Three things you can take to the bank:

Three things you can take to the bank:

- Politicians will bend with the wind,

- Property taxes will never decline, and

- Rising home prices will increase low appraisals.

It’s no surprise that complaints that appraisals are once again killing too many sales are once again on the rise this summer.

Through June, home prices nationwide, including distressed sales, increased year over year by 5.7 percent in June, rising most in the lower price ranges according to CoreLogic, which forecasts that prices will increase by 5.3 percent on a year-over-year basis to June 2017.

Twenty-three states and the District of Columbia have reached new highs in June: Alaska, Arkansas, Colorado, Hawaii, Iowa, Indiana, Kansas, Kentucky, Louisiana, Massachusetts, Montana, North Carolina, Nebraska, New York, Oklahoma, Oregon, South Dakota, Tennessee, Texas, Utah, Vermont, Washington and Wyoming.

Meanwhile, appraisers across the country are having a hard time justifying many deals. As a result, appraisals come in below contract prices, lenders finance less that buyers need, and unless buyers can come up with the cash to make up the difference, sales fall through.

This time, complaints about low appraisals came from the top.

“Appraisal-related contract issues have notably risen over the past year and were the root cause of over a quarter of contract delays in the past three months,” said NAR President Tom Salomone yesterday.

“This is likely a combination of sharply growing home prices in some areas, the uptick in home sales this year and the strong refinance market overworking the already reduced number of practicing appraisers. Realtors® are carefully monitoring this trend, and some have already indicated they’re extending closing dates on contracts to allow extra time to accommodate the possibility of appraisal-related delays,” he said.

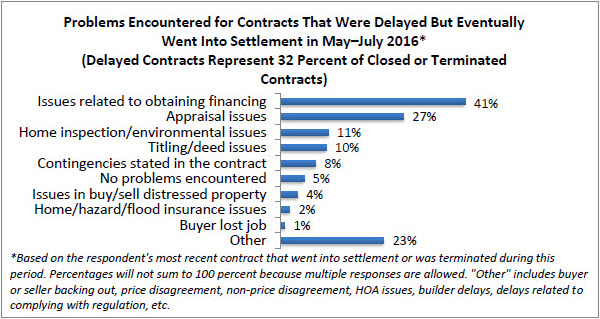

Among the 32 percent of contracts that had a delayed settlement financing in July but were eventually settled, appraisal problems were responsible for 27 percent of delays. Among the 6 percent of contracts that were terminated in July, appraisal issues were responsible for 17 percent. However, rising prices and low appraisals don’t always coincide perfectly. A year ago, in July 2015, when home prices rose 6.9 percent — more than they did this year – appraisal problems accounted for only 23 percent of delays and 15 percent of terminations.

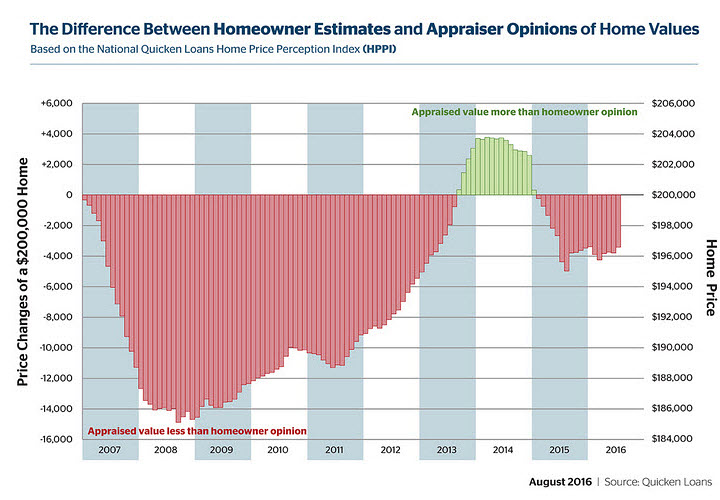

Quicken Loans tracks disparities between what refinancing owners think their homes are worth and actual appraisals and the Quicken Loans National HPPI tracks closely with Realtor complaints about low appraisals. The July report found that appraised values were an average of 1.69 percent lower than what homeowners expected. The gap between appraisals and owner expectations actually narrowed in July. In June, appraisals lagged behind expectations by 1.93 percent.

“One of the most important things for consumers to take away from the HPPI is just how regionalized housing truly is,” said Quicken Loans Chief Economist Bob Walters. “While those on the West coast are being surprised by their high appraisals, homeowners in the Northeast and Midwest are more likely to be shocked by their low values. If homeowners keep an eye on local home sales, they can be better aware of their current home value and not be shocked when they go to sell or refinance.”

“One of the most important things for consumers to take away from the HPPI is just how regionalized housing truly is,” said Quicken Loans Chief Economist Bob Walters. “While those on the West coast are being surprised by their high appraisals, homeowners in the Northeast and Midwest are more likely to be shocked by their low values. If homeowners keep an eye on local home sales, they can be better aware of their current home value and not be shocked when they go to sell or refinance.”