If you've been watching the housing market with a bit of worry, wondering when things might become more manageable for buyers, I have some good news. Based on the latest 2026 National Housing Forecast from Realtor.com®, several housing markets are expected to see their home price growth slow down considerably – or even dip – by 2026. This presents a significant opportunity for those looking to purchase a home.

10 Housing Markets Predicted to See Rapid Price Decline in 2026

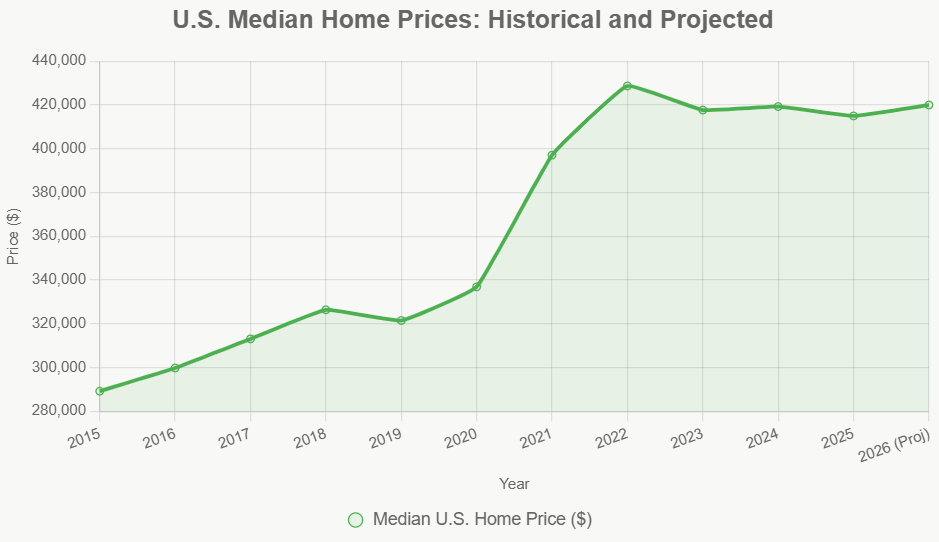

For most of us, housing is the biggest purchase we'll ever make. It’s not just about a roof over our heads; it’s about building equity, creating a stable environment, and making an investment in our future. The wild ride of the past few years, with prices soaring at breakneck speed, has made that dream feel out of reach for many. But as we look ahead to 2026, a shift is on the horizon.

Nationally, Realtor.com® predicts a modest price increase of 2.2% year-over-year. While this is still growth, it’s a far cry from the double-digit leaps we’ve become accustomed to. What’s even more interesting is that this national picture masks some dramatic regional differences. In fact, nearly a quarter of the top 100 housing markets are expected to see actual price declines in 2026. This is where the real story lies for potential homebuyers.

Where the Price Slowdown is Hitting Hardest

It's not just a little cooling; some areas are looking at a significant shift. According to Realtor.com®'s forecast, the metros expected to experience the steepest drops in home price growth are largely clustered in coastal states. Florida takes a commanding lead with four metros in the top 10, while California follows with three. We're also seeing projections for softening prices in Raleigh, North Carolina, Spokane, Washington, and Denver, Colorado.

The Top Metros to See Price Growth Cool Fastest in 2026:

| Metro | 2026 Price Growth % YoY |

|---|---|

| Cape Coral, FL | -10.2% |

| North Port, FL | -8.9% |

| Stockton, CA | -4.1% |

| Raleigh, NC | -3.7% |

| Deltona, FL | -3.6% |

| Tampa, FL | -3.6% |

| Spokane, WA | -3.5% |

| Denver, CO | -3.4% |

| Sacramento, CA | -3.3% |

| San Francisco, CA | -2.5% |

Source: Realtor.com® 2026 National Housing Forecast

You'll notice Cape Coral, Florida, stands out with a projected double-digit price growth plunge of 10.2% year-over-year. This isn't a complete surprise if you've been following real estate trends. A recent report from analytics firm Cotality already highlighted Cape Coral as having the largest annual home price decline in Florida and the second-largest nationwide back in September, dropping 7.1%.

North Port, Florida, another market flagged by Cotality for cooling, is anticipated to see the nation's second-biggest decrease in price growth at 8.9%.

Why the Cooling? A Closer Look at Florida

It seems Florida is ground zero for this market correction. Realtor.com®'s senior economic research analyst, Hannah Jones, points out that these metros have already seen prices slip from their pandemic highs. She notes that elevated home prices, coupled with rising insurance premiums and other carrying costs, are weighing down buyer demand.

In fact, Realtor.com® data shows that statewide median listing prices in Florida were down 6% in the first half of 2025 compared to the same period in 2023. A big part of this dip is due to plummeting condo prices. This is largely a result of new safety legislation passed after the Surfside tragedy, which mandated more funding for building maintenance and inspections. This has led to significant increases in homeowner association (HOA) special assessment fees, making condo ownership much more expensive.

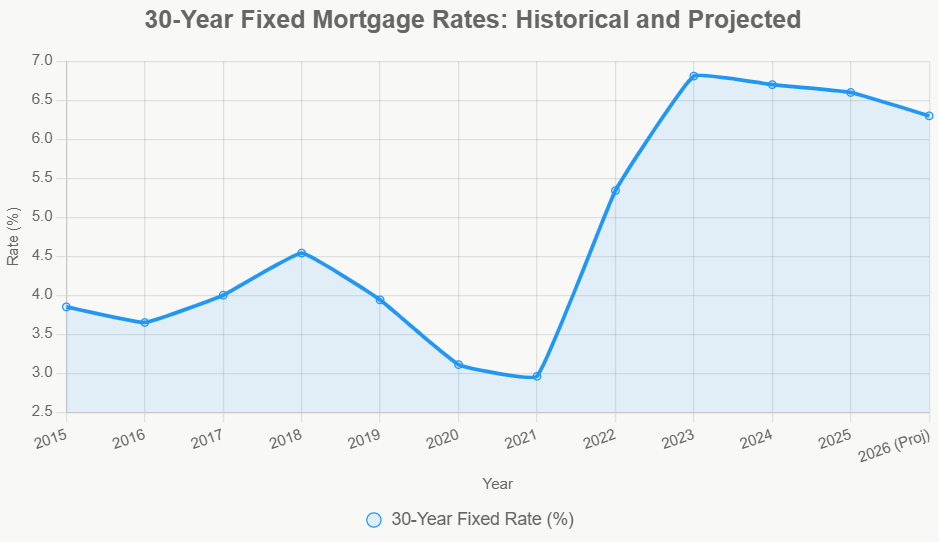

Jones also explains that Florida experienced a massive influx of new residents during the pandemic, fueled by remote work opportunities. This surge in demand helped drive prices sky-high. However, now we're seeing a correction. Rising mortgage rates, the aforementioned insurance costs, and climate-related risks are making buyers more cautious. This caution is pushing some owners to list their homes, increasing supply and consequently easing price pressures.

Karen Borelli, president of the Royal Palm Coast Realtor® Association, echoes this sentiment for Cape Coral. She mentions that home prices there have already dropped by 5% to 10% in recent years. The forecast for further price growth declines in 2026 doesn't surprise her. She explained that during the COVID-19 pandemic, demand from people seeking sunshine pushed prices up by a staggering 65% to 70%. After Hurricane Ian, the market shifted, with more homes becoming available and sales slowing down. Like the rest of Florida, escalating insurance costs and elevated mortgage rates are making homeownership less affordable.

However, Borelli offers a hopeful note for buyers in Cape Coral. She anticipates that in 2026, buyers will find a larger selection of homes and potentially reduced prices, along with builder and seller incentives. She emphasizes that real estate markets move in cycles, and while demand pushes prices up, a shift in inventory and demand can lead to more balanced conditions.

It's also worth noting that Florida Governor Ron DeSantis has been pushing for the elimination of property taxes on owner-occupied homes. Borelli suggests that if this policy is enacted, it could significantly impact home values, potentially leading to a rapid increase.

Beyond the Sunshine State: Western Markets See a Correction

While Florida is a major focal point, the cooling trend isn't confined there. Several California markets are also predicted to experience significant drops in home price growth. Stockton, in the Central Valley, is projected to see a 4.1% dip in 2026, making it the largest decrease in California and the third-largest nationwide.

Other major California cities like Sacramento (projected 3.3% decrease) and the famously expensive San Francisco (projected 2.5% decrease) are also expected to see their appreciation rates slow down.

Hannah Jones from Realtor.com® explains that these Western metros are adjusting after years of rapid price gains. Just like in the South, stretched affordability is a key driver. High prices and the persistent drag of high mortgage rates are eating into buyer demand, leading to potential price softening.

In Denver, Colorado, the growth rate is expected to decrease by 3.4% next year. Heather O'Leary, a real estate agent at eXp Realtor, attributes this partly to an increase in multifamily housing within the metro area. These types of properties typically have lower price points, which can pull down the median home price even if overall values remain relatively stable.

O'Leary also points out that for many low-income households in Denver, renting is currently more affordable than buying. This dynamic reduces demand for entry-level homes and contributes to declining median prices. Shifting migration patterns, with people moving from Denver's urban core to surrounding counties for more space and newer homes, also play a role. This outward movement redistributes demand and can slightly cool prices in the core city.

Despite the projected 3.4% pullback in Denver, O'Leary views it as a normalization rather than a collapse. She highlights Denver's current 3.6-month supply of inventory, which signals a move towards a more balanced market. For buyers, this cooling trend, combined with higher inventory, could mean more choices and a stronger position to negotiate. O'Leary notes that even a slight easing of interest rates could significantly boost a buyer's purchasing power.

For sellers, the key in these markets will be strategic pricing from the outset. Listing too high could lead to homes sitting on the market longer and requiring deeper price cuts later on.

What This Means for You: Buyers Find Leverage, Sellers Need Realism

The takeaway from all this data, sourced from Realtor.com®, is that 2026 is shaping up to be a more favorable year for homebuyers in certain regions. As Hannah Jones puts it, “For buyers, these cooling markets offer more leverage: greater negotiating power, more inventory to choose from, and more sellers willing to offer concessions.”

This cooling doesn't necessarily mean a housing market crash. Instead, it signifies a return to a more sustainable pace after a period of unsustainable growth. For those who have been priced out or struggling to compete in bidding wars, this could be the moment to re-enter the market with more confidence.

For sellers, it’s crucial to be realistic. The days of expecting multiple offers far above asking price might be over in these specific markets. Understanding current market conditions, pricing your home competitively, and being open to negotiation will be key to a successful sale.

The housing market is always evolving, and understanding these projected shifts is vital for anyone looking to buy or sell in the coming years. By paying attention to forecasts like Realtor.com®'s, we can make more informed decisions and navigate the real estate journey with greater clarity.

2026 Housing Market Forecast for Investors

Most experts forecast steady but modest price growth, shifting affordability, and evolving rental demand in 2026—creating unique opportunities for each group.

Rising demand keeps rental markets competitive, but turnkey investors benefit from strong cash flow.

Norada Real Estate helps you navigate these shifts with fully managed rental properties—so whether you’re buying, selling, or renting, you can position yourself for success in 2026.

🔥 HOT NEW Investor Deals JUST ADDED! 🔥

Talk to a Norada investment counselor today (No Obligation):

(800) 611-3060

Want to Know More About the Housing Market Trends?

Explore these related articles for even more insights:

- Housing Market Predictions for 2026 Show a Modest Price Rise of 1.2%

- Housing Market Predictions 2026 for Buyers, Sellers, and Renters

- Why Are Home Prices Dropping in Over Half of Major US Cities in 2025?

- Redfin's Bold Predictions About The Great Housing Market Reset in 2026

- 5 Most Expensive Housing Markets Are Now Seeing the Biggest Price Cuts

- Housing Market Predicted to See Strong Growth in 2026: Expert Forecast

- Housing Market Predictions for the Next 12 Months by Zillow

- Housing Market Regains Ground as Falling Mortgage Rates Unlock Buyer Savings

- Hidden Costs of Homeownership Now Add Up to Nearly $16,000 a Year

- Small Investors Dominate the Housing Market From Detroit to Vegas

- Housing Market Predictions for the Next 4 Years: 2025 to 2029

- Housing Market 2025 Splits Between Wealthy Buyers and First-Timers

- Housing Markets at Risk of Double-Digit Price Decline Over the Next 12 Months

- Will the Housing Market Shift to a Buyer’s Market in 2026?

- Mid-Atlantic Housing Market Heats Up as Mortgage Rates Go Down