Mortgage rates have climbed again, with the average 30-year fixed-rate mortgage reaching 6.55% this week, causing many potential homebuyers to pause their search. The latest news from the Freddie Mac Primary Mortgage Market Survey, released today, July 16, 2026, tells a different story. That average 30-year fixed-rate mortgage has nudged up to 6.55%. This small jump, from last week's 6.49%, might not sound like a lot, but when you're talking about buying a house, those tenths of a percent can add up quickly and make a real difference in monthly payments.

Mortgage Rates Hit 6.55%: Buyer Demand Cools Amid Rising Costs

What Does This Mean for You?

For anyone in the market right now, this news likely brings a sigh of disappointment. When mortgage rates go up, the cost of borrowing money to buy a home also goes up. This means your monthly mortgage payment will be higher for the entire time you own the home. It can make it harder to qualify for the loan you need or force you to look at homes that are a bit less expensive. I've seen this play out many times as a long-time observer of the housing market, and it always makes things a bit tougher for buyers.

Breaking Down the Numbers: A Closer Look at the Latest Rates

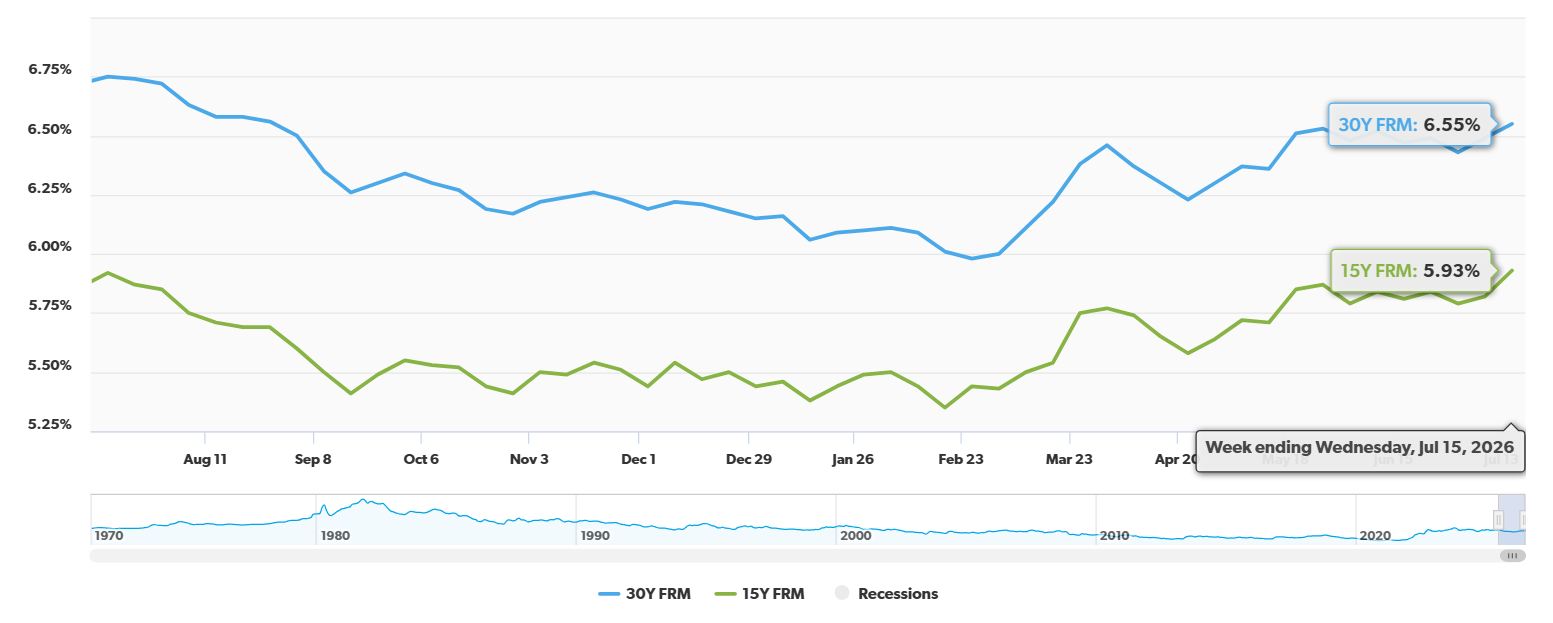

Freddie Mac, a reliable source for mortgage rate information, tracks these averages closely. Here’s what their latest survey tells us:

Table 1: Average Mortgage Rates – July 16, 2026

| Mortgage Type | This Week (July 16, 2026) | Last Week | One Year Ago |

|---|---|---|---|

| 30-Year Fixed-Rate | 6.55% | 6.49% | 6.75% |

| 15-Year Fixed-Rate | 5.93% | 5.82% | 5.92% |

Source: Freddie Mac Primary Mortgage Market Survey, July 16, 2026

You can see that both the popular 30-year fixed-rate and the 15-year fixed-rate have seen increases compared to last week. While the 30-year rate is still a little lower than it was a year ago, the recent upward trend is what's causing concern.

Why Are Rates Going Up?

It's not just random chance that mortgage rates are moving. Several things are at play, and it's helpful to understand them.

- Economic Signals: When the economy is doing well, or there are signs of inflation creeping back, lenders might increase mortgage rates. They are trying to protect themselves against the value of the money they lend decreasing over time. Think of it like this: if prices for everything else are going up, the price of borrowing money might go up too.

- The Federal Reserve: While the Federal Reserve doesn't directly set mortgage rates, their decisions on interest rates and other economic policies have a big impact. When they signal a tougher stance on inflation, it often leads to higher borrowing costs across the board, including for mortgages.

- Investor Demand: Mortgage-backed securities (that's basically bundles of mortgages that investors buy) are influenced by the overall financial markets. If investors are looking for better returns elsewhere, or if there's uncertainty, it can push mortgage rates higher.

Buyer Demand Takes a Hit

As you might expect, when borrowing costs rise, fewer people are rushing to buy homes. The survey notes that purchase application demand has softened recently. This makes perfect sense. If your dream home suddenly becomes hundreds of dollars more expensive each month due to higher interest, you'll probably put your plans on hold and wait to see if things improve. I've talked to so many families who were ready to buy, but the math just didn't work out with the new rates. It’s a tough pill to swallow.

But There's a Silver Lining?

Even with these rising rates, the Freddie Mac survey hints at some positive shifts that could eventually help buyers.

- More Homes on the Market: The good news is that housing inventory continues to rise. This means there are more homes available for sale, giving buyers more choices and potentially less competition. When there are more homes, sellers might be more willing to negotiate on price, which can help offset some of the increased borrowing costs.

- Affordability is Improving (Slowly): Despite the weekly rate bump, Freddie Mac’s Chief Economist, Sam Khater, mentioned that housing affordability is more favorable and housing inventory trends are modestly improving. This sounds a bit contradictory, doesn't it? But what it means is that while the cost of borrowing is up, the underlying conditions for buying might still be getting better. For example, if home prices themselves start to stabilize or slightly decrease, and there are more homes to choose from, it can make the overall process of buying more manageable, even with a higher interest rate.

What I'm Seeing and Thinking

From my perspective, the housing market is in a bit of a tug-of-war. On one side, you have the rising cost of borrowing, which cools off demand. On the other, you have a slowly increasing supply of homes, which should theoretically help buyers.

It’s a tricky time for both buyers and sellers. Buyers need to be realistic about what they can afford. It might mean adjusting expectations, looking at slightly smaller homes, or considering different neighborhoods. For sellers, it means understanding that buyers are more price-sensitive now. Overpriced homes will likely sit on the market longer.

I believe that the market is naturally trying to find a balance. Rates might fluctuate, and home prices will respond to how many people are buying and selling. The key for buyers right now is to be patient, do their homework, and work with trusted advisors to understand their options. Don't get discouraged by a single week's rate increase. Look at the bigger picture and the long-term trends.

Looking Ahead

Will mortgage rates keep going up? It's hard to say for sure. The economy is always changing, and unexpected events can shake things up. However, for now, it seems we need to get used to rates being in this general range. This might mean that the intense bidding wars we saw a while back will become less common.

For those still set on buying, getting pre-approved for a mortgage is more important than ever. This will give you a clear picture of how much you can borrow at the current rates and help you avoid any surprises when you find the perfect home.

VS

Out‑of‑State investors can compare Tennessee’s newer rental with higher NOI vs Florida’s A+ property with strong yield. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain near 6%, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Will Mortgage Rates Drop to 5% in 2026: Expert Forecast

- How to Get a 3% Mortgage Rate in 2026 With Assumable Mortgages?

- How to Get a 4% Interest Rate on a Mortgage in 2026?

- What Leading Housing Experts Predict for Mortgage Rates in 2026

- Mortgage Rate Predictions for 2026: What Leading Forecasters Expect

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?