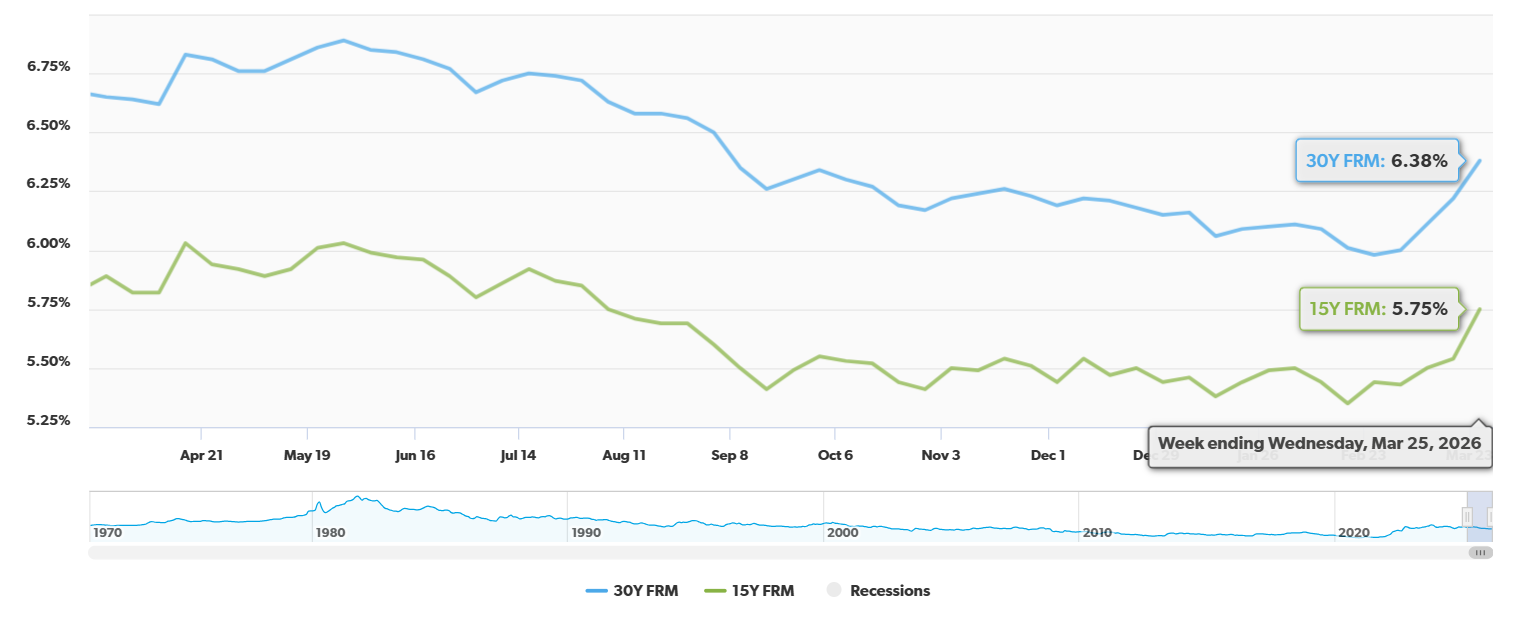

Well, if you're keeping an eye on mortgage rates and wondering what's happening right now, here's the good news: Today, March 31, 2026, mortgage rates have seen a slight dip, with the average 30-year fixed rate settling at 6.36%. This offers a small breather after a period of what feels like a rollercoaster ride for homeowners and potential buyers. It’s not a dramatic drop, mind you, but any sign of rates heading south is worth noticing in this current market.

Today's Mortgage Rates, March 31: 30-Year Fixed Goes Down Slightly to 6.36%

What the Numbers Are Saying Today

Thanks to Zillow's data, we have a clearer picture of where things stand. As of March 31, 2026, these are the average rates you're looking at:

| Mortgage Type | Average Rate |

|---|---|

| 30-Year Fixed | 6.36% |

| 20-Year Fixed | 6.32% |

| 15-Year Fixed | 5.81% |

| 5/1 ARM | 6.27% |

| 7/1 ARM | 6.20% |

| 30-Year VA | 5.89% |

| 15-Year VA | 5.47% |

| 5/1 VA | 5.41% |

Looking at this table, you can see the modest pullback is most evident in the fixed-rate options. Interestingly, the 30-year fixed rate has come down by 11 basis points (that's 0.11%), and the 15-year fixed has dropped by 9 basis points (0.09%). Adjustable-rate mortgages, or ARMs, are still hanging out above the 6% mark, which is something to keep in mind if you're considering those options.

Diving Deeper: Understanding the Popular Mortgage Types

Let's break down the most common mortgage types you see in that table:

- The 30-Year Fixed-Rate Mortgage: This is the king of the hill for many people. Your monthly principal and interest payment stays the exact same for the entire 30 years you have the loan. It offers fantastic predictability, which is a huge plus for budgeting. The trade-off? You generally pay a slightly higher interest rate compared to shorter-term loans because the lender is taking on more risk over a longer period. With today's rate at 6.36%, it's still a significant chunk of change, but down from where it was.

- The 15-Year Fixed-Rate Mortgage: This is like the speedy cousin of the 30-year. The rate is fixed, just like the longer term, but you pay off your loan in half the time. Because the loan term is shorter, lenders see less risk, and that's why you typically get a lower interest rate. Today's 5.81% is attractive, but be prepared for much higher monthly payments. The upside is you build equity much faster and save a massive amount on total interest paid over the life of the loan.

- Adjustable-Rate Mortgages (ARMs): For those looking at 5/1 or 7/1 ARMs, that first number (5 or 7) tells you how many years the interest rate is fixed. After that introductory period, the rate can adjust up or down based on market conditions. Today, the 5/1 ARM is at 6.27% and the 7/1 ARM is at 6.20%. The initial rate on an ARM is often lower than a fixed-rate mortgage, which can be appealing for people who plan to move or refinance before the fixed period ends, or if they anticipate rates falling in the future. However, the risk of higher payments down the line is real, and in this market, with rates still hovering, it requires careful consideration.

What's Driving Today's Mortgage Rates?

It’s not just random numbers that decide mortgage rates. A whole ecosystem of economic and global factors are at play. Here’s what's really shaping today's environment:

- That Lingering Geopolitical Unease: You can’t ignore what’s happening in the world. Conflict in the Middle East has been pushing oil prices higher, and that has a ripple effect. When energy costs go up, it can fuel inflation concerns. And when inflation is a worry, it often means bond yields (which mortgage rates follow closely) tend to climb. It’s a complex chain reaction, but it’s definitely playing a part in keeping mortgage rates from plummeting.

- The Fed's Steady Hand (For Now): The Federal Reserve just had its March 18 meeting, and they kept the federal funds rate right where it was, between 3.50% and 3.75%. Their message was pretty clear: they’re not in a rush to start cutting rates unless they see inflation consistently moving towards their 2% goal. This cautious approach from the Fed sends a strong signal to the market about the direction of interest rates, and it means we shouldn't expect any drastic drops anytime soon.

- Refinance Woes: Honestly, it’s been tough for homeowners looking to refinance lately. With rates stubbornly high, many people are finding themselves “locked in” to their existing mortgages that have much lower rates. You can see this in the numbers: refinance applications have dropped by 15% in recent weeks. It just doesn't make financial sense for most people to refinance into a higher rate. This lack of refinance activity also affects the broader mortgage market.

- What the Experts Are Thinking: I always like to see what the smart folks in the industry are predicting. Economists at Bankrate, for instance, are projecting that the 30-year fixed mortgage rate might average around 6.1% for the rest of 2026. Now, they’re also quick to point out that we should expect continued volatility. It’s not a straight line down, so we have to be prepared for ups and downs.

Peeking into the Future: What's Next?

Looking ahead is always a bit of a crystal ball exercise, especially in finance. But here’s what some major players are forecasting:

- Fannie Mae's Outlook: They're suggesting that if inflation does manage to stabilize, the 30-year fixed rate could even dip just under 6% by the end of 2026. That would be a significant win for many potential buyers.

- The Mortgage Bankers Association (MBA) View: The MBA is taking a slightly more conservative stance. They expect rates to mostly hang out between 6.10% and 6.30% through the remainder of 2026 and even into the early part of 2027. This suggests that while rates might not skyrocket, they also might not fall dramatically in the immediate future.

My Takeaway: A Breath of Fresh Air, But Stay Sharp

So, what’s the bottom line on today’s mortgage rates for March 31, 2026? We’ve seen a nice little dip, with the 30-year fixed at 6.36% and the 15-year fixed at 5.81%. It’s a bit of good news and a welcome reprieve from the constant upward pressure we've been feeling. However, and this is a big “however” from me, the overall economic picture is still quite uncertain. Geopolitical events, inflation worries, and the Federal Reserve's cautious stance mean that volatility is here to stay.

If you’ve been contemplating a refinance or looking to buy a new home, it’s absolutely crucial to weigh these modestly lower rates against your personal financial goals. Remember, lender offers can change by the day, and what looks attractive today might be different tomorrow. It’s a good time to be informed, stay vigilant, and perhaps have a chat with your mortgage professional to see what options might be best for your situation right now.

VS

Georgia’s affordable rental with higher cap rate vs Florida’s A‑rated property with stability. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?