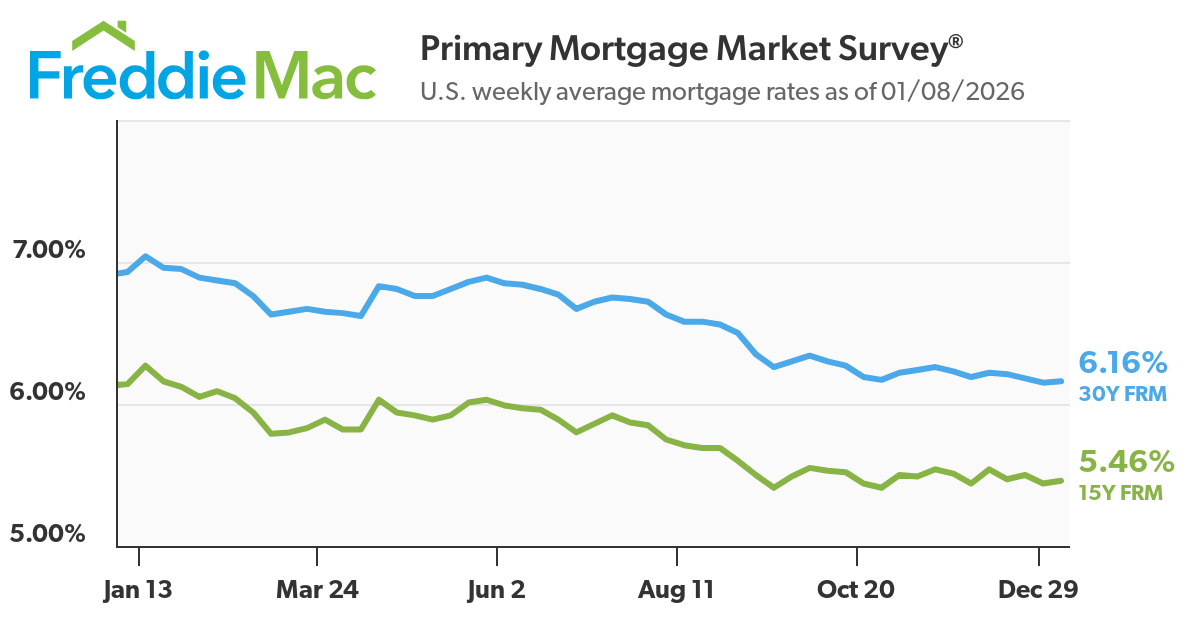

As of January 10th, the average 30-year fixed mortgage rate has dipped below 6%, currently sitting at 5.91%, and the 15-year fixed rate at 5.36%, according to Zillow. This is welcome news for many looking to buy a home, as it marks a return to levels not seen for quite some time. While these numbers are the headline, understanding what's behind them is what truly matters for anyone navigating the mortgage market.

Right now, we're seeing a particularly interesting combination of these forces at play. President Trump's recent proposals, including a ban on institutional buyers of single-family homes and a directive for Fannie Mae and Freddie Mac to purchase significant amounts of mortgage bonds, have definitely caught the market's attention and seem to be a driving factor behind this downward trend.

Today's Mortgage Rates, Jan 10: Homebuyers Can Get 30-Year Fixed Rate at 5.91%

Decoding Today's Numbers: A Snapshot

Let's break down what these rates mean practically. When we talk about mortgage rates, we're essentially looking at the cost of borrowing money to buy a house. A lower rate means you pay less in interest over the life of your loan, which can translate to substantial savings.

Here's a look at the average rates we're seeing today, according to Zillow:

| Loan Type | Average Rate |

|---|---|

| 30-year fixed | 5.91% |

| 20-year fixed | 5.83% |

| 15-year fixed | 5.36% |

| 5/1 ARM | 6.17% |

| 7/1 ARM | 6.36% |

| 30-year VA | 5.57% |

| 15-year VA | 5.21% |

| 5/1 VA | 5.36% |

You'll notice a few things here. The 30-year fixed is the most common choice for homebuyers because it offers a predictable monthly payment that stays the same for the entire loan term. The 15-year fixed has a lower interest rate, which means you pay off your mortgage faster and build equity more quickly, but your monthly payments will be higher.

Adjustable-rate mortgages (ARMs) like the 5/1 and 7/1 start with a lower initial interest rate for a set period, but then the rate can adjust periodically based on market conditions. These can be attractive if you plan to move or refinance before the initial fixed period ends, but they come with more uncertainty. VA loans, for those who qualify, often feature particularly attractive rates, as seen in the table, designed to support our nation's heroes.

The Ripple Effect of Government Action

The recent news regarding President Trump's proposed measures is a significant piece of the puzzle. His administration is looking at two key areas to influence mortgage rates:

- Banning Institutional Buyers: The idea here is to reduce competition from large companies that buy single-family homes, potentially making more properties available to individual buyers and, in theory, easing price pressures. While the direct impact on mortgage rates is debated, reducing demand from institutional investors could indirectly influence the housing market.

- Fannie Mae and Freddie Mac Bond Purchases: This is a more direct lever. Fannie Mae and Freddie Mac are government-sponsored enterprises that play a crucial role in the mortgage market by buying mortgages from lenders, packaging them into securities, and selling them to investors. When these entities purchase more mortgage bonds, it increases the demand for those bonds. Higher demand for mortgage bonds generally leads to lower bond yields, and since mortgage rates tend to follow bond yields, this action can push mortgage rates down.

The market has indeed responded favorably to these announcements. The fact that the 30-year fixed rate has dropped below 6% is a strong indicator of this. It's a psychology game as much as a financial one; when buyers and lenders see these kinds of interventions, it can create optimism and drive behavior.

What This Means for You (My Thoughts)

From my perspective, this move by the administration is a calculated attempt to stimulate the housing market. Lower mortgage rates make buying a home more affordable, which can encourage more people to enter the market. This is particularly important at a time when affordability has been a major concern for many.

However, it's always wise to be cautiously optimistic. While government intervention can have an immediate impact, the long-term sustainability of these lower rates depends on a variety of factors. Some experts are divided on whether these actions will lead to a sustained drop or just a temporary dip. I tend to agree that without continued, robust economic factors supporting lower rates, the effects might be modest or short-lived.

Beyond the Headlines: Key Influences

It’s not just presidential directives that move mortgage rates. Several underlying economic forces are constantly at play:

- The 10-Year Treasury Yield: This is one of the biggest indicators for mortgage rates. When the yield on the 10-year Treasury note goes up, mortgage rates typically follow, and vice versa. This is because mortgage-backed securities are often compared to Treasury bonds in terms of risk and return.

- Inflation: If inflation is high, the Federal Reserve might raise interest rates to cool down the economy, which can lead to higher mortgage rates. Conversely, slower-than-expected inflation reports, like those we've seen recently, can put downward pressure on rates.

- Economic Growth and Employment: A strong, growing economy with low unemployment can sometimes lead to higher interest rates as demand increases. However, a cooling labor market can signal that the economy is not overheating, which can also contribute to lower rates.

The recent reports of slower inflation and a cooling labor market in late 2025 have undoubtedly contributed to the general dip in rates we're observing. These fundamental economic signals are arguably more influential in the long run than any single policy announcement.

Looking Ahead: What Experts are Saying

Forecasting mortgage rates is a tricky business, and everyone has an opinion. However, based on current trends and expert analyses, here's what I'm hearing:

- Hovering Around 6%: Most experts anticipate that mortgage rates will continue to hover around the 6% mark for a good portion of 2026. This suggests a period of relative stability compared to the sharp fluctuations seen in previous years.

- Potential for Further Dips: Some forecasts, including those from entities like Fannie Mae, suggest that the 30-year fixed rate could dip slightly below 6% by the end of the year. This would be a continuation of the positive trend we're seeing today.

- Market Volatility: While there's a trend towards stabilization, remember that rates can still fluctuate daily. It's essential to stay informed and act when the time is right for you.

My Takeaway for Homebuyers

If you're considering buying a home, these current rates offer a compelling opportunity. The fact that the 30-year fixed is below 6% is a significant psychological and financial milestone. My advice is to:

- Get Pre-Approved: This will give you a clear understanding of what you can afford and lock in a rate for a period, giving you some breathing room.

- Shop Around: Don't just go with the first lender you talk to. Compare offers from multiple lenders to ensure you're getting the best deal.

- Consider Your Long-Term Plans: Will you be in this home for five years, or twenty-five? This will influence whether a fixed-rate or an ARM might be a better fit for your situation.

- Stay Informed: Keep an eye on market news and consult with a trusted mortgage professional.

Navigating the mortgage market can feel overwhelming, but with a little understanding and a lot of homework, you can make informed decisions that set you up for success. Today's rates are a positive sign, and with careful planning, this could be your moment to achieve the dream of homeownership.

VS

Tennessee’s balanced rental vs Texas’s larger home with lower cap rate. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Talk to a Norada investment counselor (No Obligation):

(800) 611-3060

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?