If you're like most people dreaming of owning a home, mortgage rates are probably on your mind. The good news is that mortgage rates have dropped to their lowest level since April, potentially helping buyers save thousands of dollars. The 30-year fixed-rate mortgage down to 6.63% as of August 7, 2025. What does this mean for you, whether you are in the market for buying homes or refinancing your current mortgage? Let's dive in and explore.

Mortgage Rates Drop to Lowest Level, Helping Buyers Save Thousands

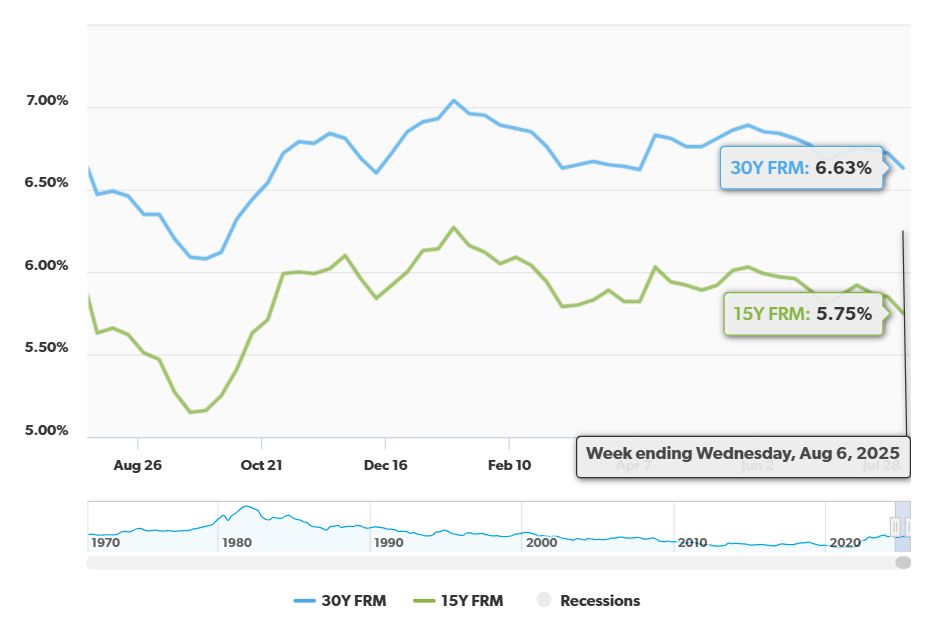

The Current Rate Environment: A Breath of Fresh Air

For quite some time, prospective homebuyers have been grappling with relatively high mortgage rates. After a period of aggressive rate hikes by the Federal Reserve to combat rising inflation, we're finally seeing rates ease a bit. It's like a small weight being lifted, especially if you've been waiting on the sidelines for rates to become more favorable. As per Freddie Mac, the 30-year fixed-rate mortgage averaged 6.63% as of August 7, 2025.

- This is a decrease of 0.09 percentage points from the previous week.

- While still higher than a year ago (6.47%), it's a welcome dip from recent highs.

- The 15-year fixed-rate mortgage also saw a drop, averaging 5.75%.

How Lower Rates Translate to Real Savings

A drop of even a fraction of a percentage point can make a significant difference in your monthly payment and the total amount you pay over the life of your loan. Let's look at a simple example:

Imagine you're buying a home for $300,000.

- At a rate of 7%, your monthly principal and interest payment would be roughly $1,996.

- If you secure a rate of 6.63%, your monthly payment would drop to approximately $1,922.

That $74 a month in savings might seem small, but over 30 years, it adds up to savings of over $26,640! And that figure doesn't even factor in the other costs of owning such as property taxes and home insurance. By diligently checking mortgage rates, finding the best mortgage is easier than ever. It pays to shop around. Freddie Mac research indicates that buyers can save thousands by getting quotes from multiple lenders. It's really that simple; don't settle for the first rate you see!

Why Are Rates Dropping?

The Federal Reserve plays a huge role in influencing mortgage rates through its monetary policy. Here's the backstory:

- Pandemic Response: The Fed initially kept rates low to stimulate the economy during the pandemic.

- Inflation Fight: As inflation surged, the Fed aggressively raised rates from March 2022 to July 2023, pushing mortgage rates upwards.

- The Pause and Potential Pivot: After holding rates steady for 14 months, the Fed cut rates three times in late 2024 by 1 percentage point to 4.25%-4.5%.

- 2025 – A Year of Uncertainty: As of July 2025, the Fed has held rates steady for five consecutive meetings.

Right now, the Fed is grappling with mixed economic signals: still-high inflation and a slowing economy. The expectation is that the Fed may cut rates later in 2025, but the timing and magnitude of those cuts are uncertain.

Related Topics:

Mortgage Rates Predictions for the Next 6 Months: August to December 2025

Mortgage Rates Predictions for the Next 3 Months: August to October 2025

The Fed's Next Moves: What to Watch For

All eyes are on the Fed's upcoming meetings, especially the one in September 16-17. The market is currently pricing in under 50% odds of a rate cut in September. But, the next realistic opportunity for a cut would be in December.

Here's a quick timeline of potential Fed actions:

| Meeting Date | Potential Action |

|---|---|

| September 16-17, 2025 | Possible rate cut (less than 50/50 odds) |

| December 2025 | Another opportunity for a rate cut |

| 2026-2027 | Gradual easing of rates expected |

What This Means for You: A Personalized Take

As a seasoned observer of the real estate market, I believe this dip in mortgage rates offers a window of opportunity. Here's my take based on different scenarios:

- First-Time Homebuyers: Rates are still elevated when compared to the historically low rates of the pandemic era, but the recent drop provides some relief. Taking the time now to strengthen your credit score and checking with multiple lenders is going to be your biggest asset.

- Existing Homeowners Looking to Refinance: If your current mortgage rate is above 7%, keep a close watch on the Fed's decisions in September and December. There may be chances to refinance if rates drop further.

- Investors: Keep an eye on bond market volatility and how the 10-year Treasury yield reacts to Fed rhetoric. Also remember that the Fed anticipates a gradual easing, potentially settling near 2.25%-2.5% by 2027.

There is no one size fits all answer. The truth is, buying a home is a big financial decision, so take the time to assess your personal circumstances. Consult with a financial advisor and real estate professional to make informed choices.

In conclusion, keep an eye on the movement of mortgage rates and Fed meetings to maximize your financial potential. Be ready to make the move that is right for you!

Capitalize Amid Rising Mortgage Rates

With mortgage rates expected to remain high in 2025, it’s more important than ever to focus on strategic real estate investments that offer stability and passive income.

Norada delivers turnkey rental properties in resilient markets—helping you build steady cash flow and protect your wealth from borrowing cost volatility.

HOT NEW LISTINGS JUST ADDED!

Speak with a seasoned Norada investment counselor today (No Obligation):

(800) 611‑3060

Also Read:

- Will Mortgage Rates Go Down in 2025: Morgan Stanley's Forecast

- Mortgage Rate Predictions 2025 from 4 Leading Housing Experts

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?