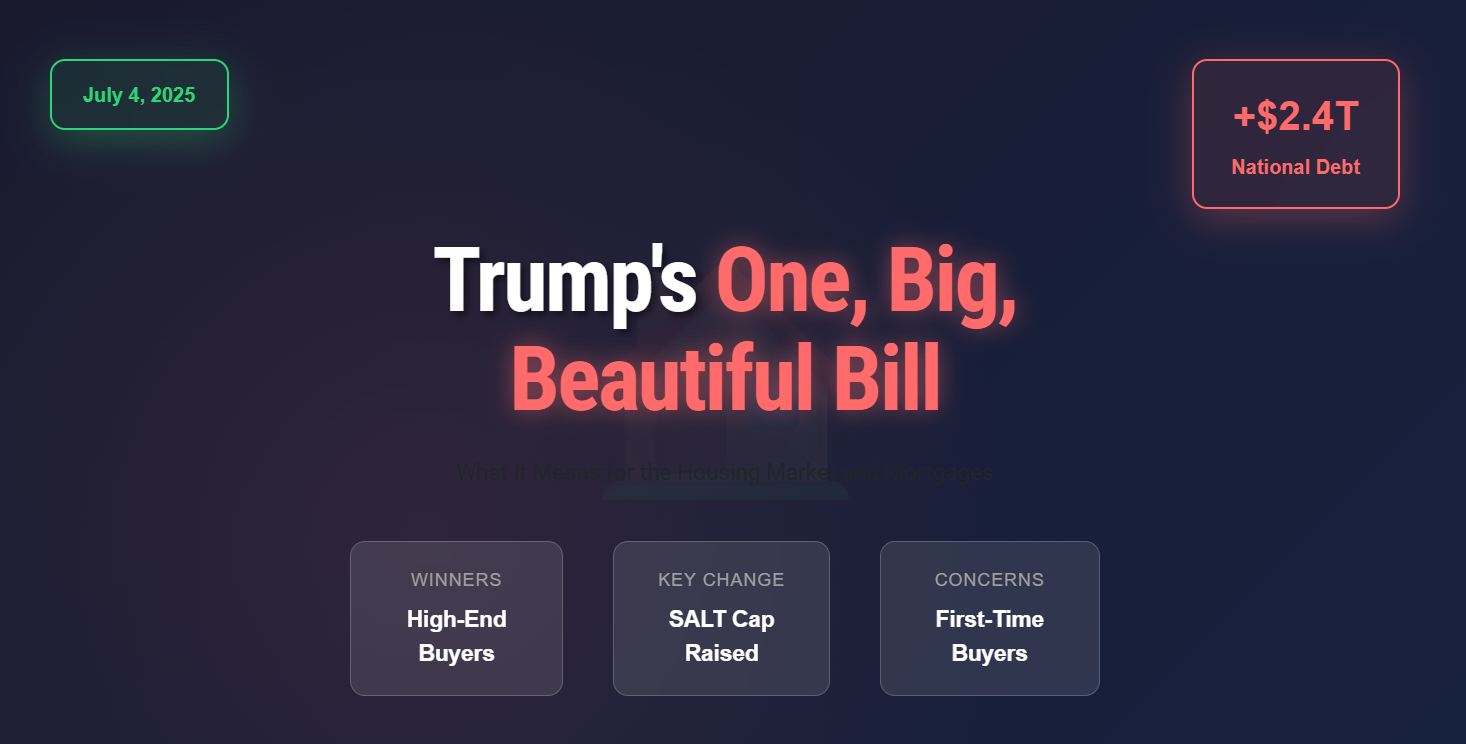

Will Trump's “Big Beautiful Bill” truly reshape the housing market? The answer is complex. Signed into law on July 4, 2025, this legislation brings a mix of tax cuts and new policies that could have significant impacts on homebuyers, renters, investors, and the mortgage industry. While some provisions aim to boost affordable housing and provide tax relief, others raise concerns about affordability and supply. Let's dig deeper into what this bill actually does and who benefits (and who doesn't).

Is One Big Beautiful Bill a Game-Changer for the Housing Market and Mortgages?

What exactly IS the “Big Beautiful Bill?”

This bill is a broad budget and tax package that touches upon various aspects of American life. But for our purposes, we need to focus on its implications for housing and mortgages. Here are some key takeaways:

- Low-Income Housing Tax Credit (LIHTC) Expansion: This is probably the most impactful aspect of the bill for affordable housing. It increases the 9% LIHTC allocation and reduces the bond financing requirement for 4% LIHTCs. This could mean significantly more affordable rental homes in the coming years.

- State and Local Tax (SALT) Deduction Increase: Homeowners in states with high property taxes may catch a break here. The SALT deduction cap is bumped up, potentially saving families money.

- Permanent Mortgage Insurance Deduction: A bit of good news for those with smaller down payments. This makes deductions for private mortgage insurance (PMI) permanent.

- Permanent Mortgage Interest Deduction Cap: Setting a secure upper limit for mortgage interest deductions at \$750,000 offers certainty for the housing market.

- Termination of Energy Efficiency Credits: This part isn't so great. Eliminating credits for energy-efficient home improvements could ironically drive up the cost of constructing new houses.

- Block on Rent-Setting Algorithm Regulation: In my opinion, this is a real problem. Preventing states from regulating AI-based rent-setting systems could lead to unchecked rent increases.

These are the core components. Before we proceed, I've compiled all this key information in table format.

| Provision | Impact |

|---|---|

| LIHTC Expansion | Increased affordable rental housing supply |

| SALT Deduction Increase | Potential tax savings for homeowners in high-tax states |

| Permanent Mortgage Insurance Deduction | Reduced cost of low-downpayment loans |

| Permanent Mortgage Interest Deduction Cap | Stability for borrowers and lenders |

| Termination of Energy Efficiency Credits | Increased construction costs |

| Block on Rent-Setting Algorithm Regulation | Potential for higher rents |

Now, let's dive into how these provisions affect different groups of people.

Who wins (and who loses) in this equation?

It's not a simple question. The “Big Beautiful Bill” has different implications for different segments of the population, and that's what we're going to discuss here in detail.

High-End Buyers and Investors: A Reason to Smile?

In my opinion, this is where the bill provides the clearest benefits. Wealthier homebuyers and real estate investors, especially in high-tax, high-cost states, have reason to be optimistic.

- SALT Deduction Increase: The increase in the SALT deduction cap is a big deal for homeowners in places like New York, California, and New Jersey. They can now deduct more of their state and local taxes, potentially saving thousands of dollars per year.

- QBI Deduction and Bonus Depreciation: These are tax breaks specifically for real estate investors. They allow them to deduct a larger portion of their business income and depreciate renovation costs more quickly, encouraging investment in rental properties and commercial real estate.

- Retention of Section 1031 Exchanges: Allows tax-deferred property swaps for investors.

For example, if you live in a state where your property taxes alone exceed $10,000 (and many do!), this increase in the SALT deduction will directly translate to tax savings. Plus, those incentives for real estate investment are designed to stimulate activity in the market.

Lower-Income Renters and First-Time Buyers: A More Uncertain Future?

This is where things get complicated. While the bill does have some positives for this group, the net effect might not be as beneficial as hoped.

- LIHTC Expansion: This is undeniably a good thing. More affordable rental housing is desperately needed in this country, and the LIHTC expansion could help ease cost burdens for low-income tenants. However, keep in mind that it will take time for these new units to be built and become available.

- Social Program Cuts: Here's the rub. The bill also includes significant cuts to social programs like Medicaid and SNAP, potentially straining low-income households and making it more difficult to afford rent or save for a down payment.

- No New Down Payment Assistance: The absence of new federal down payment assistance programs means that first-time homebuyers will still need to rely on state and local programs, which can be difficult to access or insufficient.

In my view, the LIHTC expansion is a step forward, but it's not enough to offset the potential negative effects of the social program cuts. The reality is that many low-income renters and first-time buyers may not feel any immediate relief from this bill.

Housing Supply: Will It Actually Increase?

The U.S. has been facing a serious housing shortage for years now, and any policy that aims to address this issue is worth examining closely. The “Big Beautiful Bill” tries to tackle this problem in a couple of ways:

- LIHTC Expansion: This encourages the construction of more affordable rental units.

- Opportunity Zone Incentives: Which are intended to stimulate investments in underserved communities. However, it depends on the execution.

- Termination of Energy Efficiency Credits: On the downside, eliminating these credits could raise construction costs, making it more expensive to build new homes.

Unfortunately, tariffs on imported construction materials may further slow building.

The Mortgage Industry: A Modest Boost?

The mortgage industry stands to benefit from a few key provisions in the bill:

- Permanent Mortgage Insurance Deduction: This reduces the effective cost of low-down-payment loans, which benefits both borrowers and lenders.

- Permanent Mortgage Interest Deduction Cap: This provides planning certainty for borrowers and lenders, particularly in high-cost markets. As I said, the certainty this provision allows is greatly useful.

While these measures might encourage more first-time buyers to enter the market, the lack of new federal down payment assistance limits the bill's overall impact. Some feel that a more targeted approach would be more effective.

Rent-Setting Algorithms – A Potential Affordability Crisis?

This is a critical area to watch closely. If this provision stands, it could exacerbate the affordability crisis for renters, particularly in high-cost markets.

Regulating rent-setting algorithms is a potential issue that worries me a lot. This prevents states from regulating AI models used for determining rental prices, a move that 40 state attorneys general oppose. Their concern is that this could lead to higher rents and reduced affordability, especially in already expensive areas.

Regional Variations: A Patchwork of Impacts

It's important to remember that the impact of this bill will vary significantly depending on where you live.

- High-Tax States: Residents of states like New York, New Jersey, Massachusetts, Illinois, and California will likely see the most immediate benefits from the increased SALT deduction cap, making homeownership more attractive for some.

- Lower-Tax States: Areas with lower tax burdens and looser housing supply, such as parts of Texas or the Midwest, may experience less direct benefit from the bill.

- LIHTC Impact: The supply-side effects of the LIHTC expansion will take time to materialize, meaning that high-cost cities like San Francisco or New York are unlikely to see immediate relief from affordability pressures.

In other words, this bill isn't a one-size-fits-all solution. Some regions will benefit more than others, and the long-term effects are still uncertain.

The Broader Economic Context: An Uphill Battle?

It's crucial to consider the “Big Beautiful Bill” within the context of the broader economic challenges facing the U.S. housing market.

- Housing Shortage: As I pointed out earlier, we're still facing a significant shortage of homes.

- High Mortgage Rates: Mortgage rates remain elevated, making it more expensive to buy a home.

- Elevated Prices: Home prices are still high in many markets, putting homeownership out of reach for many Americans.

- Addition to National Debt: The bill's \$2.4 trillion addition to the national debt over the next decade could push interest rates higher, increasing borrowing costs for homebuilders and homebuyers.

Proposed budget cuts to housing and community development programs could further strain affordability.

In conclusion, while the “Big Beautiful Bill” offers some potential benefits for the U.S. housing market, it's not a magic bullet. High-end buyers and investors in high-tax states stand to gain the most, while lower-income renters and first-time buyers may see limited immediate support.

The LIHTC expansion could lead to long-term growth in affordable housing, but broader economic pressures and regional variations will continue to shape the market. Personally, I believe we need a more comprehensive approach to address the housing affordability crisis, one that combines targeted tax relief, increased housing supply, and robust social safety nets.

Leverage the “BBBA” for Smarter Real Estate Moves

If the “Big Beautiful Bill Act” reshapes housing policy and mortgage access, savvy investors have a unique opportunity.

Norada helps you navigate the changing landscape with turnkey rental properties that benefit from strong financing options and market stability.

HOT NEW LISTINGS JUST ADDED!

Talk to a Norada investment counselor today (No Obligation):

(800) 611-3060

Read More:

- Trump’s Section 8 Housing Cuts: Will Millions Face Homelessness?

- Top Reasons Behind the End of the Trump-Musk Alliance in 2025

- What is Trump's Plan for Privatizing Fannie Mae and Freddie Mac?

- Elon Musk's $10,000 Homes: A Game Changer for the Housing Market?

- Elon Musk Calls for Major Reforms at the U.S. Federal Reserve

- Can Elon Musk Revolutionize Affordable Housing for Americans?

- Emergency Price Relief on Housing: What Does Trump's Order Mean?

- Trump's Inaugural Speech: Bold Plans on Border, Economy, and More

- What Happens to Kamala Harris' Proposal of $25,000 Homebuyer Assistance Now?

- Housing Market Predictions for 2025 if “Trump” Wins Election

- 10 Housing Market Predictions Under Trump for the Next 4 Years

- Will Donald Trump's Victory Reshape the Housing Market in 2025?

- Trump vs Harris: Housing Market Predictions Post-Election

- 10 Housing Market Predictions Under Trump for the Next 4 Years

- Will Donald Trump's Victory Reshape the Housing Market in 2025?