Ever get that uneasy feeling, like something just isn't quite right with the way things are going? That's the vibe I'm getting when I look at the latest economic forecasts. A recent CNBC survey of 14 economists points to a significant slowdown in growth, with the economic growth in the first quarter of this year projected to be a meager 0.3%. This sluggish pace, the weakest since the pandemic recovery, is largely attributed to the chilling effect of new tariffs, which appear to be creating conditions ripe for stagflation – a nasty combination of slow growth and persistent inflation.

Economist Survey Predicts Weak Q1 GDP Due to Tariffs

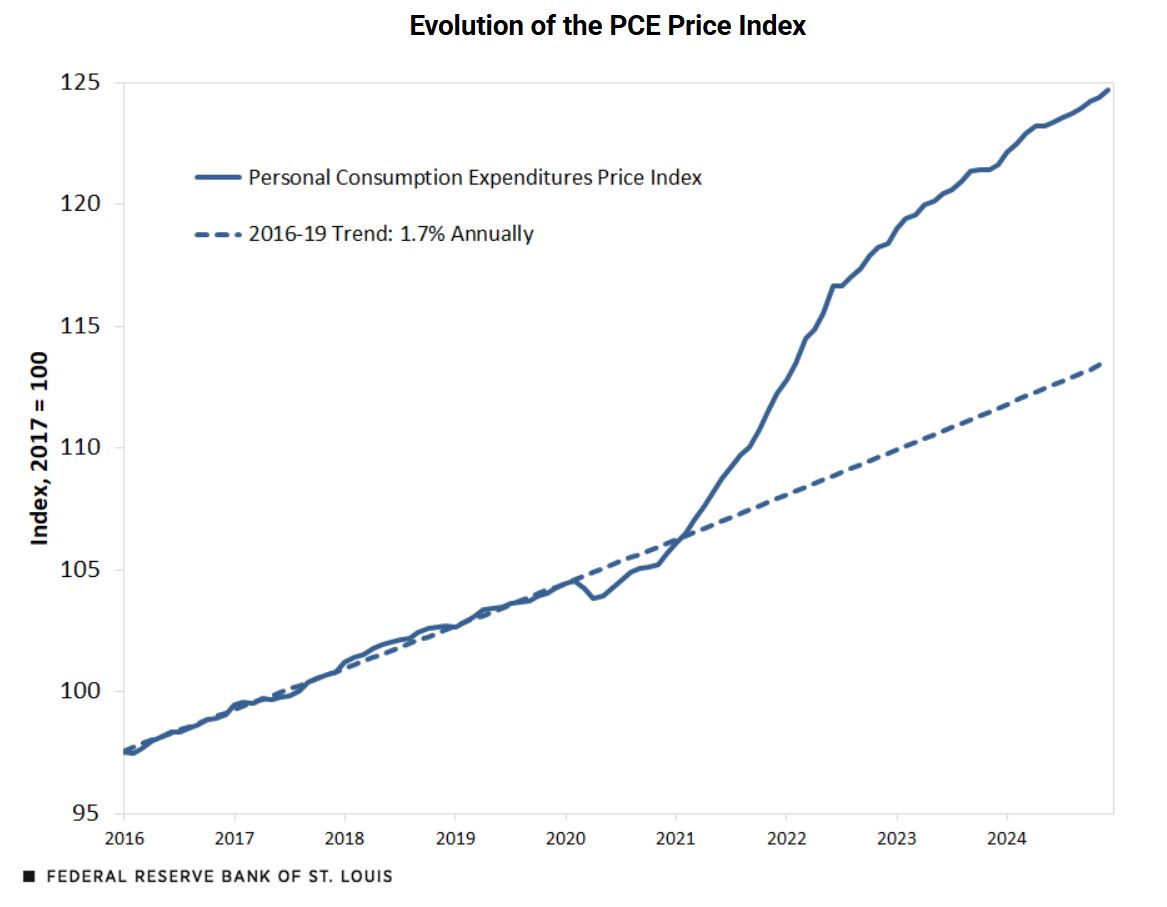

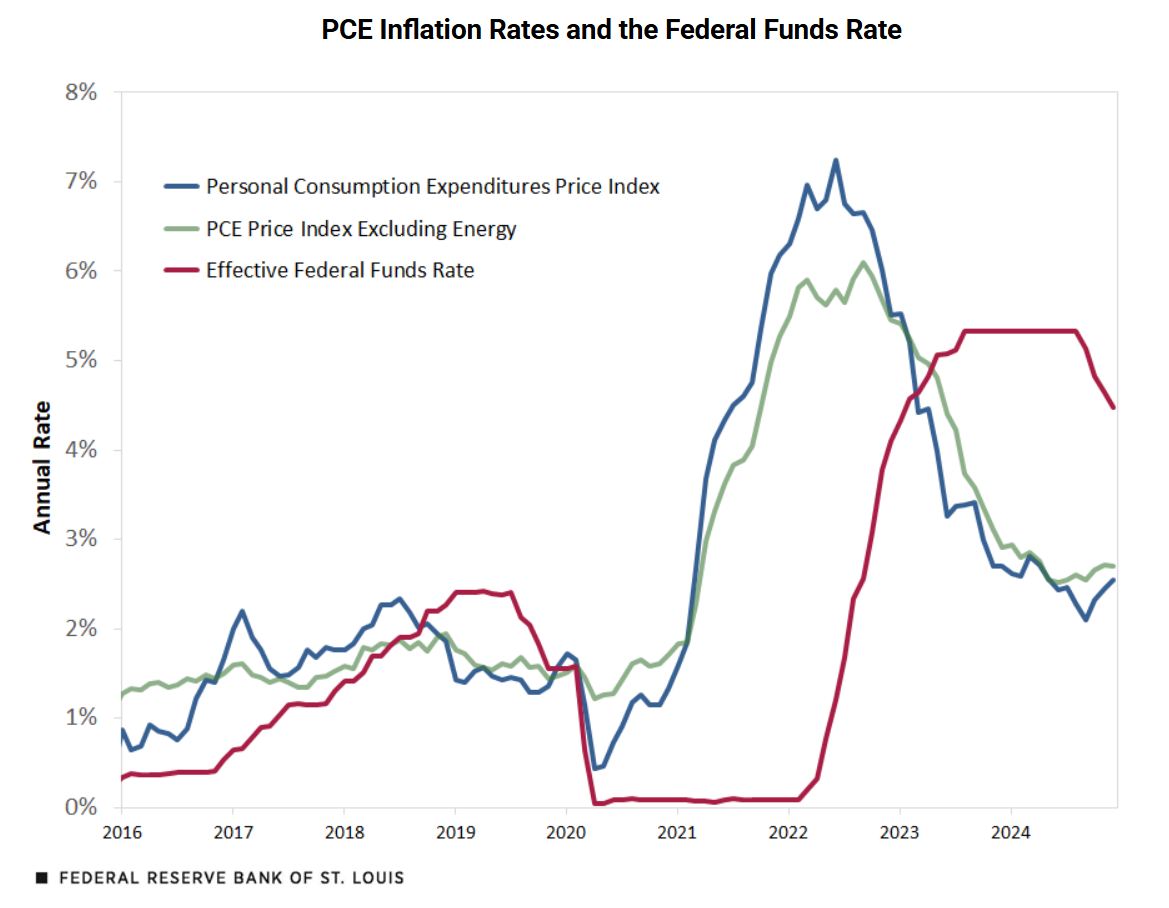

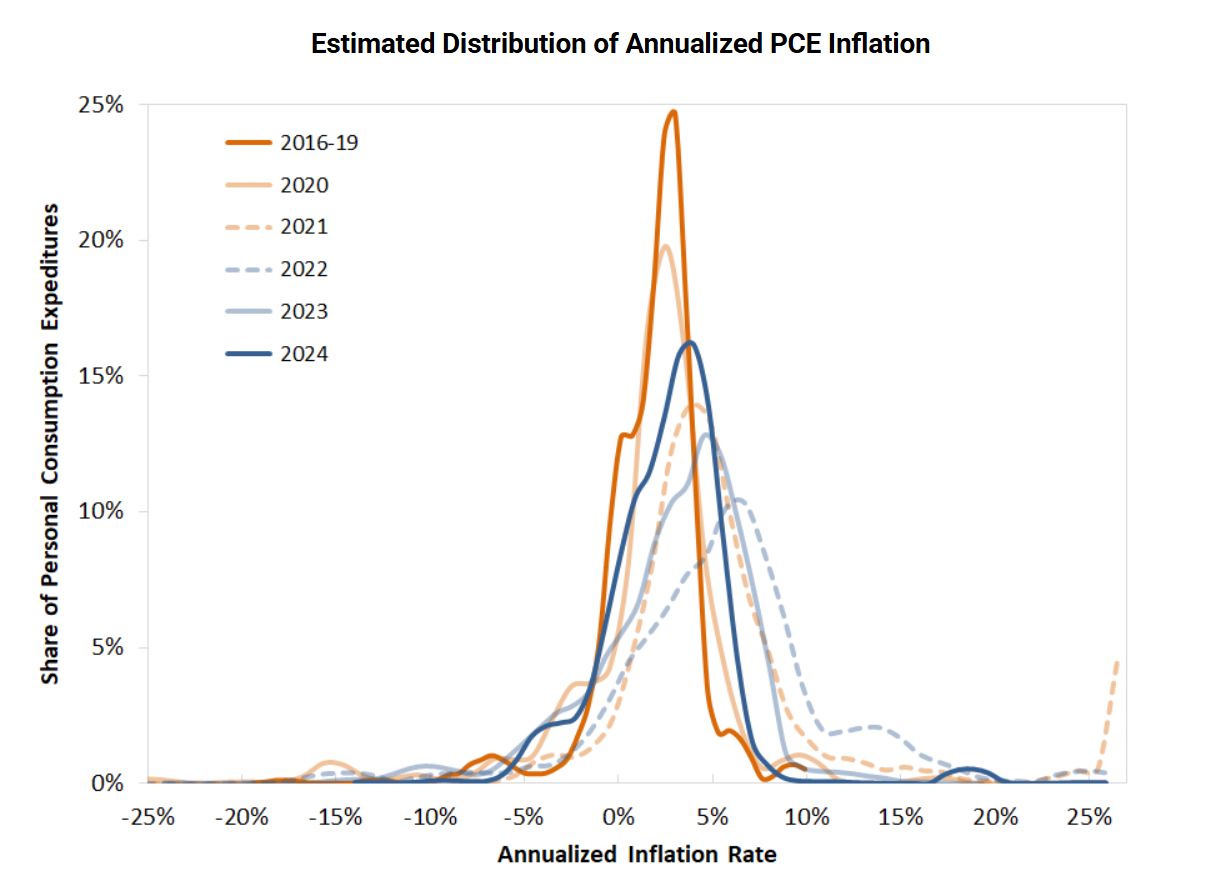

It feels like just yesterday the economy was showing some decent momentum, but these new numbers paint a starkly different picture. Seeing growth plummet from the previous quarter's 2.3% to a near standstill is definitely cause for concern. And the fact that core inflation, as measured by the Personal Consumption Expenditures (PCE) price index, the Federal Reserve's preferred gauge, is expected to remain stubbornly high around 2.9% for most of the year only adds fuel to this worrying outlook.

Why the Sudden Slowdown? The Tariff Tango

From where I'm sitting, the main culprit seems pretty clear: the uncertainty and the actual implementation of new, sweeping tariffs from the current administration. It's like throwing sand in the gears of the economic machine. Businesses become hesitant to invest, and consumers, facing potentially higher prices, tighten their purse strings.

We're already seeing signs of this in the real economic data. The Commerce Department recently reported that inflation-adjusted consumer spending in February barely budged, rising by a paltry 0.1%, following a 0.6% decline in January. This is a significant drop from the robust spending growth we saw in the last quarter of the previous year. As Barclays economists noted, the earlier decline in sentiment is now translating into a tangible slowdown in economic activity.

Another factor playing a role is a noticeable surge in imports. Now, on the surface, more goods coming into the country might seem like a good thing. However, in the context of impending tariffs, it appears businesses are rushing to bring in goods before the higher taxes kick in. While this might offer some short-term relief in terms of supply, these imports actually subtract from the GDP calculation. It's a bit of a temporary distortion, but it contributes to the weak first-quarter growth number.

Stagflation's Shadow: A Looming Threat

The prospect of stagflation is particularly troubling. Think about it: slow economic growth means fewer job opportunities and potentially stagnant wages. At the same time, persistent inflation erodes the purchasing power of the money we do have. It's a squeeze on both ends, and it can be incredibly difficult to break free from.

The CNBC survey highlights that core PCE inflation isn't expected to fall convincingly until the very end of the year. This stubbornness will likely tie the Federal Reserve's hands. While the market might be hoping for interest rate cuts to stimulate the slowing economy, the Fed will be hesitant to lower rates while inflation remains well above their target. It's a tricky situation, a real balancing act with potentially significant consequences.

Not All Doom and Gloom? A Glimmer of Hope

It's important to note that not all economists are predicting a complete downturn. The survey indicates that only a couple of the 12 economists who provided specific growth numbers for the first quarter foresee negative growth. And importantly, none are forecasting consecutive quarters of contraction, which is often a key indicator of a recession.

Oxford Economics, for instance, while having one of the lowest Q1 growth estimates (-1.6%), anticipates a rebound in the second quarter, projecting GDP growth to bounce back to 1.9%. Their reasoning is that the surge in imports during the first quarter will eventually translate into positive contributions to growth as these goods are either added to inventories or sold to consumers. It's a bit of a delayed effect.

Recession Risks on the Rise

Despite the hopes for a rebound, the margin for error looks slim. An economy growing at a snail's pace of 0.3% is incredibly vulnerable to any further shocks. And with the new tariffs expected to be implemented this week, the risks of slipping into negative territory have definitely increased.

As Mark Zandi of Moody's Analytics aptly put it, even though their baseline forecast doesn't show a decline in GDP, the mounting global trade war and potential cuts to jobs and funding create a “good chance GDP will decline in the first and even the second quarters of this year.” He further warns that a recession becomes likely if the president doesn't reconsider the tariffs by the third quarter. That's a pretty stark warning from a respected economist.

Moody's Analytics themselves are projecting a slightly better first quarter growth of 0.4%, with a rebound to 1.6% by the end of the year. However, even this more optimistic scenario still represents growth that is modestly below the long-term trend.

My Take: Navigating Choppy Waters

Personally, I find these forecasts deeply concerning. While I understand the arguments sometimes made in favor of tariffs – like protecting domestic industries – the potential for widespread economic disruption and the creation of stagflationary conditions seem to outweigh any perceived benefits in this current climate.

The interconnected nature of the global economy means that tariffs rarely have a unilateral effect. They often lead to retaliatory measures from other countries, resulting in a trade war that hurts businesses and consumers on all sides. The uncertainty created by these policies also discourages investment, which is crucial for long-term economic growth and job creation.

The fact that inflation is proving to be so sticky further complicates matters. The Federal Reserve's usual toolkit for dealing with slow growth – lowering interest rates – becomes less effective when inflation is still a significant problem. They risk further fueling price increases if they ease monetary policy prematurely.

Looking Ahead: A Need for Course Correction?

The coming months will be critical. We'll need to closely monitor economic data, particularly consumer spending, business investment, and inflation figures, to see if the anticipated rebound materializes or if the risks of a more significant downturn become reality.

It seems to me that a reassessment of the current trade policies might be necessary to avoid potentially serious economic consequences. Finding ways to foster international trade and cooperation, rather than erecting barriers, could be a more sustainable path to healthy economic growth.

In the meantime, businesses and individuals will need to navigate this period of uncertainty with caution. For businesses, this might mean carefully managing costs and delaying major investment decisions. For individuals, it could mean being mindful of spending and saving where possible.

The economic forecast for the first quarter serves as a stark reminder that policy decisions have real-world impacts. I sincerely hope that policymakers take these warnings seriously and consider adjustments to avoid the specter of stagflation becoming a reality.

Work With Norada – Build Wealth

With economists warning of stagflation and weak Q1 GDP due to tariffs, now is the time to invest in stable, income-generating real estate for financial security.

Norada’s turnkey rental properties provide consistent cash flow and long-term wealth, no matter the economic climate.

Speak with our expert investment counselors (No Obligation):

(800) 611-3060

Read More:

- Goldman Sachs Significantly Raises Recession Probability by 35%

- 2008 Crash Forecaster Warns of DOGE Triggering Economic Downturn

- Stock Market Predictions 2025: Will the Bull Run Continue?

- Stock Market Crash: Nasdaq 100 Tanks 3.5% Amid AI Concerns

- Stock Market Crash Prediction With Huge Discounts on Bitcoin, Gold, Houses

- S&P 500 Forecast for the Next Year: What to Expect in 2025?

- Stock Market Predictions for the Next 5 Years

- Billionaire Warns of Stock Market Crash If Harris Wins Elections

- Stock Market is Predicted to Surge Regardless of the Election Outcome

- Echoes of 1987: Is Today’s Stock Market Crash Leading to a Recession?

- Is the Bull Market Over? What History Says About the Stock Market Crash

- Wall Street Bear Predicts a Historic Stock Market Crash Like 1929

- Economist Predicts Stock Market Crash Worse Than 2008 Crisis

- Stock Market Forecast Next 6 Months

- Next Stock Market Crash Prediction: Is a Crash Coming Soon?

- Stock Market Crash: 30% Correction Predicted by Top Forecaster