Are you curious about the state of new housing construction? Do you want to know where the housing market is headed? Here's the bottom line: New housing starts are up, suggesting a potential rebound, but permits are down, indicating caution ahead. July 2025 saw a mixed bag of signals, with starts exceeding expectations but underlying uncertainties persisting.

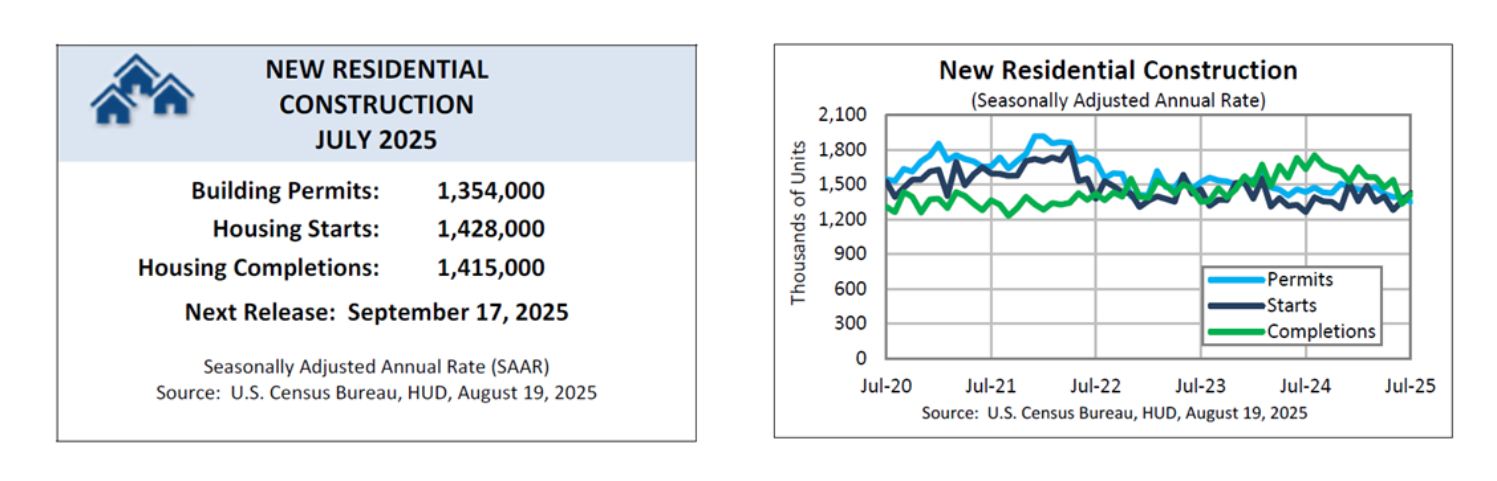

According to the U.S. Census Bureau and Department of Housing and Urban Development, overall housing starts increased 5.2% monthly in July to a seasonally adjusted annual rate of 1.43 million units. Overall, permits fell 2.8% monthly to 1.35 million annualized.

New housing construction trends are influencing everything from the size and design of homes to the materials used and the technologies incorporated. In the recent months, we have seen the new housing construction starts fall in the United States.

Housing Starts refer to the number of new residential construction projects that have begun during any particular month. Estimates of housing starts include units in structures being rebuilt on an existing foundation.

Building permits, on the other hand, are issued by local governments to allow builders to begin the construction of a new home or to make significant renovations to an existing home. Building permits are usually required for any new construction or remodeling that involves changes to the structural or mechanical systems of a home.

Housing construction refers to the actual building of the residential structure, which includes everything from laying the foundation to framing the walls, installing electrical and plumbing systems, and finishing the interior and exterior of the building.

The sequence of new housing construction events typically goes as follows:

A builder obtains a building permit from the local government, which allows them to start construction on a new housing unit.

Once construction begins, it is counted as a housing start. The construction process continues until the housing unit is completed and ready for occupancy, at which point it is considered part of the housing stock.

So, building permits come first, followed by housing starts, and then housing construction. However, it is important to note that not all permits lead to starts and not all starts to lead to completed construction. Some permits may expire before construction begins, and some starts may be delayed or canceled due to various reasons such as changes in market conditions or financing issues.

New Housing Construction: Starts, Permits, Completions 2025

Building Permits: A Glimpse into the Future

Building permits are like tea leaves for the housing market. They tell us what builders are planning to do in the coming months. When permit numbers decline, it suggests builders are becoming more cautious about starting new projects.

Here's a quick look at the July 2025 permit data:

- Privately-owned housing units authorized by building permits: 1,354,000 (seasonally adjusted annual rate)

- This is 2.8% below the revised June rate of 1,393,000.

- It is also 5.7% below the July 2024 rate of 1,436,000.

- Single-family authorizations: 870,000 (a slight increase of 0.5% from June)

- Authorizations of units in buildings with five units or more: 430,000

What does this tell us? While single-family permits saw a tiny uptick, the overall trend is downward. This indicates that builders are becoming less confident in the market's short-term prospects. High interest rates and rising construction costs could be playing a role in this decision to build less.

Housing Starts: Breaking Ground

While permits reflect future intentions, housing starts show us what's actually happening on the ground right now. These are the number of new homes that builders have begun constructing.

Here's the July 2025 housing starts data:

- Privately-owned housing starts: 1,428,000 (seasonally adjusted annual rate)

- 5.2% above the revised June estimate of 1,358,000

- 12.9% above the July 2024 rate of 1,265,000

- Single-family housing starts: 939,000 (2.8% above the revised June figure)

- Units in buildings with five units or more: 470,000

This data paints a more optimistic picture than the permit numbers. Housing starts are up across the board, suggesting that builders are still pushing forward with projects, possibly fueled by a need to meet existing demand. Perhaps they are optimistic about the longer term, betting that rates will eventually come down and that demand will continue to grow.

Regional Trends in Housing Starts:

Interestingly, there are significant regional differences in housing starts. Here's a summary of combined single-family and multifamily starts on a year-to-date basis:

- Northeast: 10.2% higher

- Midwest: 17.7% higher

- South: 2.4% lower

- West: 0.5% lower

The South's surprising drop is interesting. The region is one of the fastest growing regions in the U.S, particularly for single-family construction activity, getting an unexpected boost in July, powered by a building surge. Single-family starts rose 13% on the month and 22% annually.

Housing Completions: Bringing Homes to Market

The final piece of the puzzle is housing completions. This tells us how many new homes are actually finished and ready for occupancy.

Here's the July 2025 housing completion data:

- Privately-owned housing completions: 1,415,000 (seasonally adjusted annual rate)

- 6.0% above the revised June estimate of 1,335,000

- 13.5% below the July 2024 rate of 1,635,000

- Single-family housing completions: 1,022,000 (11.6% above the revised June rate)

- Units in buildings with five units or more: 385,000

Completions also rose in July but are lower year-on-year, suggesting perhaps that supply-chain issues from the past are still slowing down construction or that builders are still very cautious about building beyond existing demand.

The Big Picture: What Does It All Mean?

So how do we make sense of these seemingly contradictory numbers? Here's my take:

- Short-Term Caution, Long-Term Optimism: The drop in building permits suggests builders are wary about the short-term outlook. They're likely factoring in the impact of high interest rates, inflation, and persistent supply chain issues. However, the rise in housing starts indicates they are still committed to meeting existing demand and are perhaps optimistic about the longer-term prospects of the market.

- Regional Variations are Key: The housing market is not monolithic. Conditions vary significantly depending on the region. The Northeast and Midwest are seeing stronger growth in new construction, while the South and West are experiencing slowdowns. I expect it to be more of a nuanced and hyper-localized trend, given the overall macro-economic picture.

- Multifamily Driving Growth Multifamily construction has rebounded after falling to a 10-year low in 2024 – mainly to cater to affordability challenges in the single-family market, which have kept young families renting for much longer.

- Affordability Remains a Major Challenge: Even with the increase in housing starts and completions, affordability remains a significant hurdle for many prospective homebuyers. Persistently high mortgage rates and rising home prices are making it difficult for people to enter the market.

What to Watch For

Going forward, here are some key factors to keep an eye on:

- Interest Rates: Any significant movements in interest rates will have a major impact on the housing market

- Inflation: Continued high inflation will put pressure on construction costs and consumer spending

- Supply Chain Issues: Disruptions to the supply chain can delay projects and increase costs

- Consumer Confidence: How consumers feel about the economy will definitely influence their willingness to buy homes.

While the new housing construction market in 2025 presents a mixed picture, I believe that fundamental demand and supply imbalance could still drive growth. While starts are exceeding permits in some cases, more construction is needed and these numbers are always subject to change. As the market continues to evolve, staying informed will be key for those looking to navigate the complex world of real estate.

New Housing Construction Forecast 2025

So, what does all this mean for the rest of 2025? Here are a few key takeaways and factors to watch:

- Interest Rate Sensitivity: The housing market is extremely sensitive to interest rate changes. If rates stay high, affordability will remain a challenge, potentially dampening demand and construction activity.

- Construction Costs: Builders are always keeping an eye on the cost of materials and labor. If these costs continue to rise, it could put further pressure on housing prices and construction timelines.

- Government Policies: Government policies related to zoning, regulations, and incentives can have a big impact on housing construction. For example, streamlining the permitting process can help builders get projects off the ground more quickly.

- Tariffs: There have been discussions on tariffs on materials, especially from countries like China and Canada. These tariffs would further increase the cost of construction and decrease production.

- Regulatory Reforms: Regulatory reforms can help decrease the cost to builders and therefore help reduce home prices.

My Thoughts

Having followed the housing market for several years, I believe we're at a bit of a turning point. The days of rapid price appreciation and frenzied buying seem to be behind us, at least for now.

Here are a few of my observations:

- The need for affordable housing is critical. We need innovative solutions to make housing more accessible to a wider range of people. This could include things like smaller homes, accessory dwelling units (ADUs), and more efficient building techniques.

- Builders need to adapt to changing consumer preferences. Buyers are increasingly interested in energy-efficient homes, smart home technology, and flexible living spaces. Builders who can meet these demands will be better positioned for success.

- Local governments play a crucial role in shaping the housing market. By streamlining the permitting process, reducing unnecessary regulations, and investing in infrastructure, local governments can create a more favorable environment for housing construction.

Policy Paths: A Call for Action

Given the persistent affordability concerns, reducing inefficient regulatory costs offers the best policy path to improve attainable housing supply and bring down shelter inflation. This requires a collaborative effort from policymakers, builders, and community stakeholders. We have to find creative solutions that address the challenges facing the housing market.

Conclusion:

The new housing construction trends and forecast for 2025 suggest a market that's still finding its footing. While there are challenges, there are also opportunities. By understanding the key trends and factors at play, you can make informed decisions about buying, selling, or investing in real estate. I believe that a balanced approach, combining thoughtful planning with innovative solutions, is essential to navigating the dynamic housing market of 2025 and beyond.

Recommended Read:

- New Home Sales Trends and Forecast 2025

- Pending Home Sales Trends and Forecast 2025

- Historical Home Sales Data in the United States

- Single-Family Homes Construction Surges in September 2024

- High Mortgage Rates Impact New Construction: Builders Pull Back

- Benefits of Investing in New Construction Real Estate