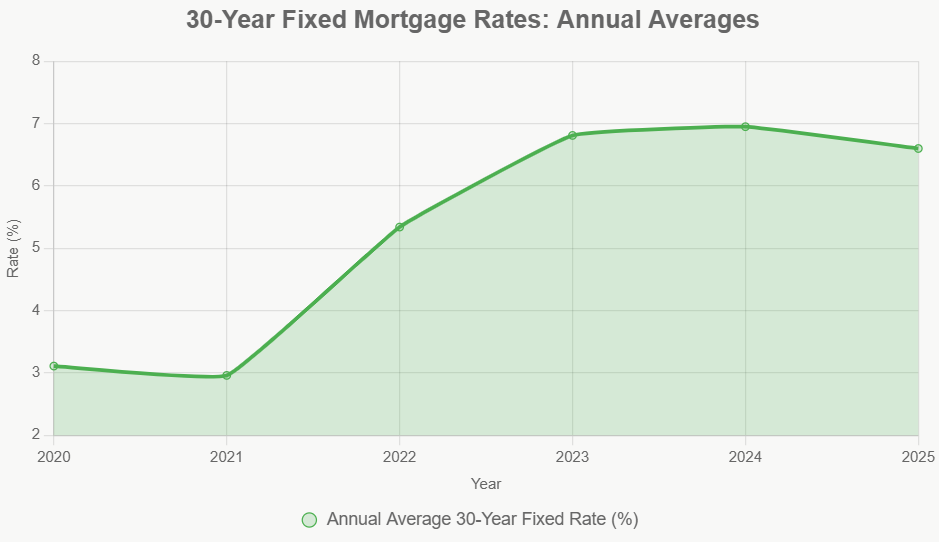

The wait is finally over for many prospective homeowners and those looking to refinance. According to Freddie Mac, the 30-year fixed-rate mortgage has officially dropped to its lowest point in more than three years, settling at an average of 6.06% as of January 15, 2026. This significant dip, a welcome change from the 7.04% seen a year ago, is already sparking a noticeable uptick in home buying and refinancing activity, signaling a potentially robust spring housing season.

It’s not just a number on a chart; it translates into real opportunities for people to achieve their homeownership dreams or improve their financial situation. This drop, according to Freddie Mac's survey, is a direct result of some smart financial plays and a hopeful outlook on interest rates from the Federal Reserve. It’s like the market is taking a collective deep breath and getting ready to spring into action.

Mortgage Rates Hit Lowest Level in 3 Years After Prolonged Highs

Why This Rate Drop Matters: Beyond the Numbers

You might be thinking, “Okay, rates are down, great!” But let's dive a bit deeper into what that 6.06% really means for you. For starters, it’s about making that dream home more affordable. Imagine what you could do with the savings from a lower monthly payment over the life of a 30-year loan. It's not just about getting into a house; it's about making homeownership sustainable and less of a financial strain.

And it’s not just for buyers. For those who are already homeowners but have been stuck with higher rates, this is a golden opportunity to refinance. This could mean lowering your monthly payments, freeing up cash for other financial goals, or even shortening your loan term. The Freddie Mac data shows a stunning 40% surge in refinance activity, which tells me many people are recognizing this immediate benefit.

The “Lock-In Effect” Begins to Thaw

One of the biggest topics in the housing market over the past couple of years has been the “lock-in effect.” This is where homeowners with super-low mortgage rates from the pandemic (think under 3%) are hesitant to sell because they'd have to buy a new home at much higher rates. However, this new low is changing the game. Freddie Mac notes that the share of homeowners with rates above 6% is now larger than those with rates below 3%. This is a crucial indicator! It suggests that more existing homeowners might now find it financially sensible to sell, which could lead to more homes hitting the market. More inventory is always good news for buyers, as it can help ease competition and potentially stabilize prices.

What's Driving These Falling Rates?

It's rarely just one thing, but in this case, there are some clear catalysts. As mentioned, expectations of further Federal Reserve rate cuts are a major influence. The Fed’s actions (or anticipated actions) ripple through the financial markets, and mortgage rates are highly sensitive to them.

But there was also a very specific, impactful announcement: President Trump's declaration that Fannie Mae and Freddie Mac would purchase $200 billion in mortgage bonds. This is a significant move. When these government-sponsored enterprises buy bonds, it increases demand for them. Higher demand for these bonds typically leads to lower yields, and lower mortgage-backed security yields directly translate to lower mortgage rates for consumers. It’s a direct intervention designed to make borrowing cheaper, and it’s clearly working.

Savings You Can See: A Table of Impact

Numbers can be dry, but let's make them relatable. Consider the difference in monthly payments and the total savings over 30 years for a hypothetical $300,000 mortgage:

| Current Rate (Jan 15, 2026) | Previous Rate (Last Week) | Rate Savings per Month | Total Savings Over 30 Years |

|---|---|---|---|

| 6.06% (30-Yr FRM) | 6.16% | $51.50 | $18,540 |

| 5.38% (15-Yr FRM) | 5.46% | $37.50 | $6,750 |

Note: These are approximate savings and do not include potential changes in taxes, insurance, or HOA fees.

As you can see, even a small drop in interest rate makes a tangible difference. That $51.50 extra in your pocket each month on a 30-year loan adds up to nearly $18,540 over the loan's lifetime. That's money that can go towards renovations, savings, or simply enjoying life a little more.

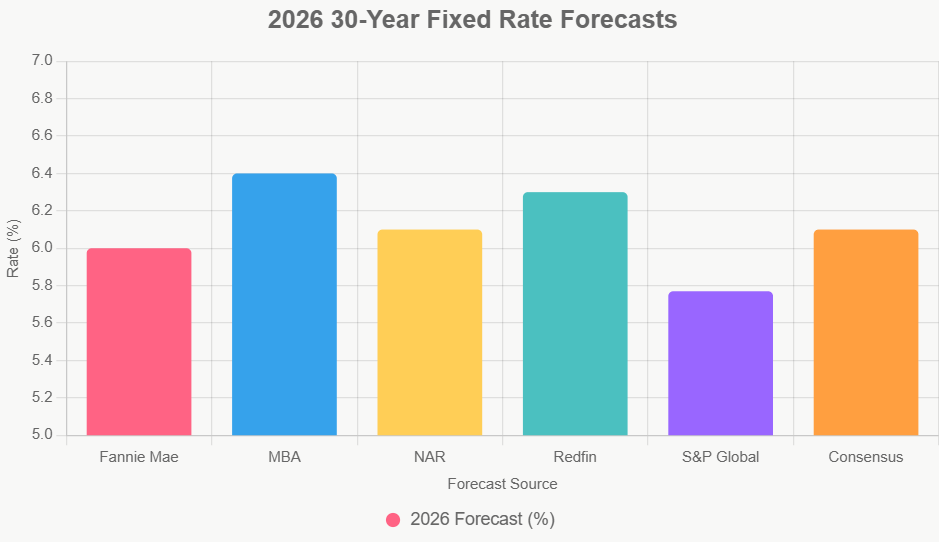

Expert Opinions: What's Next for Mortgage Rates?

While I always advise readers not to try and perfectly time the market – it’s an incredibly difficult game to play – it’s helpful to hear what the experts are predicting. The general sentiment, according to Freddie Mac's survey and other market watchers, is that rates are likely to stay in the low 6% range. Some forecasts even suggest we could see them dip below 6% by the end of this year.

This is encouraging news for the spring housing market. A more stable and potentially lower interest rate environment can give buyers more confidence and make affordability a less daunting hurdle. While we might not see the frenzied, sub-3% rates of the pandemic era again anytime soon, this current climate is far more conducive to a healthy and active housing market.

A Boost for Various Loan Types

It's not just the conventional 30-year fixed mortgage that's seeing benefits. Other loan types are also reflecting this downward trend:

- 30-Year FHA Loans: Averaging 5.70%, down from the previous week.

- 30-Year VA Loans: Also averaging 5.72%, showing a similar decrease.

This means that a broader range of borrowers, including those who might use FHA or VA loans, can benefit from these lower borrowing costs.

My Take: Cautious Optimism, Real Opportunity

From my perspective, this is a welcome development after a period of uncertainty and higher costs. It’s not a signal that prices are about to skyrocket, but rather an indication that the market is finding a more balanced and accessible rhythm. For anyone who has been on the fence about buying or refinancing, now is definitely the time to get serious and start exploring your options. Get pre-approved, speak with lenders, and see what these lower rates can do for your personal financial picture. The 30-year fixed-rate mortgage hitting its lowest level in over three years is a significant event, and one that could pave the way for a much brighter housing outlook.

and

Florida’s A+ affordable rental vs Punta Gorda’s larger high‑yield property. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Talk to a Norada investment counselor (No Obligation):

(800) 611-3060

Also Read:

- What Leading Housing Experts Predict for Mortgage Rates in 2026

- Mortgage Rate Predictions for 2026: What Leading Forecasters Expect

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?