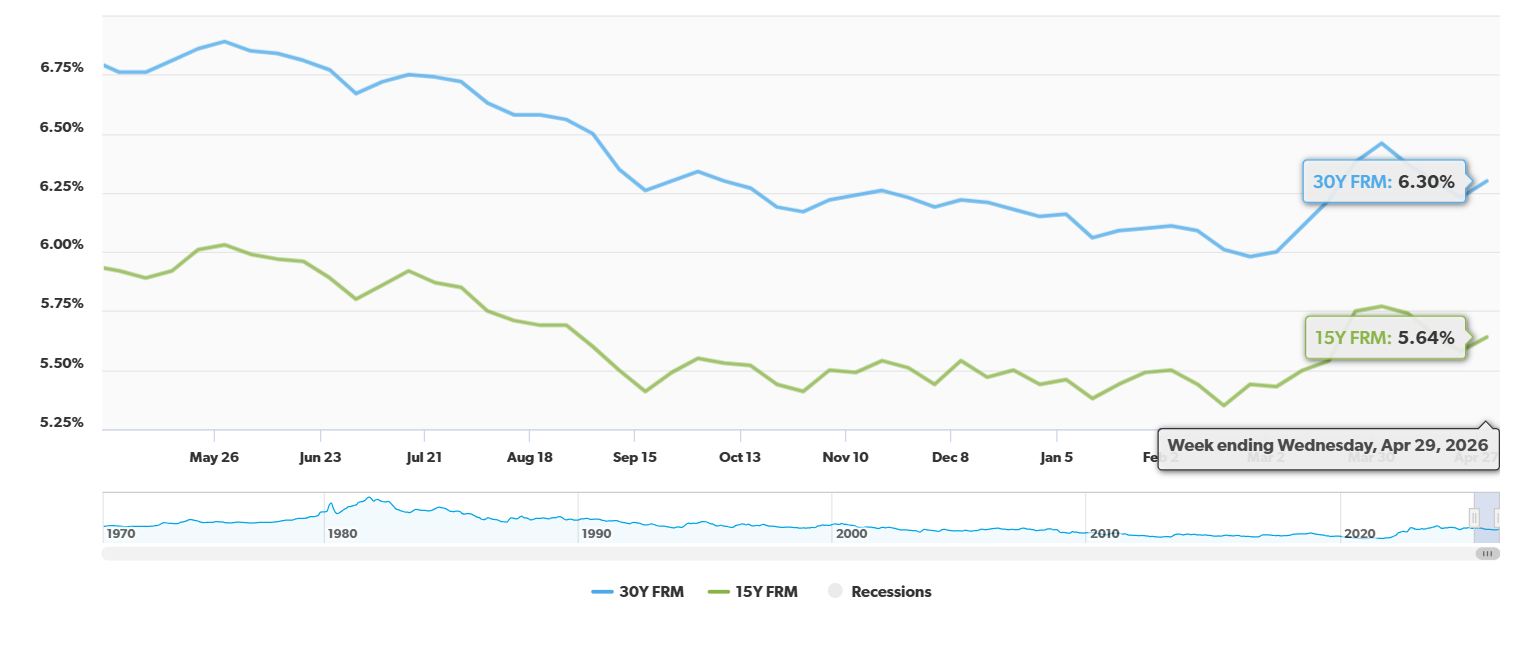

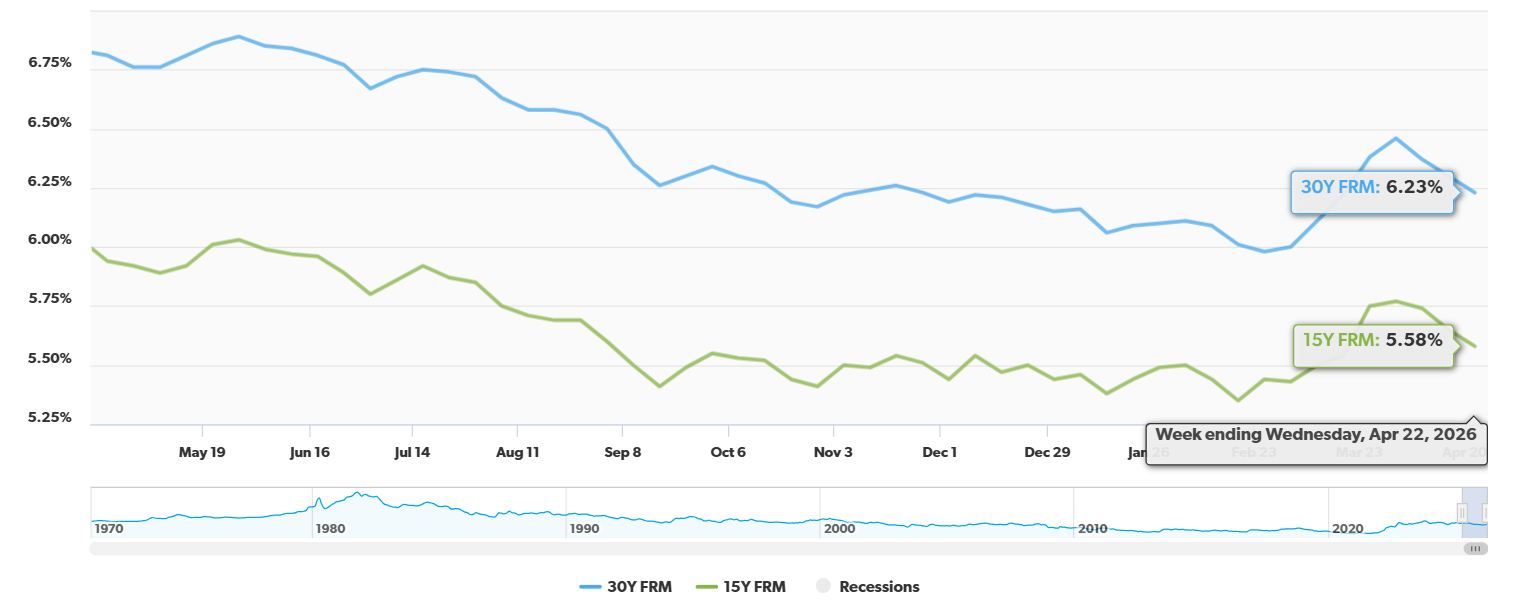

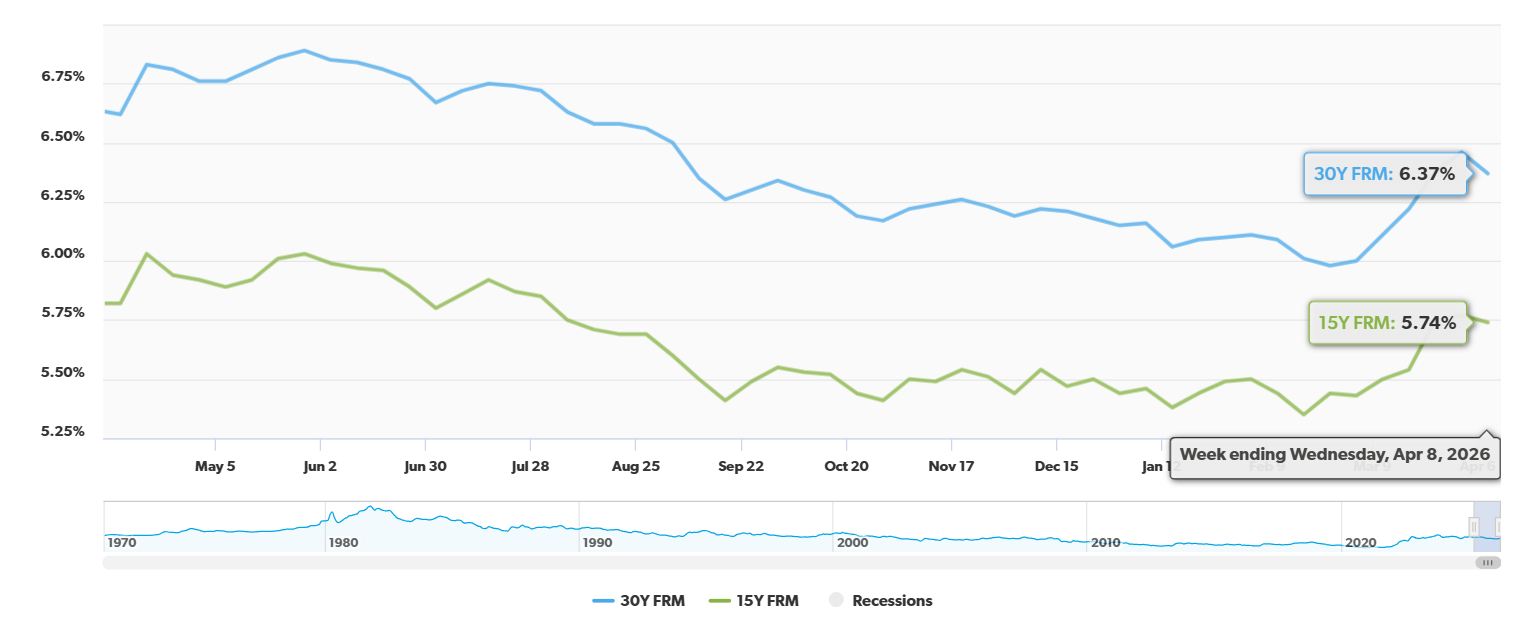

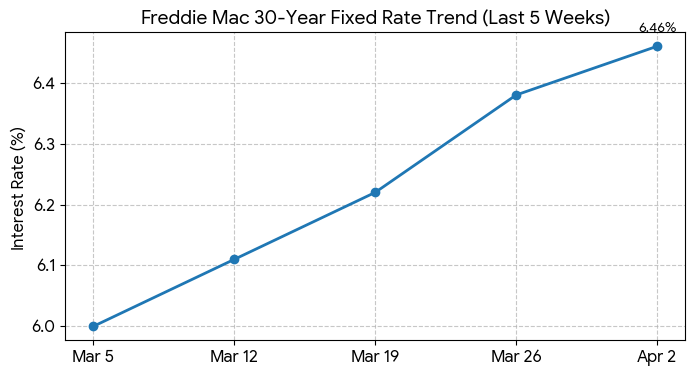

Trying to make sense of the housing market in 2026 can feel a bit like guesswork—especially when it comes to those all‑important 30‑year mortgage rates. Will they finally dip into a more comfortable range, or are we looking at another year of borrowing costs hovering stubbornly high? Based on the latest insights from major housing authorities and my own read on the economic currents, it appears that 30-year mortgage rates are likely to stay in the 5.5% to 6.5% range through the end of 2026. While some had hoped for lower figures, the economic climate suggests we'll be dealing with borrowing costs that are “higher for longer.”

30-Year Mortgage Rate Predictions for 2026

It’s easy to feel a bit lost when trying to predict mortgage rates, as so many factors are at play. From the Federal Reserve’s decisions to global events, it’s a complex dance. Here’s my breakdown of what’s really driving these numbers and why we're not seeing a sharp drop anytime soon.

The Fed's Tight Grip: Inflation and Interest Rates

The Federal Reserve's primary mission is to keep inflation in check. Lately, that inflation has been a bit more persistent than anyone would like. When the Consumer Price Index (CPI) stays elevated, the Fed tends to keep its benchmark interest rate – the federal funds rate – higher. Think of it like this: if the cost of goods and services is still climbing, the Fed is hesitant to make borrowing money cheaper, as that could further fuel spending and inflation. This “higher for longer” stance directly impacts bond yields, including those that mortgage rates are closely tied to, like the 10-year Treasury yield. I’ve seen this play out many times in my career; the Fed is usually more cautious than optimistic when inflation is stubborn.

Global Puzzles and Their Impact

We can't ignore what's happening on the world stage. Geopolitical tensions, particularly in regions like the Middle East, have a ripple effect on global oil prices. When oil prices climb, so does the cost of energy, which in turn contributes to overall inflation. This global uncertainty adds a “geopolitical premium” to things like mortgage rates and Treasury yields. It’s an extra layer of cost that lenders factor in because of the unpredictable nature of these events. It's a constant reminder that our local housing market is connected to a much larger, global economy.

The Secondary Market: A Wider Gap

Another critical piece of the puzzle is the secondary mortgage market. This is where loans are bought and sold. The spread – the difference in yield – between the 10-year Treasury and Mortgage-Backed Securities (MBS) has been wider than usual. This widening spread means lenders have to charge more for mortgages to maintain their profitability. It's an institutional factor, but it directly translates into higher rates for us as borrowers.

Expert Forecasts: What the Pros Are Saying

It’s always helpful to see what the major players in the housing industry are predicting. While early optimism for significant rate drops has softened, these revised forecasts offer a clearer picture of what to expect.

Here’s a look at some of the key predictions for late 2026:

| Forecaster | Predicted 2026 Range / Year-End Target | Key Driver / Outlook |

|---|---|---|

| Fannie Mae | 6.1% to 6.3% | Expects rates to remain sticky, averaging 6.1% late 2026-2027. |

| Mortgage Bankers Association (MBA) | 6.1% to 6.5% | Cites elevated 10-year Treasury yields and potential Fed hikes. |

| Morgan Stanley | 5.5% to 5.75% | Predicts a mid-year low followed by a moderate rebound. |

| National Association of Realtors (NAR) | 5.9% to 6.5% | Forecasts general stabilization within a narrow range. |

As you can see, there’s a consensus that rates will likely stay within a certain band, with most predicting figures above 6%. Morgan Stanley offers a slightly more optimistic outlook, suggesting a potential dip mid-year, but even they see a rebound. This consistency across different organizations gives me more confidence in the 5.5% to 6.5% range as a realistic expectation for 30-year mortgage rates in 2026.

My Take: Beyond the Numbers – Actionable Strategies

While watching economic forecasts is important, I believe the best approach for homebuyers and homeowners isn't to try and perfectly time the market – that’s a fool’s errand in my opinion. Instead, we need to focus on strategies that can help us secure the best possible rate now, regardless of minor fluctuations.

Leverage Seller-Paid Buydowns

This is a tactic I often advise clients to explore, especially in a market where sellers might be looking for an edge. A seller-paid buydown, like a 2-1 or 3-1 temporary rate buydown, can significantly lower your interest rate for the first few years of your mortgage. For example, a 2-1 buydown means your rate is 2% lower in the first year and 1% lower in the second year. This can make a substantial difference in your monthly payments during those crucial early years of homeownership. It's a win-win: the seller gets their home sold, and you get a more affordable start.

Polish Your Financial Profile

Your personal financial health plays a huge role in the rate you’ll be offered. While the Fed might move rates by a quarter-point, a significant improvement in your credit score can often yield a much larger personal benefit. If you’re planning to buy or refinance, spending time cleaning up your credit report, paying down debt, and ensuring a solid credit history can put you in a much stronger position. Moving from a “good” credit score to an “excellent” one can genuinely save you more money than waiting for a hypothetical rate drop. I’ve seen clients shave off half a percentage point or more just by improving their credit profile.

Shop Around, Especially with Credit Unions and Brokers

Don't just walk into the first big bank you see. Large financial institutions often have higher overhead and may apply stricter overlays on their rates. I highly recommend getting pre-approvals from multiple sources. Credit unions are often non-profit and can offer more competitive rates. Wholesale mortgage brokers also have access to a wider network of lenders and can often find better deals than you might find on your own. Comparing at least three to five quotes is essential. It's not about being difficult; it's about being smart with your money.

Conclusion: Preparedness is Key

The outlook for 30-year mortgage rates in 2026 suggests a period of relative stability within a higher range, likely between 5.5% and 6.5%. While economic conditions can always shift, the current trends point towards continued caution from the Federal Reserve and persistent inflationary pressures. Instead of waiting for the perfect moment, I encourage you to focus on what you can control: improving your financial standing, exploring creative financing options like seller buydowns, and diligently comparing offers from various lenders. By being prepared and proactive, you can still achieve your homeownership goals, even in this higher-rate environment.

VS

Out‑of‑State real estate investors can weigh Alabama’s newer rental with solid cap rate against Tennessee’s established A‑rated property with stability. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain near 6%, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Will Mortgage Rates Drop to 5% in 2026: Expert Forecast

- How to Get a 3% Mortgage Rate in 2026 With Assumable Mortgages?

- How to Get a 4% Interest Rate on a Mortgage in 2026?

- What Leading Housing Experts Predict for Mortgage Rates in 2026

- Mortgage Rate Predictions for 2026: What Leading Forecasters Expect

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?