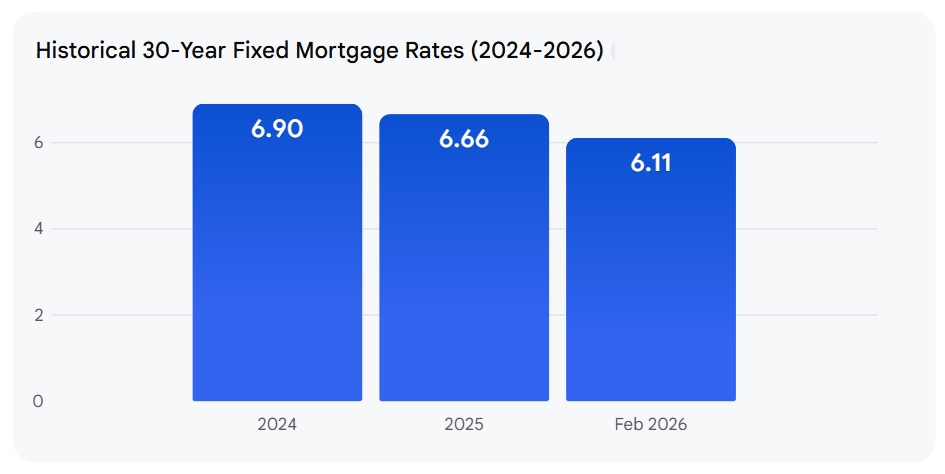

If you've been watching mortgage rates like I have, you'll be happy to hear that the average 30-year fixed refinance rate dropped by 11 basis points today, February 15, 2026, bringing it down to 6.44%. This is a welcome bit of good news for homeowners looking to secure a better deal on their mortgage.

Let's dive into what these numbers mean and if it might be your moment to refinance.

Mortgage Rates Today, February 15: 30-Year Refinance Drops by 11 Basis Points

Current Refinance Snapshot: February 15, 2026

Here's a quick look at the national refinance rates as reported by Zillow for this specific day:

| Mortgage Type | Current Rate (Feb 15, 2026) | Last Week's Average | Change |

|---|---|---|---|

| 30-Year Fixed Refi | 6.44% | 6.55% | -11 bps |

| 15-Year Fixed Refi | 5.46% | 5.46% | Steady |

| 5-Year ARM Refi | 6.97% | 6.97% | Steady |

(Note: bps stands for basis points, where 100 basis points equal 1 percentage point.)

As you can see, the biggest mover today is the 30-year fixed refinance rate, now sitting at 6.44%. That's a noticeable drop from last week's 6.55%. The 15-year fixed refinance rate remained solid at 5.46%, and the 5-year adjustable-rate mortgage (ARM) refinance rate held its ground at 6.97%.

What This Rate Drop Really Means for You

When you hear about rates dropping, especially by a few basis points, it might not sound like a huge deal. But trust me, in the world of mortgages, even small shifts can add up to significant savings over time.

- For the 30-Year Fixed Refinance: That drop to 6.44% is a signal, especially for those of you who've been on the fence about refinancing. If you had a mortgage with a rate higher than this, say you took it out when rates were north of 7% (which wasn't too long ago, like January 2025), this could be the nudge you need. Why? Because locking in a lower rate means lower monthly payments, and over the many years of a 30-year mortgage, those savings can be substantial. Imagine shaving off hundreds of dollars from your monthly payment – that's money you can use for other things, like saving for retirement, paying for your kids' education, or just enjoying life a bit more.

- For the 15-Year Fixed Refinance: The rate holding steady at 5.46% is great news if you're someone who likes to pay off your home faster. This shorter term often comes with a lower interest rate. By choosing a 15-year fixed refi, you'll pay more each month than with a 30-year loan, but you'll build equity quicker and pay way less interest overall. It’s a solid strategy for long-term financial health.

- For the 5-Year ARM Refinance: At 6.97%, ARMs are generally higher than their fixed-rate counterparts right now. However, they can still be attractive for a specific group of people. If you plan on selling your home or refinancing again within the next five years, an ARM might make sense. Your initial rate is fixed, and if you move before it adjusts, you avoid the risk of future rate hikes. It’s a calculated gamble, and for some, it pays off.

The Big Picture: Refinance Demand is Surging!

It's not just my observation; the data backs it up. The Mortgage Bankers Association (MBA) Refinance Index has seen a massive 101% surge year-over-year. That’s a huge jump compared to early 2025! What this tells me is that a lot of homeowners are actively looking to refinance.

And who are these people? It's estimated that about 4.8 million homeowners are now in a position to benefit financially from refinancing. This is the highest number we've seen since early 2022. It feels like a significant refi window has opened up, especially for those who secured loans when rates were much higher.

What's interesting is how this surge is playing out. Many borrowers are now looking at FHA loans and ARMs more closely. This is a smart move to try and tackle affordability challenges that still linger, even with rates coming down slightly. It shows that people are being creative with their options to make homeownership more manageable.

What Experts Are Saying: Stability on the Horizon?

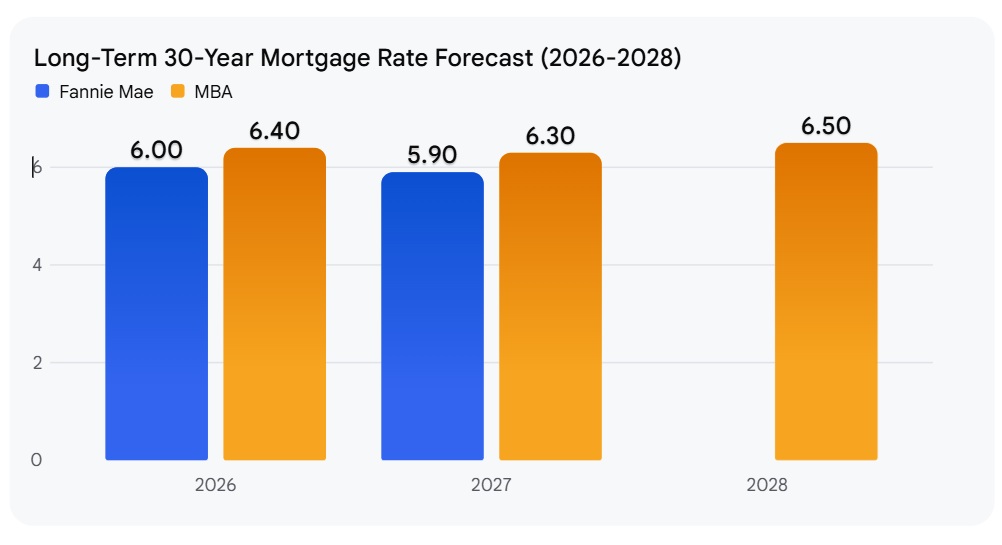

When I look ahead, I want to understand what the trends might be. Forecasters from both Fannie Mae and the MBA are predicting that mortgage rates will likely stabilize around 6% to 6.1% throughout much of 2026. This suggests that the current refinance window, where rates are hovering around the mid-6% range, is a real opportunity.

The idea of a “refinance window” is especially relevant if your current mortgage rate is above 7%. If you locked in a rate around January 2025, for example, you're definitely in a position to save money by refinancing now.

However, we also need to acknowledge the “lock-in effect.” Many of us secured mortgages when rates were historically low, often below 5%. For those homeowners, refinancing at 6.44% doesn't make much sense. They'd need to see rates drop significantly further, perhaps below 5.5%, to make it worthwhile.

Calculating Your Break-Even Point: Is Refinancing Worth It?

This is a crucial step I always emphasize. Refinancing isn't free. There are closing costs, which can typically run anywhere from 2% to 6% of your loan amount. To figure out if refinancing makes sense for you, you need to calculate your “break-even point.”

Here’s how it works:

- Total Closing Costs: Add up all the fees you'll pay to refinance.

- Monthly Savings: Figure out how much your monthly payment will decrease after refinancing.

- Break-Even Point: Divide the Total Closing Costs by your Monthly Savings. The result is the number of months it will take for your savings to cover the costs.

If you plan to stay in your home longer than your break-even point, then refinancing is likely a financially sound decision. For example, if your closing costs are $6,000 and your monthly savings are $200, your break-even point is 30 months (or 2.5 years). If you plan to stay in your home for 5 years or more, it’s a good deal!

My Takeaway for Today

For homeowners who have been waiting for a better opportunity to refinance, today, February 15, 2026, offers a glimmer of hope. The drop in the 30-year fixed refinance rate to 6.44% makes it a more attractive option, especially if your goal is long-term payment stability.

It's always wise to shop around with different lenders, compare offers, and do the math on your specific situation. Weigh the pros and cons of fixed versus adjustable rates and, most importantly, see how refinancing aligns with your personal financial goals. The market is moving, and being informed is your best strategy!

and

Florida’s modern build with strong cash flow vs Missouri’s affordable rental with higher cap rate. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to Our Investment Counselor (No Obligation):

(800) 611-3060

Market forecasts suggest steady demand, making turnkey real estate one of the most reliable paths to passive income and wealth creation.

Norada Real Estate helps investors capitalize on these trends with turnkey rental properties designed for appreciation and consistent cash flow—so you can grow wealth securely while others wait for clarity in the market.

Recommended Read:

- 30-Year Fixed Refinance Rate Trends – February 14, 2026

- Best Time to Refinance Your Mortgage: Expert Insights

- Should You Refinance Your Mortgage Now or Wait Until 2026?

- When You Refinance a Mortgage Do the 30 Years Start Over?

- Should You Refinance as Mortgage Rates Reach Lowest Level in Over a Year?

- Half of Recent Home Buyers Got Mortgage Rates Below 5%

- Mortgage Rates Need to Drop by 2% Before Buying Spree Begins

- Will Mortgage Rates Ever Be 3% Again: Future Outlook

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years