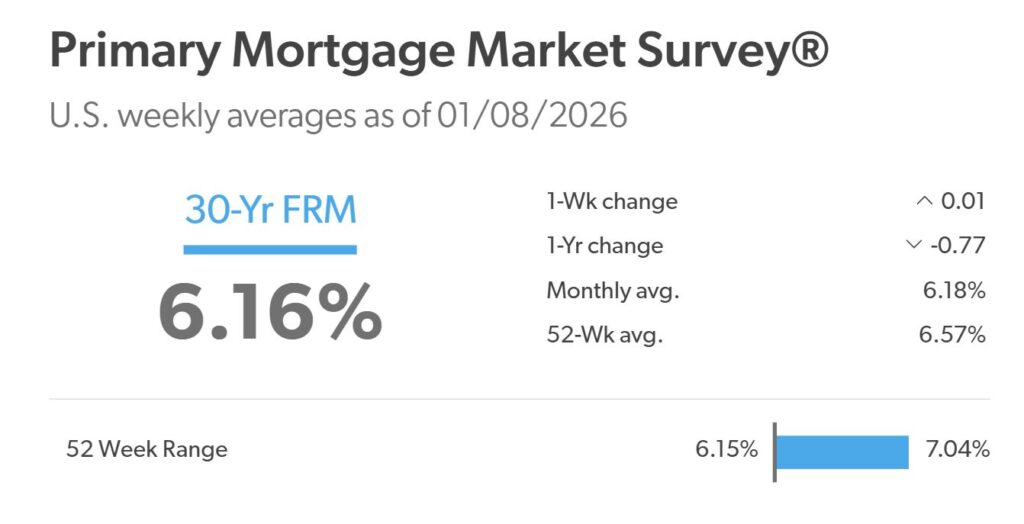

As of January 12, 2026, mortgage rates, according to Zillow, have seen a gentle dip. The most popular choice, the 30-year fixed-rate mortgage, now sits around 5.91%, a slight decrease from the previous week. This movement suggests a more favorable environment for homebuyers and those looking to refinance. The headline takeaway is that mortgage rates saw a modest decrease this week, with the 30-year fixed falling below 6%.

Today’s Mortgage Rates, Jan 12: 30-Year Fixed Loan Rate Persists Below 6%

Key Takeaways from Today's Rate Snapshot:

- Good News for Fixed-Rate Borrowers: Both the 30-year and 15-year fixed-rate mortgages have seen a decrease in their average rates compared to last week.

- The 30-Year Fixed Continues to Reign: This loan type remains the go-to for most homeowners due to its predictable, lower monthly payments.

- Shorter Terms Offer Savings: While the monthly payment is higher, the 15-year fixed rate presents a clear path to paying off your home faster and saving on interest over the life of the loan.

- ARMs are a Bit of a Gamble Right Now: With current fixed rates being quite competitive, adjustable-rate mortgages aren't the automatic savings they used to be.

Breaking Down Current Mortgage Rates

It’s helpful to see the numbers laid out clearly, so you can compare them. Zillow's data for January 12, 2026, gives us a solid picture of the current national average rates for various loan types. Please keep in mind these are averages, and your individual rate will depend on your credit score, down payment, and other financial factors.

| Loan Type | Average Rate (%) |

|---|---|

| 30-Year Fixed | 5.91 |

| 20-Year Fixed | 5.83 |

| 15-Year Fixed | 5.36 |

| 10-Year Fixed | 5.50 |

| 30-Year FHA | 6.12 |

| 30-Year VA | 5.57 |

| 5/1 ARM | 6.17 |

| 7/1 ARM | 6.36 |

Weekly Rate Comparison:

- 30-Year Fixed: Saw a drop of about 15 basis points from last week, moving from roughly 6.06% down to 5.91%.

- 15-Year Fixed: Also decreased by approximately 14 basis points, from around 5.50% to 5.36%.

Deeper Dive: Why Are Rates Moving?

It's easy to just look at the numbers, but understanding why they're moving is crucial. The recent dip in mortgage rates, especially for those long-term fixed loans, isn't just random. Economists are pointing to two main drivers: proposed housing initiatives and labor market data.

The government is clearly trying to make housing more accessible, and these proposals often signal to the market that efforts are being made to stabilize or even lower borrowing costs. On the other hand, how many jobs are being created or lost, and how wages are changing, directly impacts inflation concerns. When the labor market cools down a bit (meaning fewer job openings or slower wage growth), it often signals to the Federal Reserve that inflation might not be as big of a worry, which can lead to lower interest rates across the board, including mortgages.

The Reign of the 30-Year Fixed: Still King

The 30-year fixed-rate mortgage at 5.91% on January 12, 2026, is still the undisputed champion for a reason. Its magic lies in spreading the loan repayment over 360 months. This amortization schedule results in a lower monthly payment compared to shorter-term loans, making it more manageable for most household budgets. This predictability is a huge comfort, allowing homeowners to plan their finances without the worry of their monthly housing cost jumping up unexpectedly.

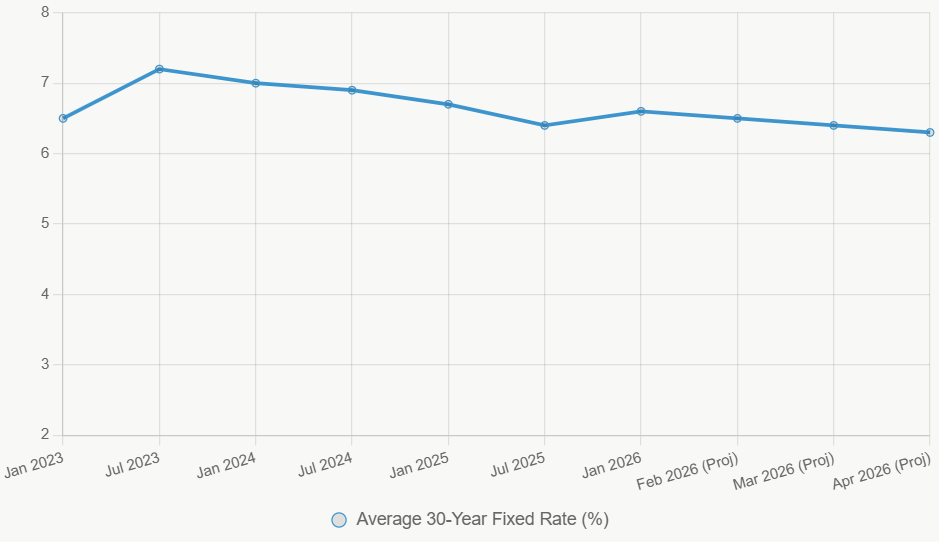

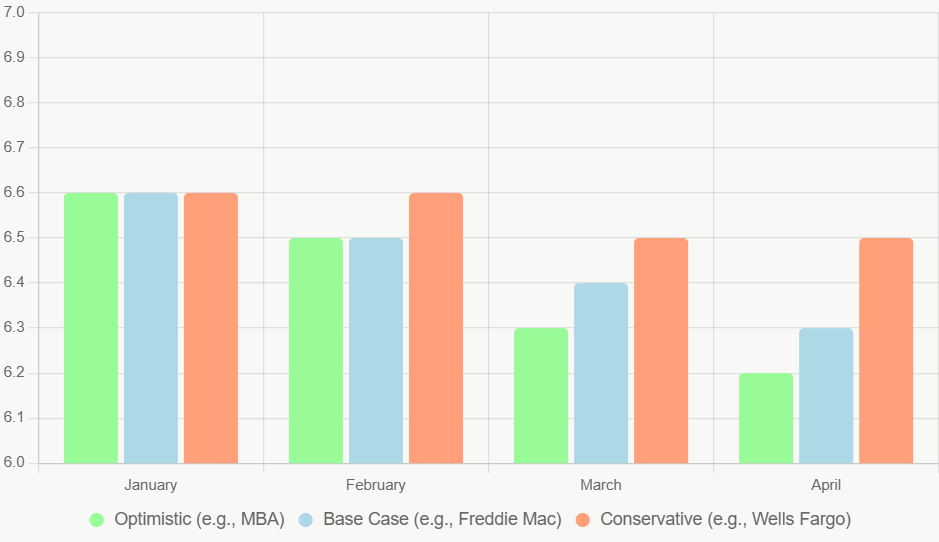

While today's rates have dipped below 6%, the outlook for much of 2026 suggests we might see them hover around or slightly above that mark. Persistent inflation worries are a significant factor here. However, economists are cautiously optimistic that by the end of the year, we might see a return to rates closer to the 5.9% range. This suggests a period of relative stability, with potential for further moderation as the year progresses.

The 15-Year Fixed: A Fast Track to Equity

At 5.36%, the 15-year fixed-rate mortgage is a fantastic option for those who can handle a higher monthly payment. The trade-off, however, is substantial. You're essentially paying off your mortgage in half the time compared to a 30-year loan. This means you'll pay significantly less interest over the entire life of the loan and build equity in your home much faster.

Right now, the difference (or “spread”) between the 15-year and 30-year rates is about 55 basis points. This wider gap makes the 15-year term even more attractive for buyers who prioritize building wealth through homeownership quickly. If you have a stable income and plan to stay in your home for a long time, the 15-year fixed can be a financially powerful choice.

Adjustable-Rate Mortgages (ARMs): A Different Ballgame in 2026

The 5/1 ARM is currently at 6.17%. Historically, the main appeal of an ARM was its lower initial interest rate compared to a fixed-rate mortgage. This allowed borrowers to save money in the first few years of their loan. However, in today's market of early 2026, many of the fixed rates are actually starting lower than these introductory ARM rates.

This “inverted” relationship is quite unusual. It means that unless you have a very specific plan – like knowing you'll sell your home or refinance before that five-year fixed period is up – an ARM might not be the cost-saver you expect. If interest rates rise significantly after the initial period, your monthly payments could become much higher and unpredictable. For most people, the security of a fixed rate at these current levels is likely more appealing.

Market Context: A “Year of Small Wins” for Homebuyers

The housing economists are framing 2026 as a “year of small wins” for homebuyers. This is largely due to the ongoing efforts to improve housing affordability. The new housing reform proposals are designed to encourage more building and make homes more accessible. While dramatic price drops aren't expected, the hope is that a combination of stabilizing home prices and income growth finally catching up will gradually bring affordability back to more typical levels.

While credit for refinance rates is not given in the prompt, it is worth mentioning that Zillow's refinance rates for a 30-year term are averaging 6.29%. This indicates that while rates have dipped for new purchases, refinancing might still be a higher hurdle for some, though the current dip could make it more attractive than it was a week prior.

State-by-State Variations: Small Differences, Big Implications

While national averages are a great starting point, mortgage rates can vary slightly from state to state. As of January 12, 2026, Zillow shows some states like California, Indiana, Kentucky, North Carolina, and Texas clustering around a slightly lower average of 5.875% for a 30-year fixed, while New York is a bit higher at 6.25%.

| State | 30‑Year Fixed Mortgage Rate | Notes |

|---|---|---|

| California | 5.875% | Slightly lower than national avg |

| Indiana | 5.875% | Slightly lower than national avg |

| Kentucky | 5.875% | Slightly lower than national avg |

| North Carolina | 5.875% | Slightly lower than national avg |

| Texas | 5.875% | Slightly lower than national avg |

| New York | 6.25% | Higher than national avg |

These differences, though seemingly small, happen because of a few things:

- Laws: States with judicial foreclosure laws (where lenders must go through courts to foreclose) sometimes have slightly higher rates to account for the longer process and potential costs.

- Local Economy: A strong local job market and high demand can influence rates. Conversely, areas where many lenders are competing for business might see lower rates.

- Operating Costs: The general cost of doing business for lenders in a particular state can also filter down into the rates they offer.

Expert Insights: What Lies Ahead?

From my perspective, the consensus among housing experts and economists for 2026 is one of gradual moderation.

- Rate Stability: The prevailing thought is that rates are likely to stay within a narrow range, probably hovering around the 6% mark for the foreseeable future, unless a major economic event shakes things up.

- Economic Drivers: It’s important to remember that mortgage rates aren't just tied to the Federal Reserve's main interest rate. They are much more closely linked to the yield on 10-year Treasury notes and broader inflation trends. Positive news on inflation or a cooling job market can definitely push rates downwards.

- 2026 Outlook: Most forecasts point to a modest downward trend in mortgage rates throughout the year. Some predict we could see them dip below 6% by the end of 2026.

- Buyer Behavior: While today's rates are significantly higher than the ultra-low rates we saw during the pandemic, their current stability is a positive for buyers. It allows for better financial planning. This stability, coupled with moderating price growth, is starting to re-engage buyers who were on the sidelines.

It's an interesting time in the housing market. While we're not seeing the rock-bottom rates of the past, the current environment offers a level of predictability that can be very beneficial for those looking to make a move.

and

Florida’s A+ affordable rental vs Punta Gorda’s larger high‑yield property. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Talk to a Norada investment counselor (No Obligation):

(800) 611-3060

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?