Good news for those looking to refinance their homes! As of today, April 12, 2026, we're seeing a welcome dip in the most popular mortgage refinance rate. The average 30-year fixed refinance rate has fallen by 13 basis points compared to this time last week, landing at a more palatable 6.68%. This small bit of relief offers a glimmer of hope after a period of ups and downs in the market. This kind of movement can sometimes be the first sign of a shift, but it's important to understand what's behind it. While the 30-year fixed rate is moving in the right direction for refinancers, other rates are telling a slightly different story, and that’s worth digging into.

Mortgage Rates Today, April 12, 2026: 30-Year Refinance Rate Drops by 13 Basis Points

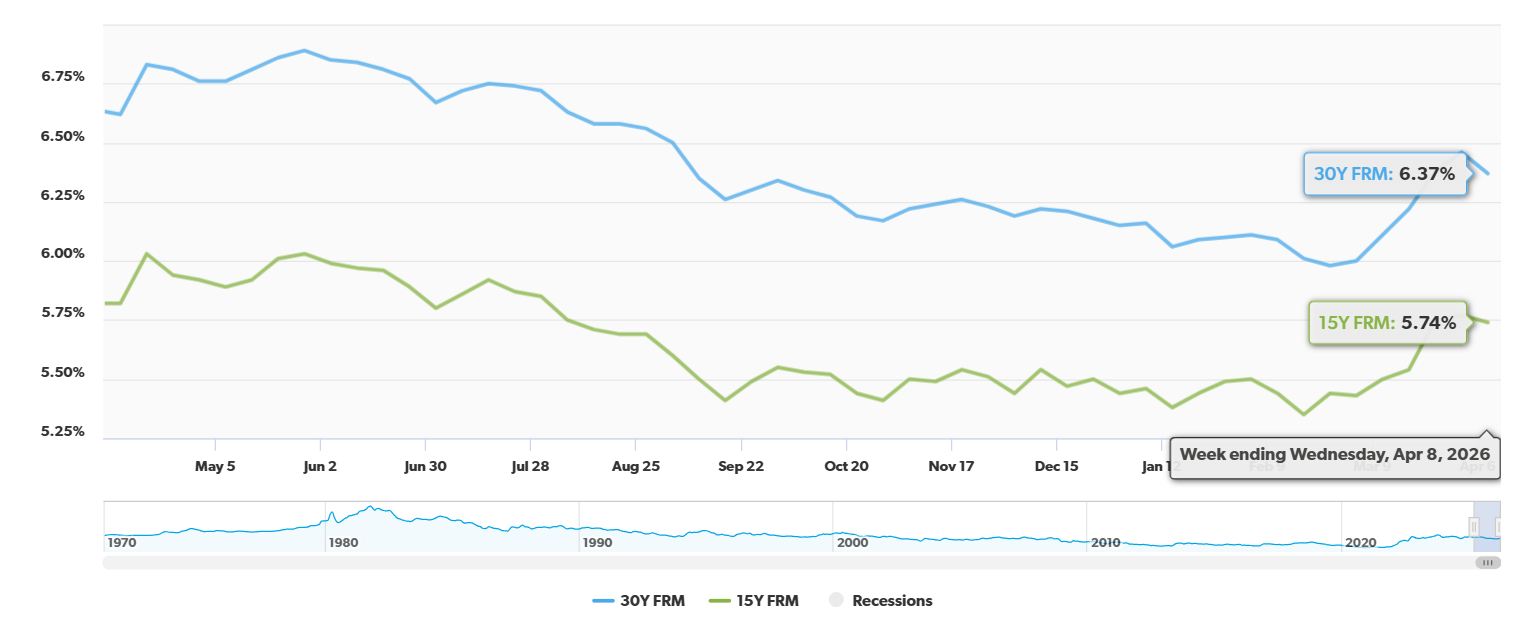

What the Numbers Tell Me Today

Let's break down the key figures reported by Zillow for April 12, 2026:

- 30-Year Fixed Refinance Rate: 6.68% (This is the big headline – a drop of 13 basis points from last week's average of 6.81%).

- 15-Year Fixed Refinance Rate: 5.68% (This rate is holding steady, which is great news for those who might be eyeing a shorter loan term).

- 5-Year ARM Refinance Rate: 7.14% (Uh oh, this one has actually gone up. It jumped 28 basis points today. This highlights the mixed signals we're getting from the market).

It's crucial to remember that these are average rates. Your personal rate could be different based on your credit score, the lender you choose, and other factors. This is why shopping around is always my top advice.

Why Is This Happening? Looking Deeper Than the Headlines

So, why the drop in the 30-year fixed refinance rate? It’s not just random chance. Several things are at play, and understanding them helps us see the bigger picture.

Think of mortgage rates like a seesaw. On one end, you have things like inflation and economic stability. On the other, you have demand and what the Federal Reserve is doing. Right now, it seems like some of the recent worries might be calming down just a tiny bit, allowing rates to breathe.

In late February and March, we saw some global events, like conflict in Iran, that caused oil prices to spike. This often makes investors a bit nervous, and they tend to put their money into safer things, like government bonds. When more people buy bonds, their prices go up, and their yields (which mortgage rates closely follow) go down. This is likely a big reason why we're seeing this slight dip today.

The “Lock-In” Effect: A Big Hurdle for Refinancers

Now, here's where my experience really comes into play. Even with this drop, most people aren't rushing to refinance. Why? It's mostly due to what we call the “lock-in effect.”

Back in the last few years, mortgage rates were incredibly low. It’s not uncommon for many homeowners, myself included during those times, to have secured rates well below 6%, and many even below 4%. The data backs this up: around 80% of U.S. mortgages are currently below 6%, and over half are under the 4% mark.

So, when current refinance rates are hovering around 6.68%, it just doesn't make much financial sense for the majority of people to go through the hassle and cost of refinancing. You'd be paying more interest over the life of the loan compared to what you're already paying. It’s like having a great deal on your favorite coffee and then considering a new deal that’s more expensive – you’d probably stick with the one you have!

Demand and Market Activity: A Tale of Two Halves

This “lock-in” effect explains why refinance demand has been weak. The Mortgage Bankers Association (MBA) pointed out that the Refinance Index took a big tumble last month (down 15% in late March). And just last week, refinance applications fell another 3% week-over-week, and they're down 4% compared to this time last year.

Because of this, refinancing makes up only about 44.3% of all mortgage applications. This is the lowest we’ve seen that number since way back in December 2025. It’s a clear sign that people who already have low rates are happy to keep them.

However, it’s not all doom and gloom in the housing market. While refinances are slow, the demand for buying a new home is still pretty strong. In fact, in March, the total volume of mortgage locks went up by 9.38%. This jump was mostly thanks to a huge 22.86% surge in home purchase locks. This shows that people are still eager to buy homes, even if they aren’t refinancing their existing ones. It’s a bit of a divergence, with one part of the market chugging along and the other feeling a bit stuck.

What's Next? Keeping an Eye on the Big Picture

As we look ahead, several factors will continue to influence mortgage rates.

- Inflation: The latest numbers on core CPI and jobs suggest that inflation is still a bit stubborn. This means the Federal Reserve will likely keep interest rates high for longer unless they see a clear sign that prices are cooling down.

- Federal Reserve Policy: What the Fed decides to do with interest rates is always a major driver. Any hints they give about future rate hikes or cuts will be watched very closely by the market.

- Global Stability: Those geopolitical events we talked about? Any further instability or shifts in global tensions can quickly impact markets and, consequently, mortgage rates.

From my perspective, the 30-year fixed refinance rate at 6.68% today is a small positive signal. But given the strong “lock-in” effect and the ongoing concerns about inflation, I don't expect a massive drop that would unlock widespread refinancing activity just yet. I think we'll likely continue to see a bit of choppiness. For a while, borrowers might be looking at rates staying in a range, perhaps between 6.0% and 6.5%, through the spring. It’s a good time to keep an eye on the news and see how these bigger economic forces play out.

Here’s a quick rundown to remember:

| Mortgage Type | Rate Today (April 12, 2026) | Change from Last Week |

|---|---|---|

| 30-Year Fixed Refinance | 6.68% | Down 13 basis points |

| 15-Year Fixed Refinance | 5.68% | Steady |

| 5-Year ARM Refinance | 7.14% | Up 28 basis points |

Ultimately, whether refinancing makes sense for you depends on your specific situation, your current interest rate, and your financial goals.

VS

Cleveland’s affordable rental with strong rent yield vs Kansas City’s larger 6‑bed property with higher NOI. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Market forecasts suggest steady demand, making turnkey real estate one of the most reliable paths to passive income and wealth creation.

Norada Real Estate helps investors capitalize on these trends with turnkey rental properties designed for appreciation and consistent cash flow—so you can grow wealth securely while others wait for clarity in the market.

Recommended Read:

- 30-Year Fixed Refinance Rate Trends – March 22, 2026

- Best Time to Refinance Your Mortgage: Expert Insights

- Should You Refinance Your Mortgage Now or Wait Until 2026?

- When You Refinance a Mortgage Do the 30 Years Start Over?

- Should You Refinance as Mortgage Rates Reach Lowest Level in Over a Year?

- Half of Recent Home Buyers Got Mortgage Rates Below 5%

- Mortgage Rates Need to Drop by 2% Before Buying Spree Begins

- Will Mortgage Rates Ever Be 3% Again: Future Outlook

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years