Imagine a retirement where your mail brings you “automatic monthly rent checks” instead of bills, where financial worries fade as predictable income flows in, allowing you to truly enjoy your golden years. This isn't a pipe dream; it's the tangible reality Norada Real Estate Investments helps thousands achieve by enabling them to “rent to retire.” By providing ready-to-go, income-generating rental properties that are professionally managed, Norada empowers individuals to build a portfolio that replaces their working salary with passive income, making retirement not just possible but truly fulfilling and financially secure.

Norada Real Estate Investments: Rent to Retire Model for Sustainable Passive Income

For years, I've seen countless people struggle with traditional retirement planning. The stock market can feel like a rollercoaster, and bank savings often don't keep up with inflation. It leaves many wondering if they'll ever truly be able to stop working without compromising their lifestyle. That's why the concept of “rent to retire” has always fascinated me, and frankly, why I believe it's one of the most powerful and underutilized strategies out there. It’s about leveraging real assets to build real freedom.

Why “Rent to Retire” is a Game Changer for Your Golden Years

The idea is elegantly simple: instead of just saving money, you acquire assets that generate money for you. Think about it. Your current salary covers your living expenses, right? The “rent to retire” strategy aims to build a portfolio of rental properties whose collective income matches or exceeds those expenses. This way, when you decide to hang up your professional hat, your essential needs and desires are covered by cash flow that doesn't rely on your active labor.

From my perspective, this isn't just about money; it’s about control. It offers a sense of security that traditional approaches often lack. With real estate, you're investing in something tangible, something that people will always need: a place to live. And that need translates into consistent demand and, more importantly, consistent income. This strategy is precisely what Norada Real Estate Investments has perfected, carving a path for everyday people to become successful real estate investors without becoming full-time landlords.

How Norada Real Estate Investments Powers Your Retirement Journey

Norada Real Estate Investments, established in 2003, is a national real estate firm that has been at the forefront of making passive income accessible. From my years of observing the real estate market, what sets us apart isn't just our experience, but our focused approach on what I call the “sleep-easy investment.” We understand that most people want the benefits of real estate without the headaches.

The “Turnkey” Advantage: Passive Income, Zero Headaches

The heart of Norada’s offering revolves around turnkey rental properties. What does “turnkey” really mean? In simple terms, it means “ready to go.” Imagine buying a house that's already renovated to high standards, has a tenant already living in it, and has professional property management lined up. You literally just turn the key (or in this digital age, get the financials) and start earning income. You don't have to worry about finding contractors, choosing paint colors, or chasing down rent checks.

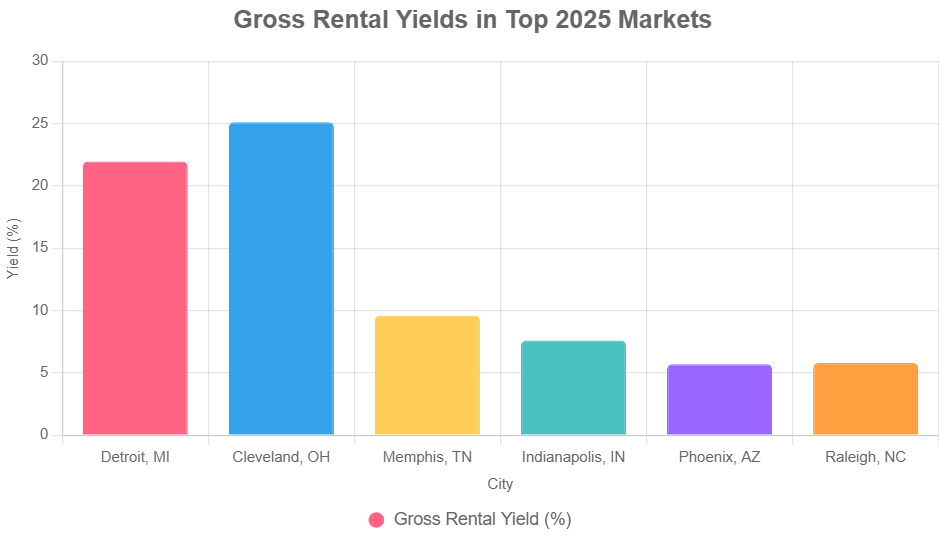

Norada specializes in identifying growth markets across the United States. We don't just pick properties at random; they're strategic. We focus on places like Dallas, Kansas City, Birmingham, and Indianapolis – areas known for strong job growth, increasing populations, and affordable housing. This deliberate choice reduces investment risk and increases the potential for both cash flow and property appreciation. We even provide a “DealGrader” score for each property, which, in my experience, is a fantastic tool for evaluating the quality and potential risks of an investment at a glance. It’s like having a seasoned investor's analysis right at your fingertips.

From single-family homes to fourplexes, Norada offers a variety of property types designed to suit different investment goals. This level of vetting and preparation is absolutely critical, especially for new investors or those who are time-poor. The last thing you want when aiming for a peaceful retirement is to buy a “fixer-upper” that becomes a money pit and a never-ending project. Norada understands this implicit need for ease and reliability.

From Goal Setting to Growing Your Portfolio

The journey to building a “rent to retire” portfolio with Norada is remarkably structured and straightforward:

- Define Income Goals: The first, and most crucial, step is setting a clear target. How much monthly rental income do you need to cover your desired retirement lifestyle? Are you aiming for $3,000 to $5,000 per month, or perhaps more? Norada helps you quantify this goal, which then dictates the size and scope of your investment portfolio. I’ve found that many people skip this step, but it’s like setting off on a journey without knowing your destination.

- Select a Turnkey Provider: This is where Norada shines. We handle the hard work: finding the right properties, overseeing high-quality renovations, and placing reliable tenants. Our comprehensive service takes the guesswork and grunt work out of investing.

- Secure Financing: Most investors use leverage (mortgages) to purchase properties. You typically put down 20-25%, allowing you to control a much larger asset with less capital. This is a powerful wealth-building tool that I often advise clients to consider, as it significantly amplifies your returns.

- Acquire and Scale: The beauty of this strategy is its scalability. You can start with one property, then as it generates income, you can reinvest profits to acquire another, and another, until your total cash flow meets your retirement target. It’s a snowball effect that builds momentum over time.

- Passive Management: This is where the true “retirement” aspect comes into play. Third-party property managers handle all the day-to-day operations – from rent collection to maintenance requests. Your role effectively becomes checking your bank account for those “automatic monthly rent checks.” This “hands-off experience” is particularly appealing to retirees who want to enjoy life, not deal with clogged toilets.

Unpacking the Benefits: Why Norada's Approach Makes Sense

Let's break down the distinct advantages that make Norada’s “rent to retire” strategy so compelling:

Immediate Cash Flow: No Waiting, Just Earning

Unlike buying a property that needs extensive repairs or sitting vacant, Norada's turnkey properties are often sold already tenanted. This means your income stream starts flowing from day one. There’s no waiting period, no missed rent, just immediate returns on your investment. In my view, this immediate cash flow is a huge stress reliever for investors, offering tangible proof that the strategy works.

Inflation Protection: Your Money Works Harder

One of the sneakiest threats to retirement savings is inflation, silently eroding your purchasing power. However, with rental properties, landlords can increase rents over time. Historically, rental income tends to keep pace with, or even exceed, inflation. This built-in adjustment mechanism acts as a natural hedge, protecting your financial future. Especially in today's economic climate, where inflation feels like a constant companion, this protective element of real estate is more valuable than ever.

Geographic Flexibility: Smart Investments, Anywhere

You don't have to invest in your own backyard, especially if your local market has high prices and low returns. Norada encourages investing in high-growth, affordable markets out-of-state, such as Indianapolis, Memphis, or Birmingham, where the Return on Investment (ROI) can be significantly higher. This flexibility allows you to chase the best deals nationwide, rather than being confined by your local ZIP code. I've seen too many people miss out on great opportunities because they were afraid to invest outside their city. Norada takes away that fear by doing the local market vetting for you.

Tax Advantages: Keeping More of What You Earn

Real estate investments come with some fantastic tax benefits. You can depreciate the property over time, which can significantly offset your rental income for tax purposes. Additionally, expenses like property taxes, mortgage interest, and even property management fees are often deductible. It's crucial to consult a tax professional, but these advantages can dramatically improve your net cash flow and overall returns, allowing you to keep more of what you earn.

Building Trust and Long-Term Wealth with Norada

Having observed the real estate investment landscape for many years, I can confidently say that Norada Real Estate Investments stands out for its commitment to simplicity, transparency, and investor success. Our business model directly addresses the primary concerns of individuals looking to “rent to retire”: managing risk, reducing effort, and ensuring consistent income.

Our company's longevity since 2003 speaks to their expertise and stability. The fact that we prioritize tenant-occupied, professionally managed properties in carefully selected growth markets shows a deep understanding of what creates true passive income. We aren't selling dreams; we're selling a well-oiled system designed for predictable results.

For anyone seeking to replace their working income with a stream of reliable, passive cash flow through real estate – whether you're close to retirement or planning for it decades out – Norada offers a compelling and thoroughly vetted solution that truly empowers individuals to achieve financial independence and live their retirement dreams on their terms.

The 2026 housing market is shaping up with strong rental demand, steady appreciation, and opportunities in turnkey properties across top U.S. cities. Investors are finding reliable cash flow even as broader economic conditions shift.

Norada Real Estate helps investors navigate turnkey opportunities—providing immediate rental income and long‑term ROI in markets positioned for growth in 2026 and beyond.

Also Read:

- Norada Real Estate Investments: Housing Market Outlook 2026

- Housing Market Predictions by Warren Buffett's Berkshire Hathaway

- Will the Housing Market Crash in 2025: What Experts Predict?

- Housing Market Predictions 2026: Will it Crash or Boom?

- Housing Market Predictions for the Next 4 Years: 2025 to 2029

- 12 Housing Markets Set for Double-Digit Price Decline by Early 2026

- Real Estate Forecast: Will Home Prices Bottom Out in 2025?

- Real Estate Forecast Next 5 Years: Top 5 Predictions for Future

- 5 Hottest Real Estate Markets for Buyers & Investors in 2025

- Will Real Estate Rebound in 2025: Top Predictions by Experts

- Will the Housing Market Crash Due to Looming Recession in 2025?

- 4 States Facing the Major Housing Market Crash or Correction

- New Tariffs Could Trigger Housing Market Slowdown in 2025

- Real Estate Forecast Next 10 Years: Will Prices Skyrocket?