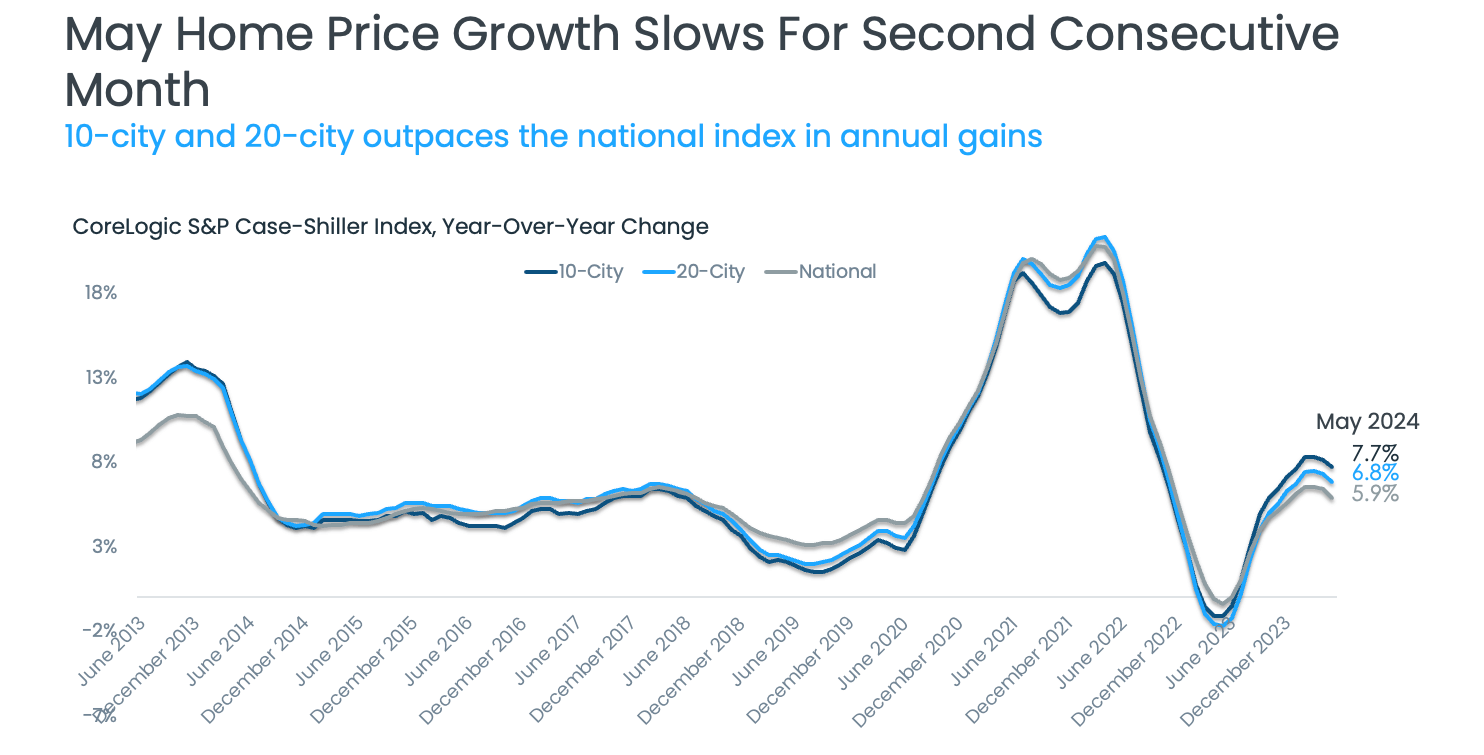

As September 2024 unfolds, the financial world is closely monitoring the Federal Reserve (the Fed) and its expected decision to cut the Federal Funds Rate. This anticipation is largely fueled by compelling economic indicators, such as a slow yet steady cooling of inflation rates and signs of a softening job market.

According to Mark Zandi, Chief Economist at Moody’s Analytics, “They’re ready to cut, just as long as we don’t get an inflation surprise between now and September, which we won’t.”

Such statements highlight the confidence among economists regarding the Fed’s forthcoming actions. But what real implications will this have for the housing market, and more importantly, for you as a potential homebuyer or seller?

The Significance of the Federal Funds Rate Cut

📈

The Federal Funds Rate

The Federal Funds Rate is a critical lever in the complex machinery of the U.S. economy, influencing everything from consumer credit costs to mortgage rates.

💰

Impact of Rate Cut

When the Fed lowers this rate, it typically signals a broader economic shift that impacts mortgage rates both directly and indirectly.

🏠

Housing Market Significance

The significance of a Federal Funds Rate cut on the housing market can be profound, affecting everything from mortgage affordability to overall housing demand.

The Federal Funds Rate is a critical lever in the complex machinery of the U.S. economy, influencing everything from consumer credit costs to mortgage rates. When the Fed lowers this rate, it typically signals a broader economic shift that impacts mortgage rates both directly and indirectly.

As someone who has followed economic trends closely for years, I can attest that these shifts often occur within a delicate balance of market forces and public sentiment. Although a one-time rate cut may not prompt an immediate drop in mortgage prices, it can accelerate a downward trend that has been building over time.

Mike Fratantoni, Chief Economist at the Mortgage Bankers Association (MBA), emphasizes this trend: “Once the Fed kicks off a rate-cutting cycle, we do expect that mortgage rates will move somewhat lower.” This underscores the interconnectedness of Fed policy and housing affordability.

Economists like Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), suggest that we are likely entering a prolonged rate-cutting cycle. He forecasts, “Generally, the rate-cutting cycle is not one-and-done. Six to eight rounds of rate cuts all through 2025 look likely.” This potential for multiple cuts lays the groundwork for sustained changes in housing market dynamics.

Projected Impact on Mortgage Rates and Housing Demand

The impact of the Federal Reserve's anticipated rate cuts on mortgage interest rates is a focal point for both buyers and sellers. The latest forecasts from reputable sources such as Fannie Mae, MBA, NAR, and Wells Fargo indicate that, as inflation stabilizes and economic sentiment improves, we could witness a gradual decline in mortgage rates through 2025.

Key Reasons This is Good News for Buyers and Sellers

- Alleviating the Lock-In Effect: One of the most significant barriers to the housing market is the “lock-in effect,” where existing homeowners hesitate to sell their properties for fear of losing favorable mortgage rates. Lower mortgage rates could provide an incentive for these homeowners to consider selling, thus increasing inventory. Although this alone may not lead to a sudden influx of listings, it creates a more favorable environment for movement in the market. However, many homeowners may still exercise caution due to the fear of re-entering the market at higher interest rates.

- Boosting Buyer Activity: The prospect of lower mortgage rates makes the housing market more attractive for potential buyers. A reduction in rates decreases the overall cost of borrowing and the total expenses associated with homeownership. For first-time buyers and those looking to upgrade, this represents an opportunity to make a purchase without being burdened by excessive monthly payments. Analysts predict that, as mortgage affordability improves, more buyers will re-enter the market, creating a ripple effect that could further stimulate housing demand.

Considerations for Homebuyers and Sellers

While the Federal Funds Rate cut is expected to gradually lower mortgage rates, it’s essential for both buyers and sellers to consider their individual circumstances. The current economic climate showcases both opportunities and challenges. Jacob Channel, Senior Economist at LendingTree, encapsulates this with a timely reminder: “Timing the market is basically impossible. If you’re always waiting for perfect market conditions, you’re going to be waiting forever. Buy now only if it’s a good idea for you.”

In essence, prospective homebuyers should focus on their financial readiness rather than attempting to time the market perfectly. Meanwhile, sellers should evaluate their current situation and weigh the potential benefits of listing their homes in a gradually improving market against the uncertainty of future price movements.

Bottom Line

The anticipated Federal Funds Rate cut, influenced by a healing economy marked by improving inflation and slower job growth, is likely to create a positive, albeit gradual, impact on mortgage rates. This new environment could unlock significant opportunities for both homebuyers and sellers. As you prepare to navigate the dynamic landscape of the housing market, engaging with a knowledgeable local real estate agent can provide you with invaluable insights and support tailored to your unique situation.

ALSO READ:

- Real Estate Forecast Next 5 Years: Top 5 Predictions for Future

- Is the Housing Market on the Brink in 2024: Crash or Boom?

- 2008 Forecaster Warns: Housing Market 2024 Needs This to Survive

- Housing Market Predictions for the Next 2 Years

- Real Estate Forecast Next 10 Years: Will Prices Skyrocket?

- Housing Market Predictions for Next 5 Years (2024-2028)

- Housing Market Predictions 2024: Will Real Estate Crash?

- Housing Market Predictions: 8 of Next 10 Years Poised for Gains

- Trump vs Harris: Which Candidate Holds the Key to the Housing Market (Prediction)

![This Texas Housing Market is the Best in the U.S. [2024 Rankings]](https://www.noradarealestate.com/wp-content/uploads/2024/08/this-texas-real-estate-market-is-the-best-in-the-us-300x157.jpeg)