It's July 1, 2026, and if you're thinking about buying a home or refinancing, you're probably wondering what's happening with mortgage rates. Well, I've got some news for you: today's mortgage rates have settled into the mid-6% range. While it might not be the super-low rates we saw a few years back, there are still smart ways to navigate the market.

Today's Mortgage Rates, July 1: 15‑Year Fixed Holds at 5.71% With ARMs Rising

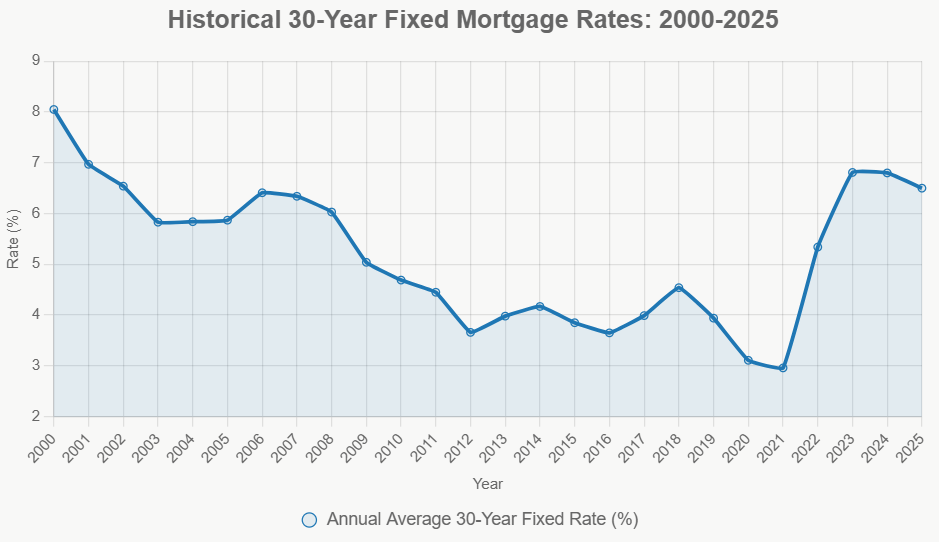

As a homeowner and someone who keeps a close eye on the housing market, I know how important it is to understand where rates are headed. It feels like just yesterday we were talking about rates in the 3% and 4% range, but those days are likely behind us for now. The good news is that things have stabilized a bit, and while they're not dropping dramatically, they aren't skyrocketing either.

What the Numbers Say Today

According to the latest data from Zillow, here's a snapshot of what mortgage rates look like as of July 1, 2026:

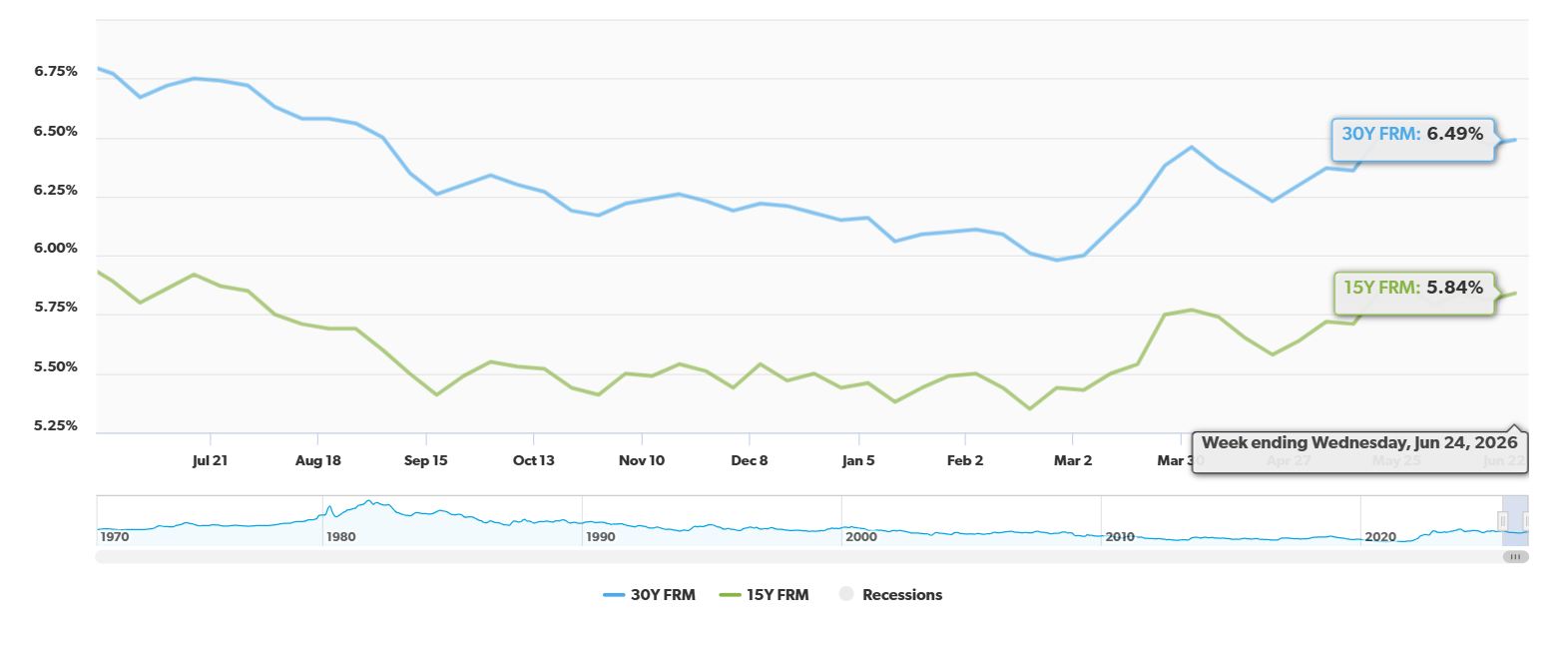

- 30-year fixed: 6.26% (This is up 7 basis points from yesterday)

- 15-year fixed: 5.71% (This is up 1 basis point from yesterday)

- 5/1 ARM: 6.17% (This is up 11 basis points from yesterday)

It's also worth noting that broader market averages show the benchmark 30-year fixed mortgage rate is sitting around 6.47% to 6.49%. This tells me that while Zillow's specific numbers are a good guide, shopping around with different lenders is even more crucial right now.

Why Are Rates Here? A Look Under the Hood

So, why aren't rates dipping lower? A couple of big factors are at play.

- Inflation is Still a Concern: Consumer inflation has been sticking around, hitting 4.2% in May. This is a key reason why the Federal Reserve is holding steady on its interest rate decisions. They want to see inflation cool down consistently toward their 2% target before they even consider lowering rates.

- The Fed's Pause: The Federal Open Market Committee (FOMC) has kept the federal funds rate paused at 3.50%–3.75%. Honestly, I don't see them making any big moves on rates until inflation shows a clearer downward trend.

- Oil Prices to the Rescue (Sort Of): On a brighter note, falling oil prices, down to around $71 a barrel, are actually helping to ease pressure on the bond markets. This is a good thing because it's preventing mortgage rates from jumping back up into the dreaded 7% territory.

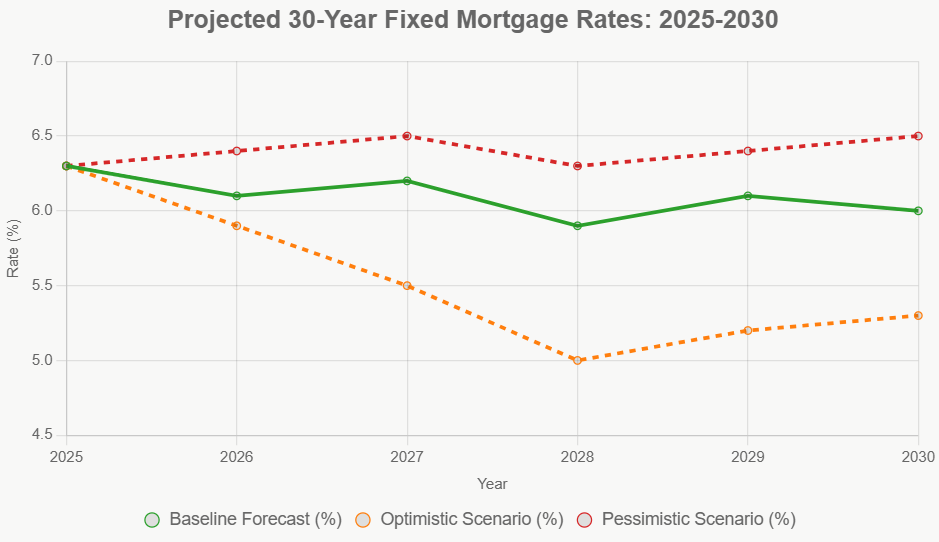

Where Are We Headed? My Crystal Ball (and the Experts')

Looking ahead, most experts agree that we're in for a period of stable, albeit somewhat volatile, rates this summer. Think of it as a plateau.

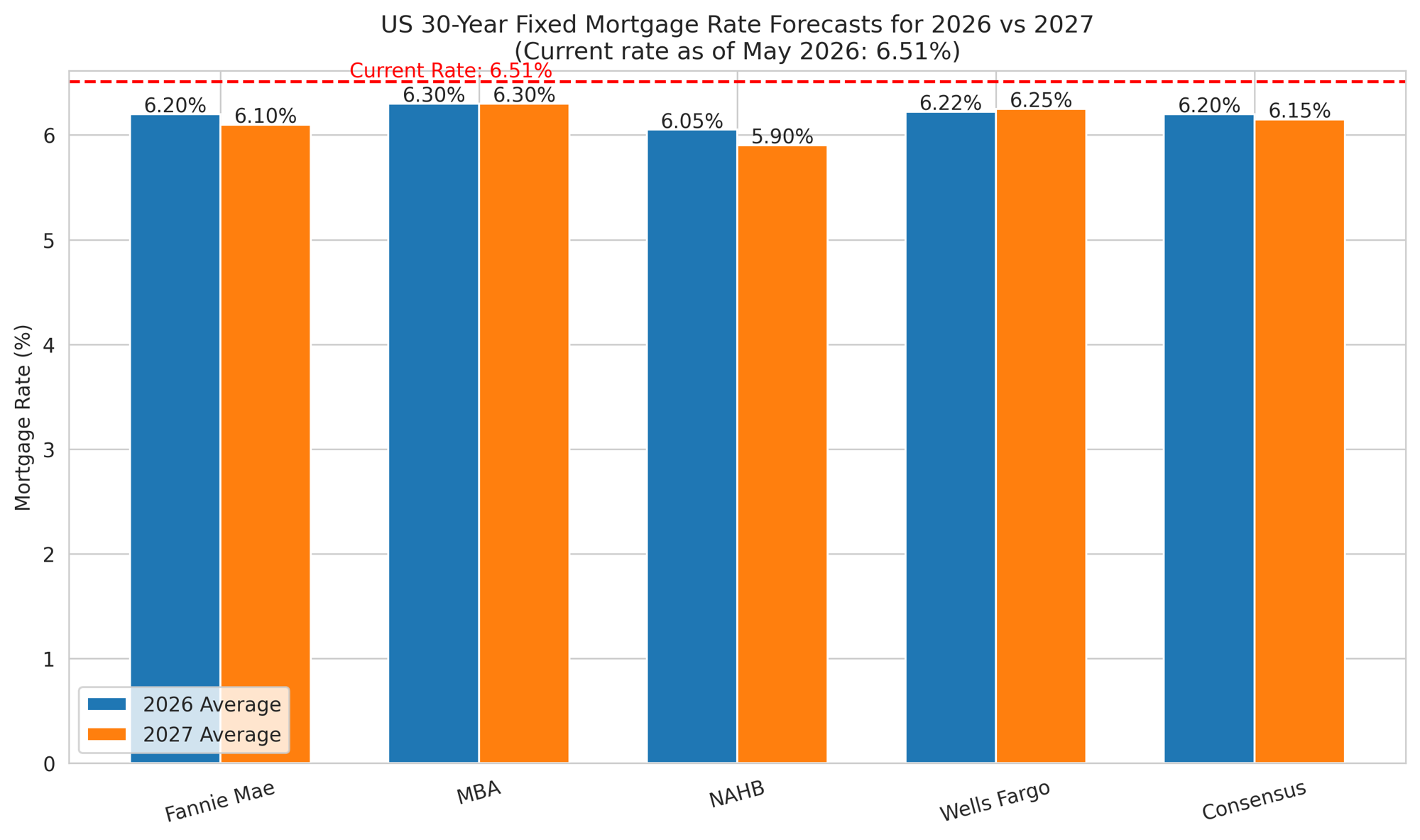

- Summer Outlook: Major housing authorities like Fannie Mae and the Mortgage Bankers Association are predicting that rates will likely finish 2026 somewhere between 6.3% and 6.4%.

- The 6% Threshold: Don't expect rates to consistently drop below 6% anytime soon. Most economists believe that won't happen until sometime in mid-2027.

What Does This Mean for You? Taking Action Today

Knowing all this, what's the best strategy for you right now? Here’s what I’d recommend:

1. Lock Your Rate Early:

If you’ve found a home you love, don't wait around. Secure a rate lock as soon as possible. Upcoming economic reports, like the Consumer Price Index (CPI) on July 15th and the Personal Consumption Expenditures (PCE) report on July 31st, can cause sudden jumps in rates.

2. Let Go of the “3% Trap”:

I know it's tempting to hold out for those incredibly low rates from the pandemic era, but those days are gone. Housing experts are unanimous: those low rates are not coming back anytime soon. It's more practical to focus on what's possible now.

3. Marry the House, Date the Rate:

This is a phrase I really believe in. Focus on finding a home that truly fits your needs and your monthly budget. Remember, you can always refinance your mortgage later if rates drop significantly. It’s often easier to find a great house than to find a great house at a rock-bottom rate.

4. Shop Around, Shop Around, Shop Around:

This is non-negotiable. Lenders' pricing can vary quite a bit, especially right now. Use platforms like Bankrate or Zillow Home Loans to compare quotes from at least three different lenders. You could easily save 25 to 50 basis points just by doing this, which adds up to significant savings over the life of your loan.

5. Consider Adjustable-Rate Mortgages (ARMs):

If you're planning to move or refinance in the next 5-7 years, an Adjustable-Rate Mortgage (ARM) could be a smart choice. For example, a 7/1 ARM is currently averaging about 60 basis points lower than a 30-year fixed. This means lower monthly payments initially, which can be a big help.

Mortgage Rate Snapshot – July 1, 2026

Here’s a quick summary of the rates we're seeing today, based on Zillow data:

| Loan Type | Interest Rate |

|---|---|

| 30-year fixed | 6.26% |

| 15-year fixed | 5.71% |

| 5/1 ARM | 6.17% |

Note: Data is based on Zillow's reported rates for July 1, 2026.

My Takeaway

While today's mortgage rates aren't as low as they once were, the market is presenting opportunities. The key is to be informed, act strategically, and remember that your perfect home might be within reach if you approach it with the right plan. Don't let the “what if” of lower rates stop you from making a move that could be right for you today.

VS

Out‑of‑State investors can compare Tennessee’s newer rental with higher NOI vs Florida’s A+ property with strong yield. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?