Florida. The name conjures images of sunshine, beaches, and maybe even a theme park or two. For years, it's been a magnet for retirees, families, and young professionals seeking a vibrant lifestyle and, historically, relatively affordable living. But lately, that picture-perfect image is getting blurry for many residents. The reality on the ground is stark: the Florida housing market is in crisis, squeezed by skyrocketing costs, crippling insurance premiums, and a growing sense of unease among homeowners and potential buyers alike. It's a complex storm, and many Floridians are struggling to stay afloat.

What I'm seeing now feels different. It's not just a typical market correction; it's a multi-faceted pressure cooker hitting everyday people hard, especially middle-class families just trying to achieve or maintain the dream of homeownership.

Tax Relief Proposed as Florida Housing Market Faces Deepening Crisis

The Affordability Squeeze: More Than Just High Prices

Let's be real: housing prices everywhere have felt inflated lately. But Florida's situation has some unique, painful twists.

- Skyrocketing Home Values: While prices might be cooling slightly now compared to the frenzy of the past couple of years, they are still significantly higher than they were pre-pandemic. Look at major metro areas:

- Miami's median list price sits around $512,000.

- Jacksonville, while lower, is still hefty at $399,000. For many working families, these numbers are simply out of reach, especially when wages haven't kept pace.

- The Insurance Nightmare: This is arguably the biggest monster under the bed for Florida homeowners right now. Insurance costs have exploded. We're talking about premiums doubling, tripling, or even quadrupling in just a few years. Some homeowners are seeing their annual insurance bills jump by thousands of dollars overnight.

- Why? A combination of factors is at play:

- Increased Hurricane Risk: More frequent and intense storms mean higher potential payouts for insurers.

- Litigation: Florida has historically had a high rate of property insurance lawsuits, driving up costs for everyone.

- Reinsurance Costs: The cost for insurance companies to insure themselves has gone up globally, and they pass that cost on. This isn't just an inconvenience; it's making homeownership untenable for some. I know people who are seriously considering selling just because they can no longer afford the insurance, even if their mortgage payment itself is manageable. It also spooks potential buyers, adding another layer of hesitation to the market.

- Why? A combination of factors is at play:

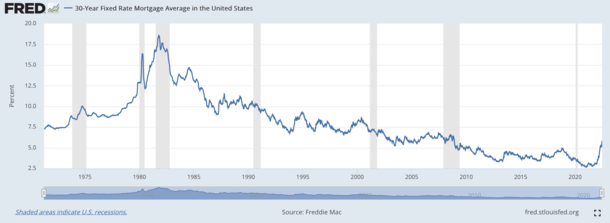

- Rising Interest Rates: While a national issue, higher mortgage rates compound Florida's affordability problem. A rate increase that might be manageable elsewhere feels crushing when layered on top of already high prices and insane insurance costs.

Market Slowdown: The Numbers Don't Lie

The heat is definitely coming off the market, but it's less of a gentle cool-down and more of a response to the intense cost pressures.

- Sales Taking a Hit: Look at the data from Realtor.com® for March:

- Pending home sales (homes under contract but not yet closed) dropped -15.1% year-over-year in Jacksonville.

- Miami saw a similar drop of -13.7%. Homes are sitting on the market longer. The bidding wars are largely gone.

- Out-of-State Interest Waning: Remember when everyone seemed to be moving to Florida? That's changing. Realtor.com® Senior Economist Joel Berner noted that “home shopping for properties in Florida by shoppers outside the Sunshine State has dwindled.” Why? Affordability. Florida's reputation as a cheaper alternative is fading fast.

From my perspective, this slowdown isn't necessarily a “crash” in the traditional sense, but rather a market straining under the weight of unsustainable costs. Buyers are hitting a wall, and sellers are having to adjust their expectations.

The Condo Conundrum: A Crisis Within a Crisis

Condominiums have long been a popular and often more affordable entry point into Florida homeownership, especially for retirees and first-time buyers. But the condo market is facing its own specific set of challenges, creating intense anxiety for owners.

- The Surfside Effect and New Regulations: The tragic collapse of the Champlain Towers South in Surfside in June 2021 sent shockwaves through the state and led to much-needed safety legislation. The law now mandates:

- “Milestone Inspections” for condo buildings three stories or higher and over 30 years old (25 years near the coast).

- Mandatory Reserve Funds: Condo associations can no longer waive collecting funds for essential future repairs (like roofs, structural elements, etc.). They must have enough money set aside to perform necessary maintenance identified in structural integrity reserve studies.

- The Financial Fallout: While crucial for safety, these regulations have created a perfect storm of financial pressure for condo owners:

- Special Assessments: Many associations, discovering the true cost of needed repairs through inspections, are levying huge special assessments on owners – sometimes tens of thousands of dollars per unit, payable over a short period.

- Skyrocketing HOA Fees: To build up those mandatory reserves, regular monthly Homeowner Association (HOA) fees are climbing dramatically.

- Insurance Hikes (Again): Condo buildings are facing the same massive insurance premium increases as single-family homes, costs which are passed directly to owners via HOA fees.

I've heard heartbreaking stories from condo owners, particularly seniors on fixed incomes, who are terrified of losing their homes. They're facing fee increases that exceed their monthly mortgage payments. One state lawmaker even warned this condo fee crisis “could trigger the next wave of homeless people.” That's not hyperbole; it's a reflection of the desperation some residents feel. Many are forced to sell, sometimes at a loss, just to escape the mounting costs.

Looking for Solutions: Can Tax Relief Help?

Amidst this crisis, lawmakers are exploring ways to provide some relief. One prominent effort comes from Florida Congressman Vern Buchanan.

- The Middle Class Mortgage Insurance Premium Act: Rep. Buchanan is pushing to bring back and make permanent a tax deduction for mortgage insurance premiums.

- What is Mortgage Insurance? Typically required if you buy a home with less than a 20% down payment. It protects the lender, not the borrower.

- The Old Deduction: This deduction existed from 2007 to 2021 but expired.

- The Proposal: Restore the deduction permanently and increase the income limit for eligibility from $100,000 to $200,000 per family.

- The Goal: As Buchanan stated, “provide tax relief for middle-class families seeking to own a home.” According to an Urban Institute study, over 361,000 Florida homebuyers needed mortgage insurance back in 2020 alone. This could put a little bit of money back into the pockets of those struggling with affordability, particularly first-time buyers who often can't scrape together a 20% down payment.

- My Take on This: Offering tax relief is certainly a welcome gesture. Every little bit helps, especially for families on the edge. Restoring the mortgage insurance deduction could ease the burden slightly for a specific group of homeowners. However, in my opinion, while helpful, this feels more like treating a symptom than curing the disease. It doesn't directly address the core drivers of the crisis: the astronomical cost of property insurance and the fundamental lack of affordable housing supply relative to demand. It helps people after they've managed to buy, but the biggest hurdle for many is getting into a home in the first place.

Helping Builders, Helping Supply? Another Legislative Angle

Rep. Buchanan is also involved in another legislative effort aimed at the supply side of the equation, specifically for condos:

- The Fair Accounting for Condominiums Act: This bill tackles a specific tax issue faced by condo developers.

- The Problem: Currently, developers often have to pay income taxes on buyer deposits received during construction, even though they don't get the full purchase price (and profit) until the unit actually closes, sometimes years later. This creates a cash-flow strain.

- The Proposal: Exempt high-rise condo projects under construction from this immediate tax burden on deposits, aligning their tax treatment more closely with single-family home builders.

- The Goal: Make it financially easier for developers to build multi-unit condos, thereby potentially increasing the housing supply. Buchanan argues this could help those “most impacted by the nationwide housing crisis.”

- My Thoughts: Addressing hurdles for developers could eventually help with supply, which is a critical piece of the puzzle. More supply generally leads to more stable (or even lower) prices over the long term. However, this is a long-term play. It doesn't provide immediate relief to homeowners struggling today. Furthermore, we need to ensure that any new development includes a significant component of truly affordable housing, not just luxury condos that cater to the higher end of the market. Boosting overall supply is good, but targeted efforts for workforce and middle-income housing are desperately needed.

Where Do We Go From Here? The Path Forward is Murky

So, yes, the Florida housing market is in crisis. It's a complex web of high prices, crippling insurance costs, post-Surfside condo regulations leading to massive fee hikes, and a general affordability crunch exacerbated by interest rates.

Legislative efforts like tax deductions and accounting changes for developers might offer some marginal relief or help slightly on the supply side over time. But they don't feel like the comprehensive solution Florida needs.

What truly needs to happen, in my view?

- Tackling the Insurance Beast: This is paramount. Meaningful reform is needed to stabilize the property insurance market. This could involve tort reform, encouraging more insurers to enter the Florida market, and exploring innovative solutions to manage catastrophic risk. Without addressing insurance, homeownership will remain precarious for many.

- Boosting Affordable Housing Supply: We need more homes, period. But specifically, we need more homes targeted at middle-income and workforce families. This requires zoning reforms, incentives for developers, and potentially exploring different housing models.

- Supporting Condo Owners: Finding ways to help long-time condo residents, especially seniors on fixed incomes, manage the costs associated with the new safety regulations is crucial. This might involve state-backed low-interest loans or grants for critical repairs and reserve funding.

The Florida dream of affordable homeownership in the sun is under serious threat. While the market might be slowing down in terms of sales, the financial pressure on existing homeowners, particularly in condos, is intensifying. It's a crisis that demands more than just temporary fixes; it requires bold, comprehensive action to restore stability and affordability for the long haul.

Work with Norada, Your Trusted Source for

Real Estate Investment in “Florida Markets”

Discover high-quality, ready-to-rent properties designed to deliver consistent returns.

Contact us today to expand your real estate portfolio with confidence.

Contact our investment counselors (No Obligation):

(800) 611-3060

Read More:

- Is the Florida Housing Market on the Verge of Collapse or a Crash?

- 3 Florida Cities at High Risk of a Housing Market Crash or Decline

- 4 States Facing the Major Housing Market Crash or Correction

- Florida Housing Market: Record Supply Expected to Favor Buyers in 2025

- Florida Housing Market Forecast for Next 2 Years: 2025-2026

- Florida Real Estate Market Saw a Post-Hurricane Rebound Last Month

- Florida Housing Market: Predictions for Next 5 Years (2025-2030)

- Hottest Florida Housing Markets in 2025: Miami and Orlando

- Florida Real Estate: 9 Housing Markets Predicted to Rise in 2025

- Housing Markets at Risk: California, New Jersey, Illinois, Florida

- 3 Florida Housing Markets Are Again on the Brink of a Crash

- Florida Housing Market Predictions 2025: Insights Across All Cities

- Florida Housing Market Trends: Rent Growth Falls Behind Nation

- When Will the Housing Market Crash in Florida?

- South Florida Housing Market: Will it Crash?

- South Florida Housing Market: A Crossroads for Homebuyers