Yes, you read that right! The significant drop in mortgage rates from 6.96% to around 6.06% over the past year is major news for anyone dreaming of owning a home or looking to refinance. This isn't just a small dip; it's a considerable shift that could put homeownership within reach for more people and save existing homeowners a substantial amount of money. As of mid-January 2026, long-term mortgage rates reached their lowest point in three years, marking a welcome turn of events for the housing market.

It signals a strong opportunity for buyers and a chance for existing homeowners to potentially lower their monthly payments. Let's dive into what this all means for you.

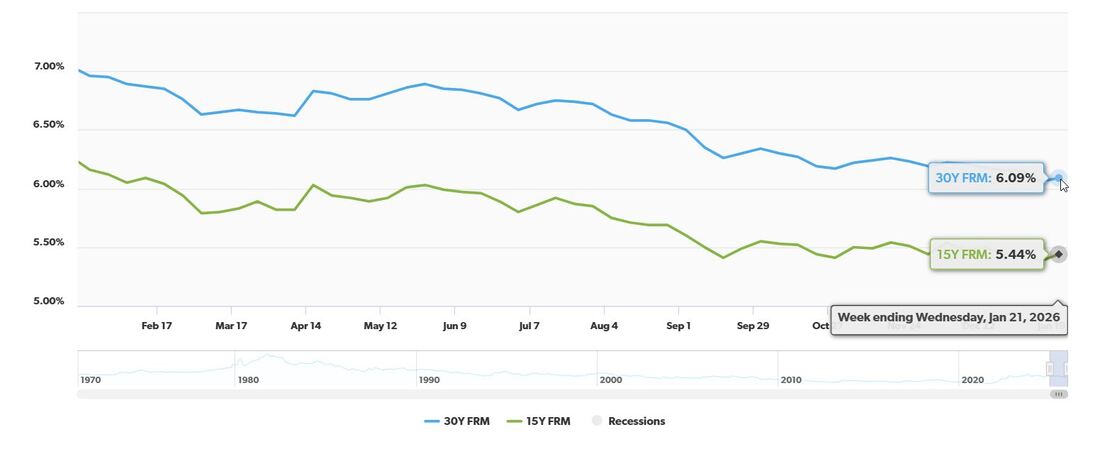

Mortgage Rates Plunge Nearly 1% in a Year, Sliding From 6.96% to 6.06%

Why Are Mortgage Rates Dropping So Much?

It’s not an accident that mortgage rates have fallen so dramatically. Several factors are at play, making this a particularly opportune time to consider a mortgage.

Government Intervention: A Big Push for Lower Rates

One of the most significant drivers of the recent decline was a strategic move by the government. In early January 2026, President Donald Trump announced a * $200 billion mortgage-backed securities buyback plan*. When the government buys these securities, it injects money into the mortgage market and, in turn, helps to lower borrowing costs for everyone. This kind of decisive action can have a powerful and immediate impact on mortgage rates, and we’re seeing that effect clearly now. It's a direct effort to make homes more affordable, and it seems to be working.

Market Influences: Keeping a Close Eye on the 10-Year Treasury

Beyond direct government action, mortgage rates are also closely tied to broader economic indicators. A key benchmark we always look at is the yield on the 10-year Treasury note. Think of this as a signal of what investors expect for the economy and interest rates in the future. When the 10-year Treasury yield is low, mortgage rates tend to follow suit. Recently, the 10-year Treasury yield has been hovering around 4.25%, which has helped keep those mortgage rates down. It’s a delicate dance between government policy and the natural forces of the financial markets.

The Real Financial Impact: What This Drop Means for Your Wallet

This isn't just about numbers on a screen; it translates into real savings. Let's break down the financial impact of this rate reduction.

As data from Freddie Mac’s Primary Mortgage Market Survey® shows, the average 30-year fixed-rate mortgage has seen a significant drop.

Here’s a snapshot of the recent trends as of January 22, 2026:

| Mortgage Type | Average Rate (Mid-Jan 2026) | Rate (Jan 22, 2026) | 1-Week Change | 1-Year Change | 52-Week Low | 52-Week High |

|---|---|---|---|---|---|---|

| 30-Year Fixed-Rate | 6.06% | 6.09% | +0.03% | -0.87% | 6.06% | 6.95% |

| 15-Year Fixed-Rate | 5.38% | 5.44% | +0.06% | -0.72% | 5.38% | 6.12% |

Notice how the 30-year fixed-rate mortgage averaged 6.06% in mid-January 2026, a substantial decrease from the 6.96% seen exactly one year prior. Even with a slight uptick to 6.09% by January 22, 2026, the savings are undeniable.

Let's look at a concrete example:

Imagine you're looking to buy a $400,000 home and need a mortgage of $320,000.

- At a 6.96% rate (last year): Your monthly principal and interest payment would be approximately $2,116.

- At a 6.06% rate (this year): Your monthly principal and interest payment drops to roughly $1,933.

That's a difference of nearly $183 per month! Over the 30-year life of the loan, this can add up to a colossal saving of nearly $66,000. That’s a significant chunk of change that could go towards renovations, investments, or simply enjoying life a little more.

The 15-year fixed-rate mortgage has also seen impressive drops, falling from 6.16% a year ago to around 5.38% in mid-January 2026. While the monthly payments are higher on a shorter term, the overall interest paid is considerably less, making it an attractive option for those who can afford it.

Who Benefits Most from These Lower Rates?

Firstly, first-time homebuyers are in a prime position. For years, the rising cost of homes coupled with high interest rates made the dream of owning a home feel unattainable for many. This drop in rates makes those monthly payments more manageable, potentially bringing more people into the market and making their first home purchase a reality.

Secondly, existing homeowners looking to refinance have a golden opportunity. If you have a mortgage with a rate significantly higher than today's offerings, refinancing could lower your monthly payments, free up cash flow, and even shorten your loan term if you choose. It’s a smart financial move that could save you tens of thousands of dollars.

And for those considering buying a larger or more expensive home, the lower rates mean you might be able to afford more house than you previously thought possible, without a drastic increase in your monthly outlay.

My Take: This is a Buyer's Market Moment

From my perspective, this isn't just a statistical blip; it's a strong signal that the housing market is becoming more accessible. While the economy is improving, which can sometimes push rates up, the government's intervention has created a temporary but significant advantage.

This is precisely why I always advise my clients to shop around for the best rate. Even a small difference in interest rates can lead to massive savings over time. Getting quotes from multiple lenders is crucial. Don't just go with the first one you talk to. Compare offers carefully, and don't be afraid to negotiate.

What to Keep in Mind Next

While these rates are fantastic, it’s important to remember that they can fluctuate. The 10-year Treasury yield can move, and economic conditions can change. If you're thinking about buying or refinancing, it's best to act while the timing is favorable.

Here are my key takeaways for you:

- Act Now: Take advantage of these lower rates while they’re available.

- Shop Around: Get multiple quotes from different lenders.

- Get Pre-Approved: This helps you understand your budget and shows sellers you’re serious.

- Consider Your Options: Think about whether a 15-year or 30-year mortgage best suits your financial goals.

- Work with a Trusted Advisor: A good mortgage broker or loan officer can guide you through the process.

This period of lower mortgage rates is a significant development, offering tangible financial benefits to a wide range of individuals. It's a moment where the dream of homeownership is becoming more attainable, and savings are readily available for those looking to optimize their finances.

And

Alabama’s newer A- rental vs Tennessee’s larger property with higher NOI. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- What Leading Housing Experts Predict for Mortgage Rates in 2026

- Mortgage Rate Predictions for 2026: What Leading Forecasters Expect

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?