The transformation of the American Dream, most broadly manifested in popular folklore as the aspiration of the US middle-class to own a home (even if it means agreeing to a 30-year loan with one's friendly neighborhood too-big-to-fail bank), into the American Nightmare, in which an entire generation (the Millennials) is locked out of purchasing a home due to over $1 trillion in student loans hanging over every financial decision, an abysmal jobs market (for everyone but college educated “waiters and bartenders” whose hiring is on a tear), and banks' unwillingness to lend money to anyone that can fog a mirror, and forcing millions of Americans to rent instead of buy, has been duly documented here before.

The transformation of the American Dream, most broadly manifested in popular folklore as the aspiration of the US middle-class to own a home (even if it means agreeing to a 30-year loan with one's friendly neighborhood too-big-to-fail bank), into the American Nightmare, in which an entire generation (the Millennials) is locked out of purchasing a home due to over $1 trillion in student loans hanging over every financial decision, an abysmal jobs market (for everyone but college educated “waiters and bartenders” whose hiring is on a tear), and banks' unwillingness to lend money to anyone that can fog a mirror, and forcing millions of Americans to rent instead of buy, has been duly documented here before.

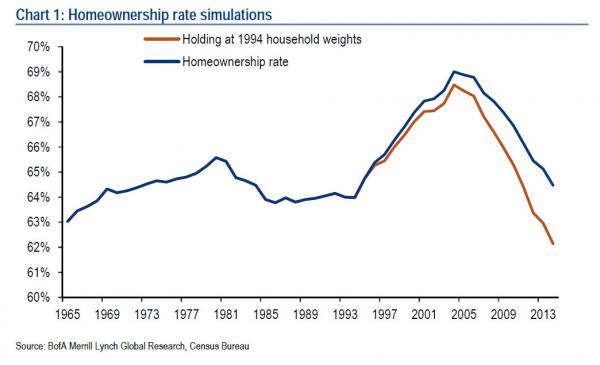

As we showed most recently in October, the officially reported US homeownership rate, after peaking during the first housing/credit bubble, has been plunging in a straight line and is now the lowest since 1994.

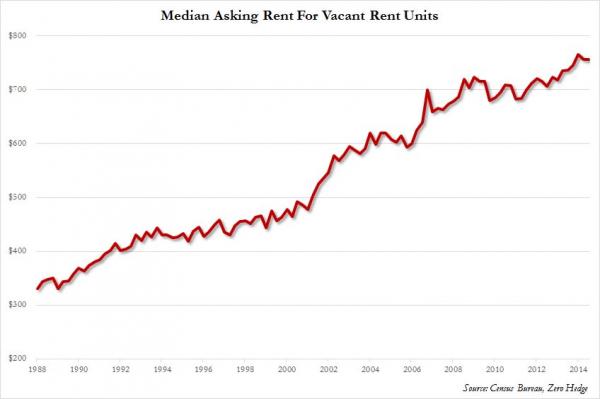

The offset: soaring, record high rents, because since few can afford the debt to purchase a still massively overpriced housing market, the only option is renting at which point the laws of supply and demand kick in.

We have also shown in the past why the “American Dream” is now anything but. The answer in one word: Millennials.

What is however not at all known, is that just like the unemployment rate's major methodological revision several decades ago, so too the homeownership calculation has been “adjusted” in recent years with the consequence of making it appear better than it is.

To normalize for this revision, Bank of America ran a simulation on the US Homeownership rate, in which it “derived a homeownership rate assuming household weights by age group as of 1994. In other words, we only allow for the change in the homeownership rates over time to matter, holding the household age weights constant. Under this methodology, the homeownership rate would have declined to 62.1% last year.”

In other words, instead of the most recently announced 63.9% homeownership rate, which was already the lowest since either 1983 or 1994 depending on how one looks at it, when stripping away the adjustment “fudge” which added some 2.3% to the homeownership rate simply because US households have aged, the real homeownership rate is far worse than what everyone believes.

As Bank of America summarizes, “this suggests that the decline in the homeownership rate thus far has been even more dramatic than the published data suggest.”

It does indeed, and as the chart below shows, when stripping away the now traditional assumption fudges which have flooded every single data set and made virtually all the New Paranormal data meaningless due to its reliance on pre-Lehman Brothers crash demographic and labor participation assumptions, the reality is that not only is the American Dream now completely over, but that the American Nightmare has never been worse, because as Bank of America just calculated, the real US homeownership rate has never been lower!