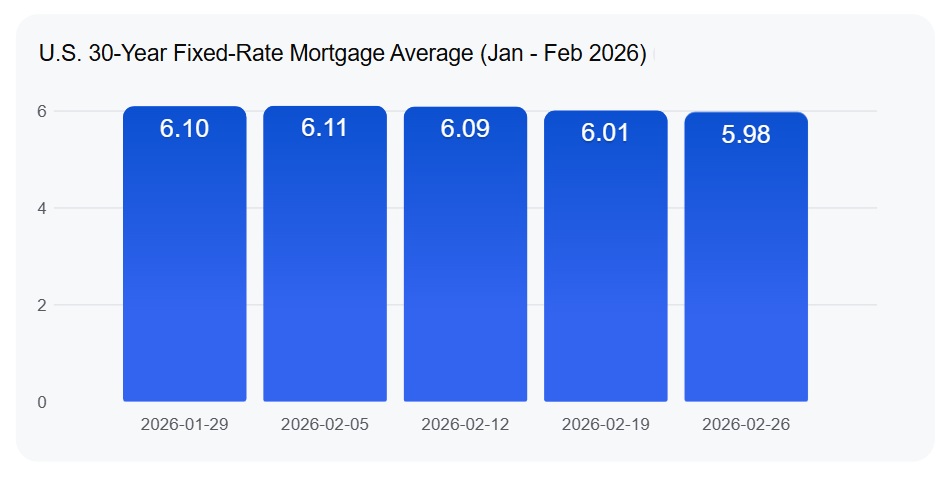

This is huge news for anyone dreaming of homeownership or looking to refinance their mortgage. The 30-year fixed mortgage rate has officially dipped below 6%, settling at a fantastic 5.98%, according to the latest, highly anticipated report from Freddie Mac. This milestone, the first time we’ve seen rates in the 5% range in about three and a half years, is more than just a number; it's a significant shift that could dramatically improve affordability and breathe new life into the housing market.

30-Year Fixed Mortgage Rate Drops Steeply by 78 Basis Points

While this week's change might seem modest, the year-over-year drop of a stunning 78 basis points represents a truly substantial improvement for borrowers. A drop like this isn't just a blip.

It feels like a turning point. After the rollercoaster of rising rates we’ve experienced, seeing the primary 30-year fixed mortgage rate fall this much represents a substantial win for potential and current homeowners. It’s like finally getting a bit of breathing room after holding your breath for too long. This decrease opens up doors that might have felt slammed shut just a few months ago.

A Significant Swing in Borrowing Costs

Let's break down what these numbers from Freddie Mac's Primary Mortgage Market Survey® actually mean for you.

The headline number, 5.98% for the 30-year fixed-rate mortgage, is significant. It's not just a little bit lower than last week; it's the lowest it’s been in a long time. While the weekly change from last week was a tiny decrease of just 3 basis points, the real story is in the big picture. Compared to this time last year, when rates were hovering much higher, we’ve seen a dramatic decrease of 78 basis points. To put that into perspective, that's nearly a full percentage point drop in your borrowing cost.

Think about it: last year, the average rate was closer to 6.76%. That means the cost of borrowing the same amount of money has gone down considerably. This doesn't just make buying a new home more accessible; it also makes refinancing your existing mortgage to a lower rate incredibly attractive.

The 15-year fixed mortgage rate also offers good news, although with a slightly different weekly trend. It's currently at 5.44%. While it ticked up a bit this week by 9 basis points, it's still a full 50 basis points lower than it was a year ago. This reinforces the overall trend: despite minor weekly ups and downs, the general direction for mortgage rates has been downward over the past year.

Decoding the Impact: What the Rate Drop Means for Your Wallet

This isn't just about numbers on a screen; it's about tangible savings and increased possibilities. Let's look at a quick comparison:

| Loan Type | Current Rate (Feb 26, 2026) | Rate Last Year (Approx.) | Yearly Change | Potential Monthly Savings (on $400k Loan) |

|---|---|---|---|---|

| 30-Year Fixed | 5.98% | 6.76% | -78 bps (-0.78%) | Approximately $135 per month |

| 15-Year Fixed | 5.44% | 5.94% | -50 bps (-0.50%) | Approximately $70 per month |

Note: Monthly savings are estimates based on a $400,000 loan amount and may vary based on loan terms and specific lender rates.

When you're talking about a 78 basis point drop on a 30-year mortgage, the savings add up incredibly quickly over the life of the loan. For a $400,000 mortgage, a difference of 0.78% can mean saving thousands, if not tens of thousands, of dollars. The thought of saving $135 more each month at 5.98% compared to, say, 6.5% is enough to make a big difference for families budgeting for a new home. It’s this kind of substantial shift that can make or break a home purchase for many people.

Why This “5-Handle” Matters So Much

Here's why this rate falling below 6% is so important. It's not just a little bit lower; it's a psychological benchmark that many buyers and sellers have been waiting for.

- The “5-Handle” Effect: For years, we've seen rates climb into the 6% and even 7% range. Seeing a rate with a “5” in front of it, like 5.98%, has a powerful psychological impact. It makes the idea of buying or refinancing feel much more achievable for people who might have been priced out or hesitant. I've seen firsthand how a round number like this can encourage people to finally make a move.

- Unlocking the Market: Many homeowners who got mortgages during the super-low rate environment of the pandemic have been hesitant to sell. They might have a 3% rate and are understandably reluctant to trade it for a 7% rate. However, as rates drop closer to the 6% mark, that difference becomes smaller, potentially freeing up more homes for sale. This could lead to a much-needed increase in housing inventory.

- Perfect Timing for Spring: This rate drop comes at an ideal time, just as we head into the traditionally busy spring homebuying season. More buyers looking and potentially more homes coming onto the market? That’s a recipe for a more active and vibrant real estate market. I'm expecting this to be a really strong spring for home sales.

- Boosting Purchasing Power: Experts estimate that a drop of this magnitude can significantly increase a household's purchasing power. For the average U.S. household, this could mean they can afford a significantly more expensive home than they could a year ago. The National Association of REALTORS® suggests that over a million more households could qualify for a mortgage nationally. This is incredibly empowering for first-time buyers.

- Refinancing Frenzy: For those who already own homes and perhaps bought or refinanced at higher rates in the past year or two, now is the time to seriously look at refinancing. Those who bought at rates of 7% or higher could see substantial savings by refinancing to this new 5.98% rate. We've already seen an uptick in refinance activity, and this news will likely push that even higher.

My Take: A Welcome Shift for Buyers and the Economy

As someone who works with people navigating the mortgage process, I find this news incredibly encouraging. The Federal Reserve's recent rate cuts and government initiatives to support the housing market are clearly having a positive effect. Seeing the 30-year fixed mortgage rate fall below 6% is a clear sign that the market is responding, and more importantly, that borrowers are getting a break.

This isn't just about getting a slightly better deal; it's about restoring balance and accessibility to the housing market. It’s about giving families the chance to achieve their homeownership dreams and helping existing homeowners improve their financial situations. If you've been on the fence about buying or refinancing, I strongly suggest you talk to your lender about what these new rates could mean for you. The savings are real, and the opportunity is here.

And

Alabama’s newer A- rental vs Tennessee’s larger property with higher NOI. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Will Mortgage Rates Drop to 5% in 2026: Expert Forecast

- How to Get a 3% Mortgage Rate in 2026 With Assumable Mortgages?

- How to Get a 4% Interest Rate on a Mortgage in 2026?

- What Leading Housing Experts Predict for Mortgage Rates in 2026

- Mortgage Rate Predictions for 2026: What Leading Forecasters Expect

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?