As of February 24, 2026, the average mortgage rates are still holding comfortably below the 6% mark, which is fantastic news for anyone looking to buy a home or refinance. Specifically, Zillow data shows the 30-year fixed rate is at 5.875% (with an APR of 6.015%), and the 15-year fixed rate is at 5.375% (with an APR of 5.638%). This offers a welcome sense of stability in today's housing market.

Today’s Mortgage Rates, February 24: Buyers Benefit from Stable Fixed Rates

Today's Mortgage Rates: A Detailed Look

Let's break down what we're looking at today, according to Zillow's most recent figures as of February 24, 2026.

Here's a clear picture of the current average rates:

| Loan Type | Interest Rate | APR |

|---|---|---|

| 30-Year Fixed | 5.875% | 6.015% |

| 20-Year Fixed | 5.875% | 6.114% |

| 15-Year Fixed | 5.375% | 5.638% |

| 10-Year Fixed | 5.250% | 5.654% |

| 30-Year FHA | 5.625% | 6.299% |

| 30-Year VA | 5.625% | 5.897% |

| 30-Year Jumbo | 5.875% | 6.030% |

| 7/6 ARM | 5.625% | 6.173% |

As you can see, the 30-year fixed rate is the most commonly sought-after loan, and sitting below 6% is a significant positive for affordability. The 15-year fixed rate offers even better savings if you can swing the higher monthly payments. It's interesting to note how close the 20-year fixed rate is to the 30-year, suggesting it might be an attractive middle ground for some buyers.

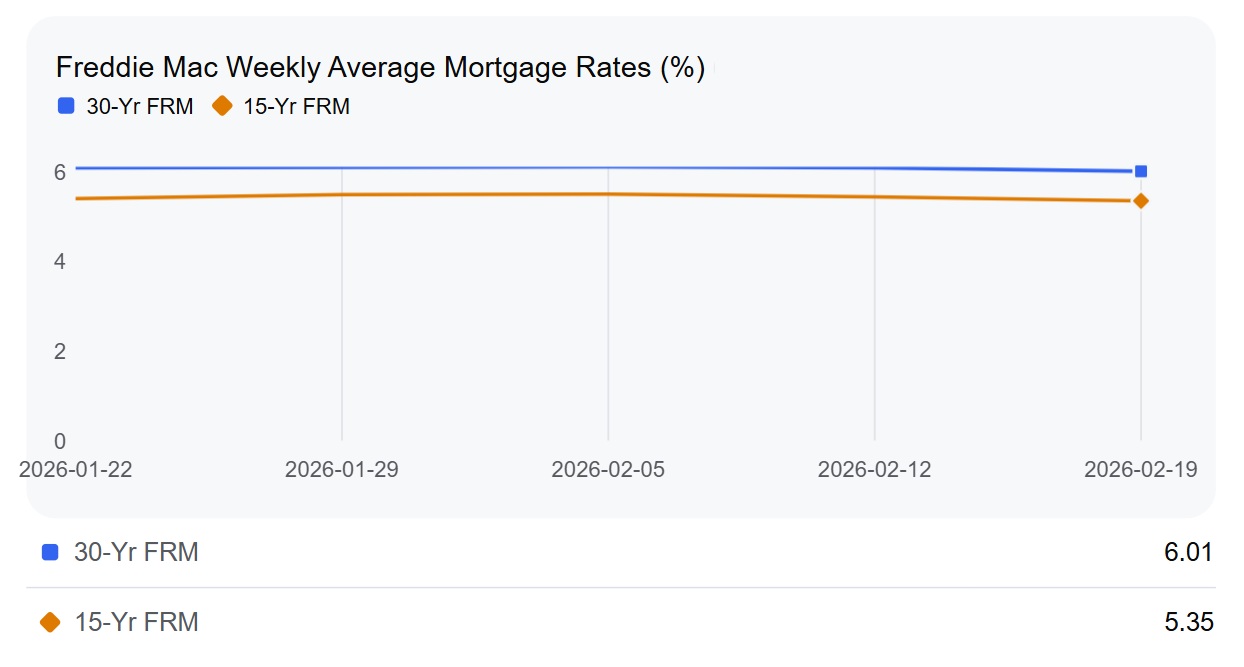

Where Have We Been? Weekly Rate Trends

Looking at the past week, we've observed a slight upward tick in fixed-rate mortgages.

- The 30-Year Fixed rate has seen a modest increase of about 13 basis points, moving from roughly 5.74% to its current 5.875%.

- Similarly, the 15-Year Fixed rate has nudged up by 6 basis points, from around 5.41% to the current 5.375%.

While these might seem like small numbers, they represent lenders adjusting their pricing based on various market forces. From my experience, these kinds of small movements are normal and don't necessarily signal a major shift. It's more about lenders fine-tuning their offerings.

Understanding the Bigger Picture: Market Context

It's crucial to put these current rates into perspective. The fact that we're below 6% for the average 30-year fixed mortgage is a huge win when you recall the spikes we saw in late 2023 when rates touched nearly 7.80% in some instances. Zillow's data showing averages near 5.86% on certain marketplaces indicates some lenders are even offering rates slightly better than the average.

Key Market Developments Shaping Today's Rates:

- Federal Reserve's Influence: The Federal Reserve's decision to hold rates steady at their January 2026 meeting was anticipated. The general feeling among experts is that we might see one or two rate cuts later in the year, provided inflation continues its downward trend. Still, the minutes from recent meetings emphasize a cautious approach, especially concerning services inflation. This means borrowing costs could remain relatively stable for a while.

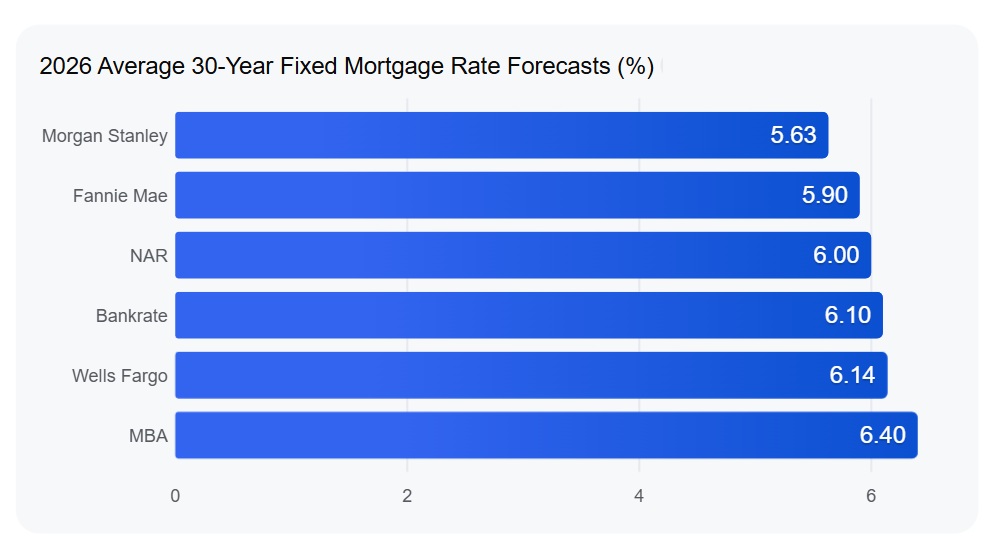

- Economic Projections: Major housing organizations like Fannie Mae and the Mortgage Bankers Association (MBA) are forecasting that 30-year mortgage rates will stay within a tight range, likely between 6.0% and 6.1%, for the rest of 2026. This predictability is a huge plus for long-term financial planning.

- A Boost for Refinancing: With rates significantly lower than they were throughout 2024 and most of 2025, refinance applications have more than doubled in the past year. People are smart to lock in lower monthly payments if they have an opportunity.

What Does This Mean for You?

So, how do these today's mortgage rates February 24 2026 affect you?

- For Homebuyers: If you're in the market for a new home, rates below 6% offer a much more manageable cost of borrowing compared to just a year ago. This is a solid window to explore your options and secure financing without breaking the bank.

- For Those Looking to Refinance: Even with the slight recent uptick, if your current mortgage rate is above 6.5%, it's still very likely worth exploring a refinance to potentially lower your monthly payments and save money over the life of your loan.

- Government-Backed Loans (FHA & VA): The FHA and VA loans are incredibly competitive right now at 5.625%. These are excellent options for many borrowers looking for accessible ways to become homeowners.

- Adjustable-Rate Mortgages (ARMs): You'll notice that the 7/6 ARM rate is very close to the fixed rates. This narrows the traditional gap where ARMs offered significantly lower initial payments. For many, the predictability of a fixed rate might outweigh the minimal savings of an ARM right now.

My Take on Today's Mortgage Rates

From where I stand, the mortgage market on February 24, 2026, is in a good place. The slight increases we've seen this week are just minor fluctuations, and the overall picture is one of stability and affordability. Rates remaining below 6% for most major loan types is a fantastic situation for both new buyers and homeowners looking to improve their financial standing. It's a practical time to sit down, crunch the numbers, and see what options make the most sense for your personal financial goals.

VS

Texas’s A‑rated rental with stability vs Ohio’s affordable property with higher cap rate. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to Our Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?