Well, it’s November 30th, and guess what? The 30-year fixed mortgage rate remains stable around 6.00%. This is the first time we’ve seen this benchmark in a while, and honestly, it brings a sigh of relief to many. It’s definitely sparking conversations about whether a dip into the 5% range might be closer than we think. While rates are always a bit of a moving target across the country, a lot of people are finally looking at the lowest mortgage rates they’ve seen in months.

Today’s Mortgage Rates, Nov 30: 30-Year Fixed Rate Poised to Break Into the 5% Range

It feels like just yesterday we were talking about rates being higher. According to the latest numbers from Zillow, the average for that popular 30-year fixed mortgage is now holding steady at a solid 6.00%. For those considering a shorter commitment, the 15-year fixed is looking good at 5.50%. To give you some perspective, just last Wednesday, Freddie Mac had reported the 30-year fixed rate averaging a higher 6.23%. This really goes to show how fast things can change in the mortgage world, and why, no matter what the numbers say, you absolutely must shop around with different lenders. It's the simplest way to make sure you're getting the best deal possible.

Current Mortgage Rates for November 30, 2025

Here’s a quick peek at the average rates as of today, according to Zillow. Remember these are national averages, so your personal rate might be a little different based on your unique situation.

| Loan Type | Average Rate |

|---|---|

| 30-year fixed | 6.00% |

| 20-year fixed | 5.86% |

| 15-year fixed | 5.50% |

| 5/1 ARM | 6.11% |

| 7/1 ARM | 6.15% |

| 30-year VA | 5.44% |

| 15-year VA | 5.10% |

| 5/1 VA | 5.11% |

Current Mortgage Refinance Rates: Are You Ready to Save?

If you’ve been thinking about refinancing your current home loan, now might be an opportune time to investigate. The rates for refinancing are a little different than buying, but still showing some attractive numbers.

| Loan Type | Average Rate |

|---|---|

| 30-year fixed | 6.14% |

| 20-year fixed | 6.05% |

| 15-year fixed | 5.60% |

| 5/1 ARM | 6.55% |

| 7/1 ARM | 6.72% |

| 30-year VA | 5.57% |

| 15-year VA | 5.18% |

| 5/1 VA | 5.04% |

👉 The Big Picture: Seeing that 6% mark again is a significant sign that the market is continuing to shift. If these rates keep inching lower, that psychological barrier of 5% could really encourage more people to jump into the market as buyers or to refinance their existing homes. The main takeaway for everyone right now is simple: compare, compare, compare! Even a fraction of a percent difference in your interest rate can add up to thousands of dollars saved over the life of your loan.

What Today’s Rates Mean for Homebuyers and Homeowners

Let's break down what this news means for you, whether you're looking to buy your first home or you're a seasoned homeowner thinking about your next move.

- For Buyers: With the 30-year fixed rate dipping back to 6.00%, affordability just got a bit better compared to last week’s 6.23%. Even a small drop like this can mean hundreds of dollars saved each month on your mortgage payment. For anyone who’s been waiting on the sidelines, watching and hoping for the right moment, this could be the signal you’ve been looking for. It's a real window of opportunity.

- For Refinancers: If you’re looking to refinance, the current averages for a 30-year fixed at 6.14% are still a tad higher than purchase rates. However, if you locked in a rate much higher than that, say at 7% or more, earlier this year or last, refinancing now could still lead to a significant reduction in your monthly payments. It’s definitely worth checking out your options.

- Market Sentiment: This easing of rates toward the 5% mark is important. If it continues, we could see buyer demand really pick up steam. This might lead to more competition in the housing market as we move into early 2026.

My Two Cents: As someone who’s followed the housing market for a while, this return to 6% feels like a much-needed stabilization. It's not the rock-bottom rates of a few years ago, but it's certainly a more manageable environment than we've seen recently. The key takeaway for buyers and refinancers is to be proactive. Don't assume your current lender is offering the best deal. Get quotes from several different lenders – online lenders, local banks, credit unions. You might be surprised by the difference.

How to Get the Best Possible Mortgage Rate

Beyond just the national averages, there are concrete steps you can take to increase your chances of snagging a lower mortgage rate. It’s not all about luck or the whims of the market; your personal financial health plays a huge role.

- Polish Your Financial Profile:

- Boost Your Credit Score: This is arguably the most impactful step. A higher credit score tells lenders you're a lower risk, and that translates directly into a lower interest rate. Most lenders offer their best rates to those with scores of 740 or higher. While some conventional loans might start accepting scores as low as 620, the rate you’ll get will be significantly higher. To improve your score, make it a habit to pay all your bills on time, keep your credit card balances as low as possible (ideally below 30% of your credit limit), and steer clear of opening new credit accounts right before you apply for a mortgage.

- Increase Your Down Payment: The more you can put down upfront, the less the lender has to finance, and the less risk they take on. A larger down payment can lead to a lower interest rate, a smaller loan amount overall, and consequently, smaller monthly payments. Plus, putting down at least 20% is crucial if you want to avoid paying for Private Mortgage Insurance (PMI), which is an added monthly cost.

- Lower Your Debt-to-Income (DTI) Ratio: Lenders absolutely scrutinize your DTI to gauge your ability to handle loan payments. The general aim is to keep your DTI at 36% or less, though some lenders might be flexible if you have substantial savings. You can tackle this by paying down existing debts (like car loans or credit cards) or by increasing your income.

- Adjust Your Loan Terms Wisely:

- Consider a Shorter Loan Term: While the 30-year fixed is incredibly popular for its lower monthly payments, a 15-year mortgage almost always comes with a lower interest rate because it’s less risky for the lender. The trade-off, of course, is that your monthly payments will be higher. You need to weigh affordability now versus potential long-term savings.

- Buy Mortgage Discount Points: This is an option you can discuss with your lender at closing. You can pay an upfront fee, typically 1% of the loan amount per point, to “buy down” your interest rate. One point can usually shave about 0.25% off your rate. The trick here is to do the math and figure out how many years it will take for the monthly savings to cover the upfront cost.

- Explore Different Mortgage Types: Don’t just default to a fixed-rate loan. Look into options like FHA loans (if you qualify), VA loans (for eligible veterans), or Adjustable-Rate Mortgages (ARMs). ARMs often have a lower initial interest rate compared to fixed-rate loans for the first few years, which can be appealing, but you need to understand how those rates will adjust later on.

Expert Forecasts and Market Factors: What's Driving Rates?

So, what’s behind these movements and what do the experts predict? It’s a complex puzzle with a few key pieces.

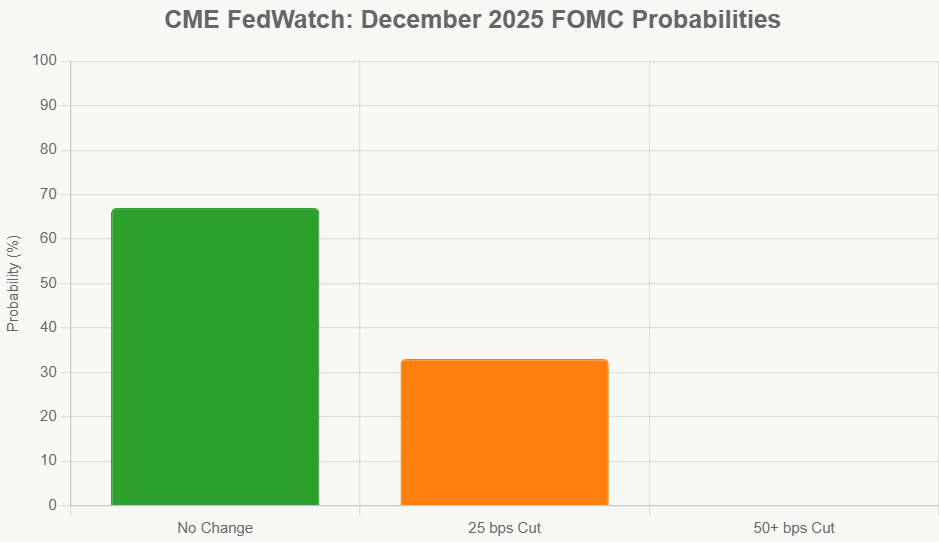

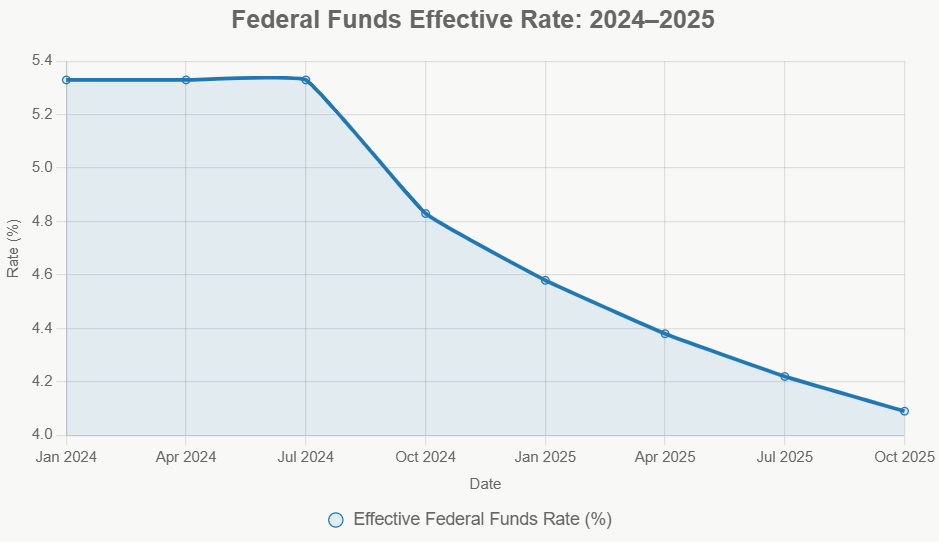

- The Federal Reserve's Role: The Fed has been making moves to influence the economy, including cutting its benchmark rate. While another cut might be on the horizon later this year, it's important to remember that the Fed's actions don't always translate directly or immediately to lower mortgage rates. The market's reaction is a mix of the Fed’s commentary, broader economic signals, and other global factors.

- Economic Uncertainty Looms: We've been experiencing a period of market volatility. This general uncertainty can make mortgage rates behave in ways that seem unpredictable. Lenders are always trying to price in risk, and when the economic future feels fuzzy, rates can be more sensitive.

- The “Lock-In Effect” and Housing Inventory: A significant factor limiting housing inventory is the “lock-in effect.” Many homeowners secured mortgages at historically low rates years ago. Now, with current rates much higher, they're understandably reluctant to sell and give up those low rates. This keeps the supply of homes down. However, some sellers might be getting tired of waiting for rates to drop significantly, which could lead to a slight improvement in inventory.

- Expert Predictions for the Future: Looking ahead, expert forecasts for the 30-year fixed rate at the end of 2025 and into 2026 generally hover in the 6% range. However, it’s critical to understand that these are just predictions, and the housing market is notoriously tricky to forecast accurately. Things can change rapidly based on economic news and Fed policy.

My personal take? It’s a good sign that rates are easing, but I don't expect a sudden plunge back into the 4% or 5% range anytime soon unless there's a significant economic downturn. The 6% average is likely to be the new normal for a while, with dips and rises around it. For those who managed to miss the peak rates of 7% or more, that refinance opportunity is definitely one to explore right now.

Final Thoughts

Today, November 30th, presents a more favorable picture for mortgage rates, with the 30-year fixed at 6.00%. This is a welcome change and offers a glimmer of hope for buyers and refinancers alike. While a move into the 5% range is still a topic of much speculation, the current rates provide a more accessible entry point into the housing market than we've seen in recent months. Remember to do your homework, compare lenders, and work on improving your financial health to secure the best possible rate.

Invest Smartly in Turnkey Rental Properties

With rates dipping to their lowest levels, investors are locking in financing to maximize cash flow and long-term returns.

Norada Real Estate helps you seize this rare opportunity with turnkey rental properties in strong markets—so you can build passive income while borrowing costs remain historically low.

🔥 HOT NEW LISTINGS JUST ADDED! 🔥

Talk to a Norada investment counselor today (No Obligation):

(800) 611-3060

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?