All good investors are visionaries. That is, before making an investment they make predictions about the future – which may or may not come true.

All good investors are visionaries. That is, before making an investment they make predictions about the future – which may or may not come true.

That said, and working with the humility appropriate for any investor with a healthy appreciation for risk and instinct for survival, here are eight trends we believe will make their mark on rental real estate going into 2015 and beyond.

Rental Demand Will Be Strong

Apartment demand is going to stay strong for a while. Despite a broad economic recovery from the 2008-2010 recession on the surface, millennials and Generation Y members aren’t exactly emerging from their parents’ basements by the millions, nor are they particularly eager to get married and start families in little starter homes like their parents and grandparents before them did.

“14% of 24-35 year olds are still living with parents.” – 2013 Gallup poll

Yes, we all know exceptions. But data indicates that young Americans are waiting longer to complete all kinds of rites of passage: Marriage, home-ownership, and through no fault of their own, careers.

Case in point: The U.S. Census Bureau reported that Americans formed about 746,000 new households last year. That seems like a lot, but it’s well below the normal level of about 1.1 million.

Why? Here are three reasons:

1. Housing Bubble Burst

This generation saw either their parents, neighbors and friends’ parents devastated by the collapse of the housing bubble. They saw people driven to bankruptcy and despair by pursuing what used to be the dream of home-ownership. They learned to distrust banks. And so what used to be a middle-class rite of passage is now perceived as a risky endeavor, best left to the firmly established.

2. Volatile Employment

Employment is less stable. Two generations ago, it was common to start with a firm and spend 20 or 30 years there, retiring with a gold watch and a pension. It made great sense to buy a home as soon as you could, because you had a reasonable expectation of stable employment. Now pensions are a thing of the past, and stable career workers have been supplanted by an army of contractors, or short-term workers. More and more people are forced to make do cobbling part-time employment and contracting gigs together to make a living.

3. Loan Rejection

It’s tough to get a mortgage. Yes, interest rates are low. But good luck qualifying for a mortgage when you’ve got nothing but self-employment, temp jobs and part-time income on your application – and you’re saddled with record student loan payments pushing your debt-to-income ratio into the stratosphere.

Put these things together, and younger Americans age 18-35 or so aren’t going to be flocking to join the ranks of homeowners for a while. Nor are the teenagers who will be joining that demographic over the next several years.

We’ll see some pent up demand for home-ownership make itself felt at some point. But it could be years before we see today’s millennials leave their rental units behind and make a big demographic-scale shift to home-ownership.

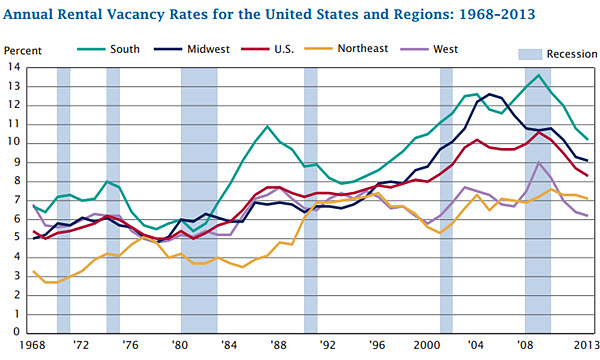

Vacancy Rates Will Decline

We present you the U.S. Census Bureau Housing trending graph:

A couple of things to note:

1. First, there is no historically significant correlation between national vacancy rates and recessions. Vacancy rates in previous recessions either continued previous trends, or they drifted all over the place.

2. Second, the decline in vacancy rates since they peaked around 2009-2010 is an extraordinarily powerful trend, and it’s nationwide. Indeed, the trend began in the Midwest well before the recession.

This is a secular trend that transcends the traditional market cycle, and is reflective of the larger socioeconomic, demographic and cultural changes we hinted at above – changes in the nature of employment and work, and in changes in the priorities value systems of younger middle-class Americans with regard to education, employment and their willingness to start a family.

Smaller Cities Will Dominate ROI

Millenials aren’t exactly staying on Ma and Pa’s farm. But they don’t have to move to New York, Los Angeles and Chicago anymore to seek their fortunes. Indeed, many won’t, but will choose to live in areas with a more modest cost of living.

Telecommuting has made a lot of things possible, and one of them is young creative-class people don’t have to actually work in a skyscraper when they can email their files to the Manhattan corporate headquarters from their porch in Peoria.

This is a much better deal for the renter in the early years of his or her career than having to live in a shoebox in the city.

Walkability Will Matter

We’ll also see renters increasingly value neighborhood “walkability”. Why? Young Americans are choosing to bike rather than drive. We are already seeing solid evidence of a “walkability” premium in recent years, beginning with this University of Arizona study that found that “on a 100-point scale, a 10-point increase in walkability increases property values by 1 to 9 percent, depending on the type.”

See also this study by the Brookings Institution taking a look at the Washington D.C. market. That trend will continue, though if fuel prices remain low its effect will be slightly muted.

Tech Centers Will Rule

Technology centers are those areas that have made investments in public WiFi, for example, but also that have a steady influx of technologically savvy younger workers, whether minted from local universities or attracted by major employers who have set up shop in the area.

Think areas like the Research Triangle of North Carolina, for example, or areas rapidly spreading from Northern California up to Seattle along the I-5 corridor.

Mortgage Rates Will Rise

This isn’t going to make it any easier for the basement-dwellers and apartment residents to make the leap. But monetary policy has held mortgage rates down – at the expense of savers – for many years now, and there are limits to how long that policy can last.

We’re not alone. Mortgage giant Freddie Mac’s team of economists are projecting mortgages to be approaching 5 percent by the end of 2015. The 30-year fixed rate is hovering around 4 percent, so while 5 percent may sound low to those of us who have been around a while, it also represents a 25 percent increase.

To put it in perspective, that’s enough to push the payments on a $200,000 house from $954 to $1,073 – an increase in housing costs of over 10 percent.

A 1% point increase in mortgage rates from today’s levels would result in a mortgage payment increase of 10 percent for 30-year fixed rate buyers.

Economic Confidence Will Improve

Aside from the projected increase in interest rates, 2015 should be a decent year for economic growth as well. Freddie Mac’s economist team is projecting economic growth of about 3 percent overall, which is enough to fuel an overall prosperity, but not indicative of a bubble formation. If a bubble exists, it is probably in the form of student loan debt, now above $1 trillion outstanding, which weighs heavily on the ability of younger Americans to qualify for a mortgage or even save meaningfully for a down payment as their parents did.

But there is more to the housing market, certainly, than struggling college grads.

Data from the National Association of Realtors (NAR) indicates that consumer confidence is on the rise, and now stands at the highest it’s been in 7 years (their consumer confidence index was 94.5 in October). That’s slightly below the long-term average of 100. But if there is one thing we know now, that we didn’t know in 2007, it’s that the long-term average consumer confidence rate was too high anyway!

We note that consumer sentiment is actually more optimistic than real estate professionals – the NAR is reporting that while consumer confidence is at a 7 year high, realtor confidence in the future is at a 2½ year low.

Empty Nesters Will Rent Again

In past generations, people raised their children and then either stayed in their paid-for homes into their golden years, or downsized to plow excess money into rental real estate, annuities or other income investments. But recently, observers noted a different trend of baby-boomers, who are now empty nesters, migrating to rentals at the rate of 200,000 households a year from 2010 to 2013, according to reporting from Multi-family Executive Magazine.

These aren’t geriatric folks, these 50+ and 60+ individuals and couples are healthier and more active than previous generations were at that age – and they want to be where the fun is. As a result, many of them are flocking to urban cores and centers of dining and recreation, rather than suburbia.

What’s driving the trend?

Lifestyle Choices – Some people don’t want to grow old mowing the lawn.

Foreclosures – Some of these individuals were displaced by the foreclosure crisis when their real estate decisions went south in 2007-2012.

Divorce – It’s not uncommon now for parents to stay together for the sake of the kids – and then go their separate ways. In this case, either or both former spouses may choose to move back to town or rent an apartment for the time being.

These trends will last far beyond 2015: The Joint Center for Housing Studies is projecting that by 2023, half of the growth in renters will be in the 65 and older crowd.

– – – – –

RealtyTrac’s numbers are confirming these trends, thus far. This means that rental property investors (and those property managers advising them and executing their strategy) have some marketing options. It’s not just about the 18-35 crowd anymore. The rental market is likely to be a mix of younger individuals and families who have not yet transitioned to home-ownership on one hand – and baby boomers who are downsizing from home-ownership on the other.

Each will likely have different preferences for amenities, recreational activities, and housing sizes as boomers are going for the 2 and 3-bedroom rentals while the millennials are keeping things small.