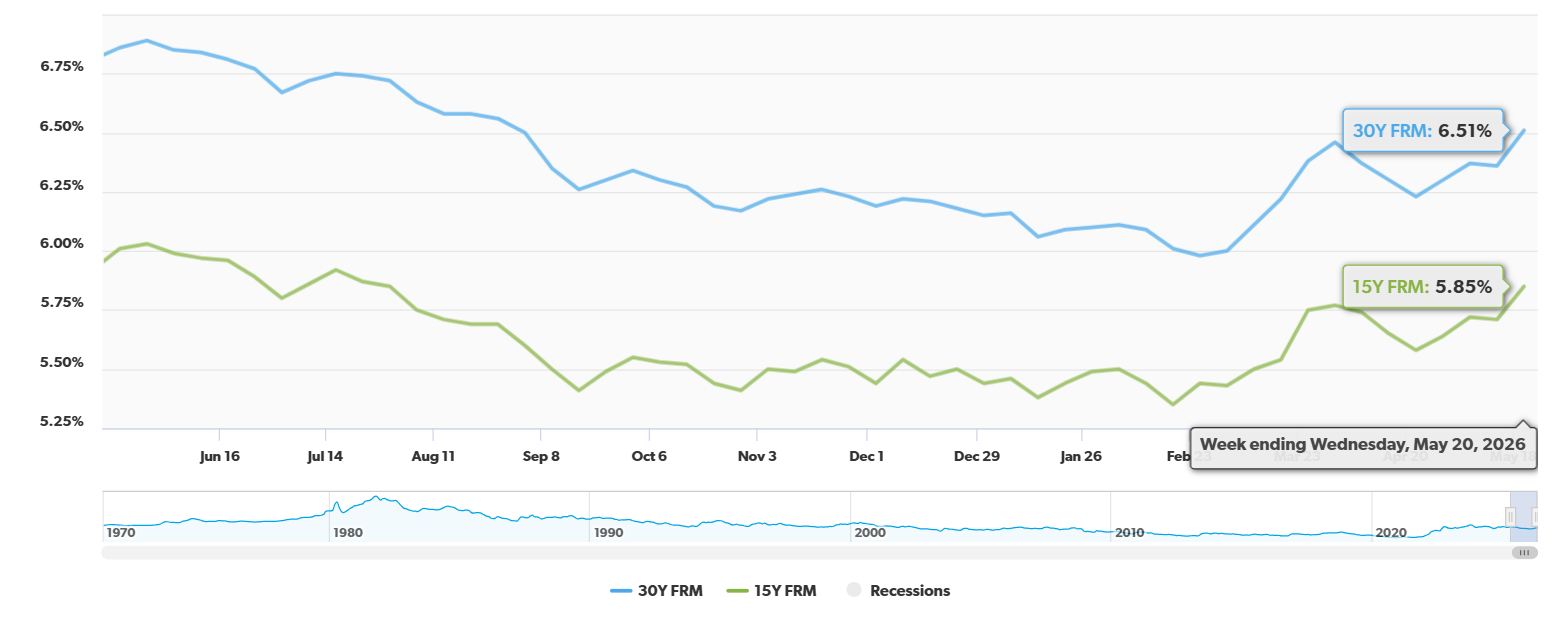

The 30-year fixed-rate mortgage (FRM) averaged 6.51% for the week ending May 21, 2026, marking a 35-basis-point drop from the 6.86% average recorded during the same week in 2025. While long-term borrow costs remain lower than last year, the weekly average actually surged by 15 basis points from the previous week's average of 6.36% amid bond market volatility.

30-Year Fixed Mortgage Rate Drops by 35 Basis Points Year-Over-Year

It’s been a wild ride in the world of mortgage rates, hasn't it? This year, we're seeing a fascinating trend: while the long-term outlook for borrowing costs is more favorable than last year, the short-term picture has been a bit more unpredictable.

Let's break down the numbers from Freddie Mac's Primary Mortgage Market Survey (PMMS):

| Loan Type | Current Week Average (May 21, 2026) | Previous Week Average | Year-Over-Year Change |

|---|---|---|---|

| 30-Year Fixed | 6.51% | 6.36% | -35 basis points (6.86% in 2025) |

| 15-Year Fixed | 5.85% | 5.71% | -16 basis points (6.01% in 2025) |

As you can see, not only has the 30-year fixed rate decreased significantly year-over-year, but the 15-year fixed rate has also seen a reduction, dropping by 16 basis points. This is a positive signal for many buyers.

Why the Weekly Wobble? Understanding Market Dynamics

You might be wondering why, despite the year-over-year decrease, the average rate ticked up by 15 basis points from the previous week. This is where market volatility comes into play. We've been seeing some stubborn inflation data, coupled with ongoing geopolitical events, which tends to make investors nervous. When investors get nervous, they often move their money into safer assets like bonds. This increased demand for bonds drives up their yields, and the yield on the 10-year Treasury note, in particular, has been heading towards a 52-week high. Since mortgage rates are closely tied to Treasury yields, this directly influences the weekly average for mortgages.

It's a complex dance, but the key takeaway for us is that while rates are generally lower than last year, they can move up and down from week to week.

A Glimmer of Hope: Rates Still Below Recent Peaks

While the recent weekly increase might give some pause, it’s crucial to remember the broader context. Even with this uptick, rates are still comfortably below the peaks we saw in late 2023 and 2024. Many of us remember when rates briefly dipped below the 6% mark earlier in February 2026. While we aren't quite there again, the overall trend shows a market that has cooled down from its highest points. This offers a much-needed respite for buyers who may have been priced out during those more expensive periods.

My Take: Patience and Preparedness are Key

From my perspective, this environment calls for a balanced approach. It's easy to get caught up in the day-to-day rate movements, but the year-over-year drop is a more significant indicator of where we stand.

Here's what I believe is most important for you right now:

- Shop Around, Shop Smart: This is probably the most critical piece of advice I can give. The Freddie Mac economists are absolutely right – shopping around and getting multiple quotes from different lenders can save you thousands of dollars over the life of your loan. Don't just go with the first lender you talk to. Compare rates, fees, and loan terms. Even a quarter-percentage-point difference can add up significantly.

- Understand Your Finances: Before you even start looking at homes, get pre-approved for a mortgage. This will give you a clear picture of how much you can afford and will make your offers more competitive. Be prepared to have your finances in order – good credit scores and a solid down payment can help you secure better rates.

- Stay Informed, But Don't Obsess: Keep an eye on mortgage rate trends, but don't let weekly fluctuations dictate your entire home-buying strategy. Focus on your long-term financial goals and what makes sense for your personal situation. If you're ready to buy and find a home you love at a rate that works for you, don't hesitate to act.

The Impact of Lower Rates: What It Means for Buyers

A 35-basis-point drop might sound small, but it can translate into a noticeable difference in your monthly payments and the total interest you pay over 30 years. For example, on a $300,000 loan, a decrease from 6.86% to 6.51% could mean saving roughly $60-$70 per month. Over 30 years, that’s thousands of dollars back in your pocket! This makes homeownership more accessible for a wider range of people.

Looking Ahead: What Could Influence Rates Next?

As we move forward, several factors will continue to shape mortgage rates:

- Inflation Data: This remains a primary driver. If inflation continues to show signs of cooling, it could put downward pressure on interest rates. Conversely, sticky inflation could lead to higher rates.

- Federal Reserve Policy: While the Fed doesn't directly set mortgage rates, its monetary policy decisions, particularly regarding interest rates, have a significant impact on the broader economy and borrowing costs.

- Global Economic Conditions: As we’ve seen, geopolitical events and global economic stability can create market uncertainty, influencing investor behavior and, consequently, mortgage rates.

Conclusion: A Favorable Environment, With Caveats

The year-over-year drop in 30-year fixed mortgage rates is a genuinely positive development for the housing market. It signals a more affordable borrowing environment compared to the previous year, potentially opening doors for many aspiring homeowners. However, the recent weekly increase serves as a reminder that the market is dynamic. My best advice is to stay informed, do your homework by comparing lenders, and be ready to act when the right opportunity arises. The dream of homeownership is within reach, especially with these improved rates.

VS

Out‑of‑State investors can compare Indiana’s affordable rental with higher cap rate vs Florida’s newer A+ property with stability. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain near 6%, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Will Mortgage Rates Drop to 5% in 2026: Expert Forecast

- How to Get a 3% Mortgage Rate in 2026 With Assumable Mortgages?

- How to Get a 4% Interest Rate on a Mortgage in 2026?

- What Leading Housing Experts Predict for Mortgage Rates in 2026

- Mortgage Rate Predictions for 2026: What Leading Forecasters Expect

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?