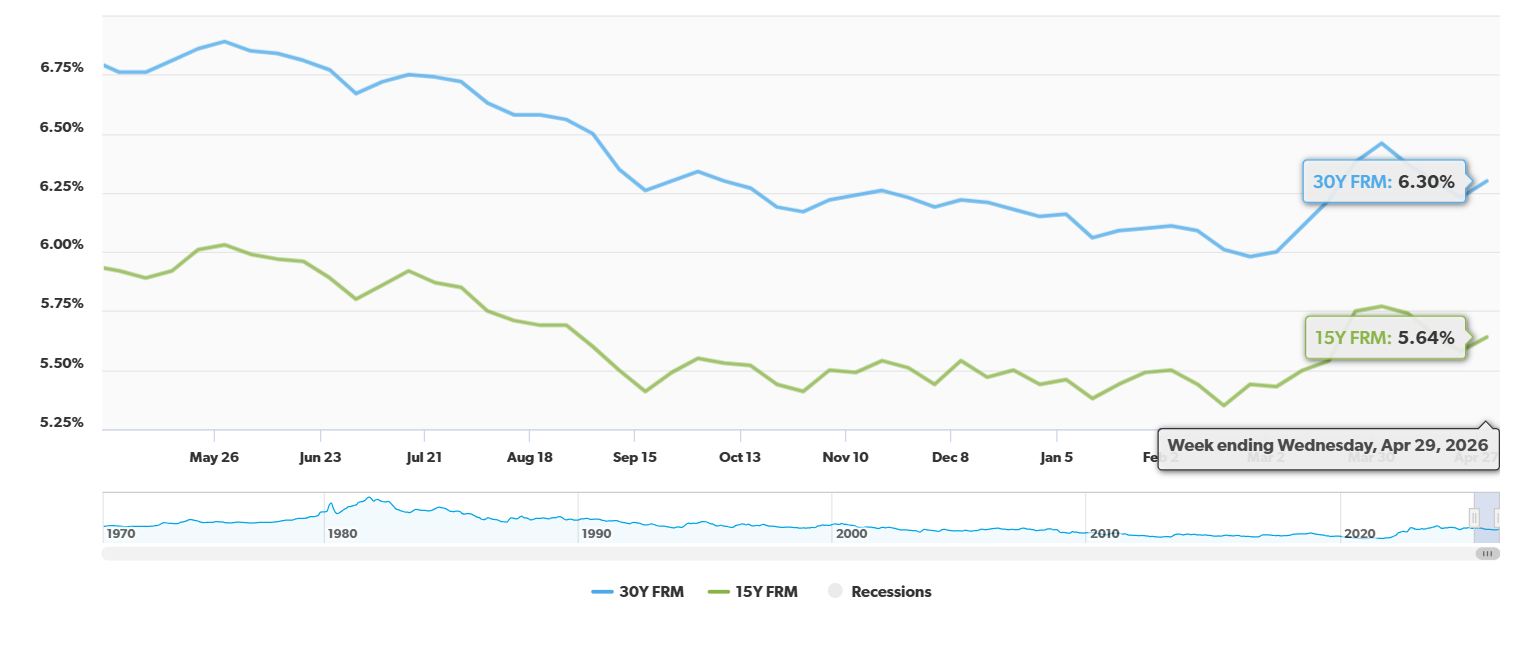

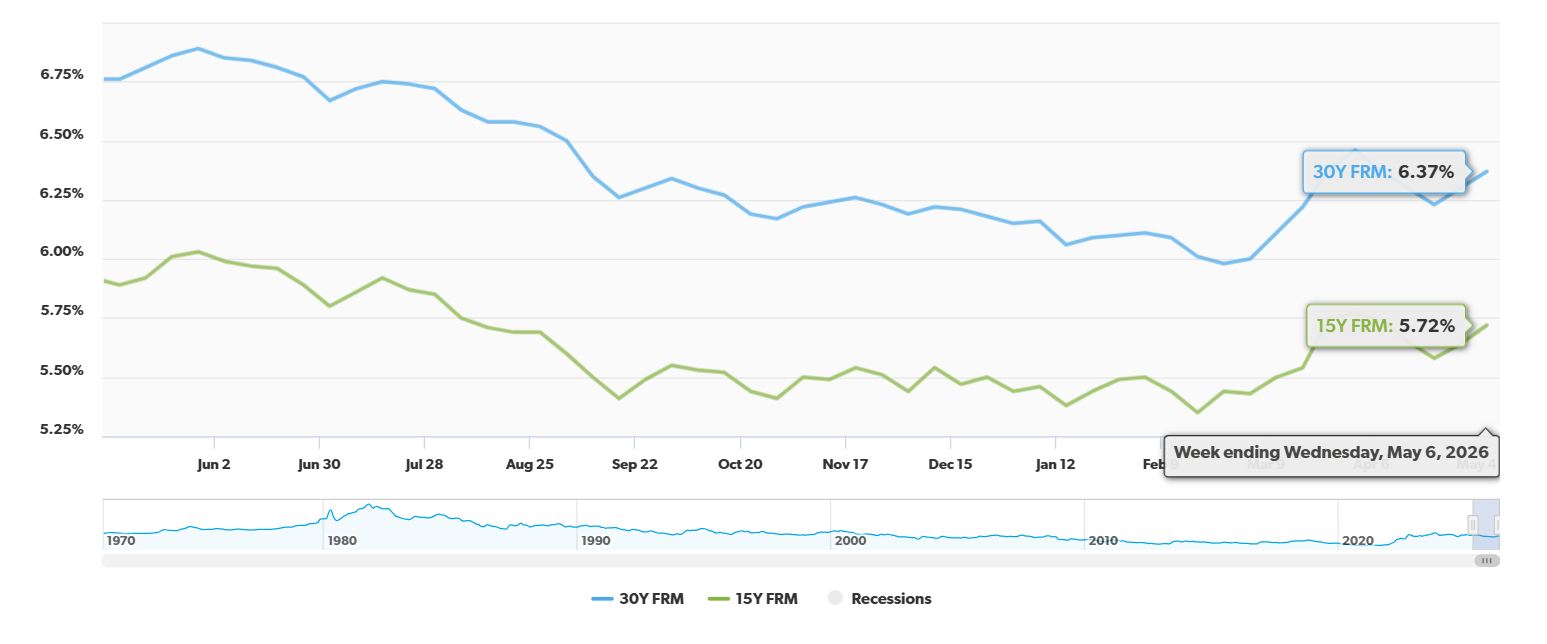

The 30 year fixed mortgage rate has seen a significant drop of 39 basis points compared to this time last year. While there’s been a small bump up in the past week, the overall trend is a welcome one for anyone looking to finance their property. As of May 7, 2026, Freddie Mac reported that the average 30-year fixed-rate mortgage is sitting at 6.37%. Now, that’s up just a touch from last week’s 6.30%, but here’s the kicker: this time last year, that average was a higher 6.76%.

That difference, that 39 basis points, might sound small, but trust me, it can add up to some serious savings and a bigger purchasing power for you. Seeing these rates come down year-over-year is a breath of fresh air. It feels like we’re finally getting a bit of breathing room in what has been a challenging affordability environment.

30‑Year Fixed Mortgage Rate Drops by 39 Basis Points Since Last Year

Breaking Down the Numbers: A Closer Look at the Data

Let’s get a little more specific. Freddie Mac’s Primary Mortgage Market Survey® is a crucial tool for understanding where mortgage rates are heading. Here’s what their latest data, as of May 7, 2026, tells us:

| Mortgage Type | Current Average (05/07/2026) | 1-Week Change | 1-Year Change |

|---|---|---|---|

| 30-Year Fixed | 6.37% | +0.07% | -0.39% |

| 15-Year Fixed | 5.72% | +0.08% | -0.17% |

As you can see, the 30-year fixed-rate mortgage isn't just good compared to last year; it’s also sitting at a monthly average of 6.3% and a 52-week average of 6.38%. The range over the past year has been from 5.98% to 6.89%, so we’re currently in the middle of that, leaning towards the lower end.

The 15-year fixed-rate mortgage is also showing a similar year-over-year improvement, currently at 5.72%, down 17 basis points from 5.89% a year ago. This is also great news, especially for those who can manage a higher monthly payment for a shorter loan term and want to pay off their home faster.

The Real Impact: How a 39 Basis Point Drop Affects Your Wallet

So, what does a 39 basis point drop in the 30 year fixed mortgage rate actually mean for you, a potential homebuyer or refinancer? It’s more significant than you might think.

1. Significant Monthly Savings and Boosted Purchasing Power:

Let’s do some simple math. Imagine you’re looking at a $400,000 mortgage.

- Last Year (at 6.76%): Your monthly principal and interest payment would have been around $2,597.

- This Year (at 6.37%): That payment drops to roughly $2,494.

That’s a saving of about $103 per month, which works out to over $1,200 per year! Now, think about what that extra money can do. It can go towards furnishing your new home, saving for other financial goals, or simply giving you more breathing room in your budget.

Beyond monthly savings, this decrease also effectively increases your purchasing power. For the same monthly payment you could afford last year, you can now potentially afford a home worth about $16,000 more. This could mean the difference between your dream home and just a starter home.

2. Easing the “Lock-In” Effect and Improving Market Sentiment:

I’ve spoken to many homeowners who are hesitant to sell because they’re comfortable with their super-low, pandemic-era mortgage rates. This is what we call the “lock-in” effect. When rates start to trend downwards consistently, it can encourage those homeowners to list their properties, increasing the available inventory for buyers.

This downward trend also signals to buyers who have been on the fence that we might have passed the peak of interest rates. When rates dipped earlier this year, we saw a notable surge in mortgage applications – about 30%! This year-over-year drop suggests a more stable and potentially improving market sentiment for buyers.

3. A Modest Ease in Affordability Pressures:

The good news doesn't stop there. The data from Freddie Mac also points to other positive factors for buyers this spring. Alongside these lower mortgage rates, we’re seeing:

- Increased new-home sales: This indicates demand is picking up.

- Median new-home prices at their lowest level since July 2021: This is a significant development in affordability.

- Higher inventory than in recent years: More homes on the market mean more choices for buyers and less intense bidding wars.

These combined factors are working together to modestly ease affordability pressures for many people looking to buy a home this spring.

Why This Matters to Me (and Likely You Too!)

As someone who has navigated the mortgage process myself and advised others, I know how much these rates influence big life decisions. A 39 basis point drop year-over-year isn't just a number; it's a tangible benefit that can make homeownership more accessible and less financially burdensome.

While the slight weekly increase is something to note, it’s important to focus on the broader, more sustained trend. Geopolitical tensions can cause short-term fluctuations, but the underlying economic conditions that are driving these rates lower, like improved inventory and more stable new-home prices, are very encouraging.

If you’re in the market to buy or refinance, now might be an excellent time to explore your options. It’s always wise to shop around with different lenders and get personalized quotes to see exactly how these rates can benefit you. Don’t just look at the headline numbers; consider your specific financial situation and long-term goals.

The Takeaway

The 30 year fixed mortgage rate drop of 39 basis points year-over-year is a significant positive development for the housing market. It’s offering much-needed relief and improved purchasing power for prospective buyers. While market conditions can always shift, the current trend provides a compelling reason to reconsider your homeownership plans.

VS

Alabama’s new build with solid cap rate vs Georgia’s affordable rental with stronger NOI. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain near 6%, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Will Mortgage Rates Drop to 5% in 2026: Expert Forecast

- How to Get a 3% Mortgage Rate in 2026 With Assumable Mortgages?

- How to Get a 4% Interest Rate on a Mortgage in 2026?

- What Leading Housing Experts Predict for Mortgage Rates in 2026

- Mortgage Rate Predictions for 2026: What Leading Forecasters Expect

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?