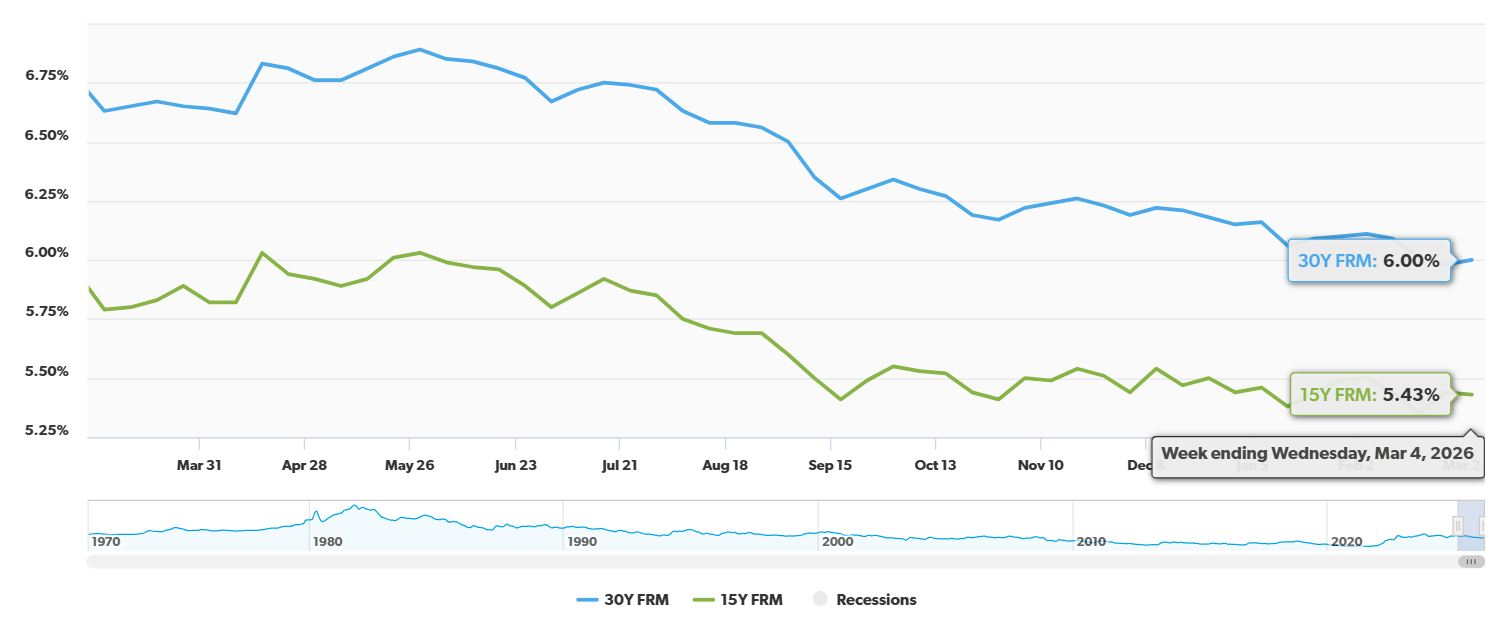

The average 30-year fixed mortgage rate has seen a significant drop, falling by a whopping 63 basis points to hit 6%. This is a major development, bringing rates to their lowest point since 2022 and offering potential savings and new opportunities for countless homeowners and aspiring buyers.

I can tell you that movement like this in mortgage rates is not just a statistic; it's a game-changer. A nearly full percentage point decrease in just a year can translate into thousands of dollars saved over the life of a loan. It's the kind of news that gets people looking at their finances and dreaming a little bigger.

30-Year Fixed Mortgage Rate Drops Steeply by 63 Basis Points

What Does a 63-Basis Point Drop Really Mean?

Let's break this down. When we talk about basis points, it might sound a bit technical, but it's quite simple. One basis point is equal to 0.01%. So, a 63-basis point drop means the average rate has decreased by 0.63%.

This isn't just a small wiggle; it's a substantial shift. Think about it this way: if you're borrowing a significant amount, like say $300,000, a 0.63% difference in your interest rate can easily shave off tens of thousands of dollars from your total payments over 30 years. That's money that can go towards your down payment, home improvements, or simply boost your savings.

Freddie Mac's Latest Survey: The Numbers Don't Lie

The data comes to us from Freddie Mac's latest Primary Mortgage Market Survey®, released on March 5, 2026. According to their findings, the average 30-year fixed-rate mortgage is now standing at 6%. This is a noticeable dip from the 6.63% we saw this time last year.

Even just from the previous week, the average rate saw a tiny bump up by 2 basis points, but that hardly takes away from the enormous yearly gain. It’s important to look at the bigger picture, and the year-over-year change is what's truly exciting.

We also saw some movement in the 15-year fixed-rate mortgage. This popular option averaged 5.43% this week, a slight decrease from last week's 5.44% and a decent drop from 5.79% a year ago. While not as dramatic as the 30-year fixed, it's still positive news for those looking for shorter-term mortgages.

A Table of Savings: Seeing is Believing

To really grasp the impact of these rate changes, let's look at a clear breakdown of the numbers and the potential savings.

| Mortgage Type | Current Avg. (03/05/2026) | 1-Wk Change | 1-Yr Change | Potential Yearly Savings (on $300K loan) |

|---|---|---|---|---|

| 30-Yr Fixed FRM | 6.00% | +0.02% | -0.63% | Approx. $2,000+ |

| 15-Yr Fixed FRM | 5.43% | -0.01% | -0.36% | Approx. $1,000+ |

Note: Potential yearly savings are approximate and based on a $300,000 loan amount. Actual savings will vary based on loan principal, exact interest rates, and loan terms.

As you can see, that -0.63% change for the 30-year fixed rate is significant. If you have a $300,000 mortgage, this translates to roughly over $2,000 in savings per year. Over the 30-year term, that’s potentially tens of thousands of dollars back in your pocket. This is a huge deal, folks.

Why Are Rates Falling? More Than Just One Reason

It's easy to see a rate drop and just cheer, but understanding why it's happening can give us even more insight. While interest rates are influenced by a complex web of economic factors, here's what I'm seeing:

- Inflation Control: Central banks (like the Federal Reserve in the U.S.) often raise interest rates to combat inflation. When inflation shows signs of cooling down, these central banks may start to ease off, leading to lower borrowing costs, including mortgage rates.

- Economic Signals: The overall health of the economy plays a huge role. If there are signs of a slowdown or a desire to encourage more spending and investment, lower interest rates can be used as a tool.

- Treasury Yields: Mortgage rates are closely tied to the yields on U.S. Treasury bonds, particularly the 10-year Treasury note. When bond yields go down, mortgage rates tend to follow suit.

However, it's not always a smooth ride. Freddie Mac's Chief Economist, Sam Khater, pointed out that recent global events, like tensions in the Middle East, have caused some volatility and an increase in 10-year Treasury yields. This can put upward pressure on mortgage rates. But, despite these jitters, the overall trend is still very favorable for borrowers.

What This Means for You: Buyers, Sellers, and Refinancers

This significant drop in 30-year fixed mortgage rates is like a breath of fresh air for the housing market.

- For Buyers: If you've been priced out of the market or finding it tough to qualify, this could be your moment. Lower rates mean lower monthly payments, making homes more affordable. It’s a fantastic time to get off the sidelines and start your homeownership journey. I’m seeing more first-time buyers jump in because the math suddenly makes sense for them.

- For Sellers: While lower rates can increase buyer demand, it’s also worth noting that people who bought when rates were higher might be hesitant to sell if they’d have to buy a new place with a higher rate. However, the increased pool of buyers due to affordability can still lead to a healthy market.

- For Refinancers: If you currently have a mortgage with a rate significantly higher than the current 6%, refinancing could be a smart move. You could potentially lower your monthly payments, shorten your loan term, or even tap into your home's equity. I’ve seen homeowners save hundreds a month by simply refinancing at a better rate, and this drop makes it even more compelling. Refinance activity is already on the rise, and I expect it to continue strong.

The Takeaway: Act Smart, But Don't Rush

Seeing mortgage rates hover near their lowest levels since 2022 is incredibly encouraging. The 63-basis point drop in the 30-year fixed mortgage rate is a clear signal that opportunities are present.

My professional advice?

- Get Pre-Approved: If you're a buyer, get pre-approved for a mortgage so you know exactly what you can afford.

- Shop Around: Don't take the first offer from a lender. Compare rates and fees from multiple lenders to ensure you’re getting the best deal.

- Understand Your Options: Talk to a mortgage broker or loan officer. They can help you understand which loan products (fixed-rate, adjustable-rate, etc.) best fit your financial situation and goals.

- Consider Refinancing: If you're an existing homeowner, run the numbers. It might be time to lower your monthly housing costs.

This is a dynamic market, and rates can fluctuate. While recent geopolitical events have added some uncertainty, the overall trend of lower rates is a significant positive for anyone involved in real estate. Enjoy this welcome relief, and make informed decisions!

VS

Nashville’s A‑rated rental with stability vs Birmingham’s affordable property with higher cap rate. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain near 6%, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Will Mortgage Rates Drop to 5% in 2026: Expert Forecast

- How to Get a 3% Mortgage Rate in 2026 With Assumable Mortgages?

- How to Get a 4% Interest Rate on a Mortgage in 2026?

- What Leading Housing Experts Predict for Mortgage Rates in 2026

- Mortgage Rate Predictions for 2026: What Leading Forecasters Expect

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?